RBA minutes released earlier today did not uncover new earth, but basically tossed around the same things that have been said over and over once more.

On China:

– Chinese Economy is on “sustainable” growth while Financial conditions in China remain accomodative

It is interesting to see RBA having such a positive outlook on China, as Chinese Manufacturing PMI has been barely crossing the 50.0 mark and New Yuan Loans have been generally lower than expected. Furthermore, there have been new tightening measures to curb rising property prices, pushing the Shanghai Composite Index and even spilling over to the Hong Kong Hang Seng Index lower. PBOC has also been guiding USD/CNY lower – pushing Yuan stronger. These do not sound like accomodative measures, and it is a surprise that RBA continue to believe China to be keeping a loose belt.

Verdict – Hawkish

On Global Growth:

– Growth in US “moderate”, with improvement in housing market and payrolls. Sequester cuts came “into force in full”, unlike what most forecasters expected . Europe is expected to remain weak due to fiscal consolidation despite improvement in overall sentiment and economic activity recently.

RBA refrained from commenting on the impact of the sequester cuts, but economic outlook on US remains upbeat. Europe remains a concern though the issues raised by RBA is common knowledge and does not provide additional bearish insights.

Verdict – Neutral

On Domestic Economy:

– Mining sector grew further in Q4, though sector is approaching peak.

– Investment outside mining sector decline in Q4, but there are indications that levels will recover later in the year.

– Business profits have declined while debt levels rising at 4% per annum

– Domestic consumption mixed, but maintain “modest” growth

– Labor market “remain subdued” despite steady unemployment rate, though modest employment growth in the near term can be expected

Again no surprises here as all these are common knowledge. RBA is maintaining a “modest” outlook which is still mildly positive.

Verdict – Mildly Hawkish

On Financial Stability:

– Australia banks continue to enjoy strong profitability in recent periods.

– Wholesale funding cost has eased with improved global market sentiment

– Household and Business borrowing “restrained”. Debt-servicing capacity higher due to lower interest rates.

There is very little reason for RBA to cut rates based on this as banks are stable. Rate cuts have bring down borrowing costs to end consumers and allow better servicing ratios despite a slight recent increase in unemployment rate. With everything looking healthy, a further rate cut would only encourage more borrowing and result in inflationary pressure.

Verdict – Hawkish

On Monetary Policy:

– Lending rates “clearly below normal levels”

– Low rates still have further to run

– Exchange rate remained high, while inflation levels allow further rate cut if necessary.

Perhaps the most important paragraph of the minutes. It seems that RBA does not see any reason for rate cuts, and the “scope” that was mentioned was simply referring to current inflation level which is in the middle of the targeted band – hardly the most dovish scope. The dovish “if necessary” line appears to be thrown just as a cursory remark just because so many other Central Banks are touting the same thing, rather than a actual threat of rate cut. This is similar to the SNB’s recent re-affirmation of their 1.20 EUR/CHF defence – hardly relevant right now but still acting as a deterrence against speculators.

Verdict – Neutral

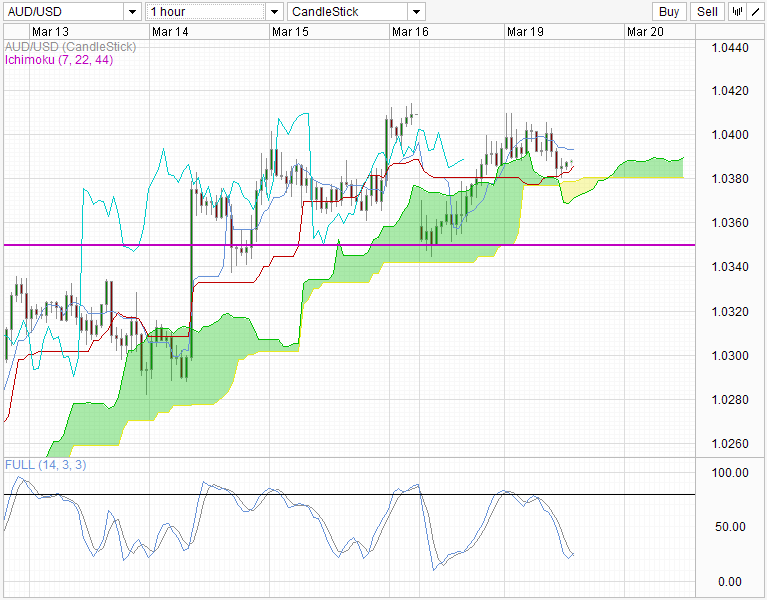

Hourly Chart

The overall slightly hawkish/less dovish tone pushed AUD/USD higher by 20 pips, pushing price above 1.04. However, overall tone is still bearish as Cyprus outcome continues to weigh risk correlated assets down. Nonetheless, bulls should be glad that we’ve recovered most of the losses of Monday and have closed the bearish gap. Price is also supported above current Kumo and the Kijuu-Sen, and sitting above the consolidation of 15 Mar, which will help support price against any short-term sell-off.

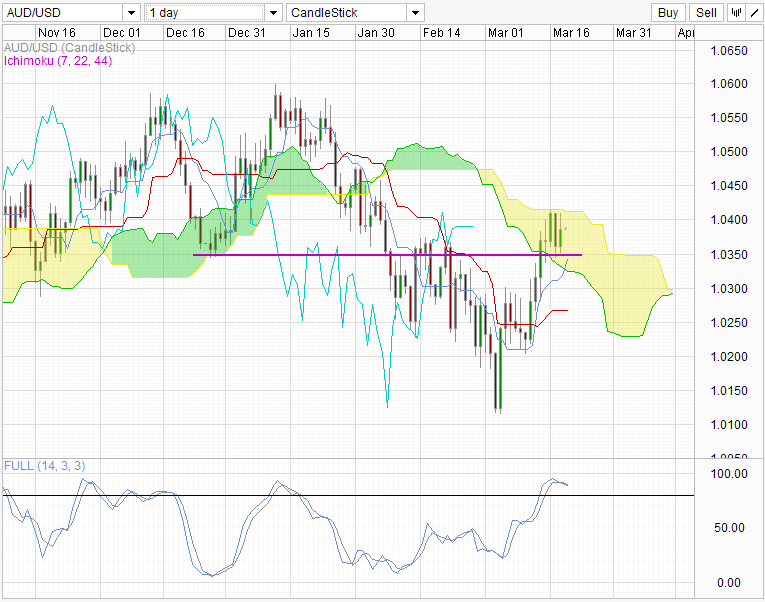

Daily Chart

Outlook from Daily Chart perspective is uncertain, as price is trading right in-between current Kumo, and also trading around the bottom back in late Dec. A clean break above 1.04 and the Kumo upwards will help to accelerate bullish momentum, while a break below 1.035 will most probably have the opposite effect. This outlook is in-line with the Cyprus uncertainty and we could see fundamental catalyst pushing price either side easily especially since RBA is losing their dovish influence in the market; Overnight Index Swaps are pricing in a paltry 8% probability for a 25 bps rate cut in the April meeting. Expect bears to lose influence (or perhaps they already did looking at the rally since early Mar) and bulls to gain initiative from here.

Click here for the full RBA minutes

More Links:

AUD/USD – Settles Between Key Levels of 1.0360 and 1.04

GBP/USD – Consolidates Around 1.51

EUR/JPY Technicals – Cypriot presents strong potential either side

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

centers on forex and macro-economic trends impacting the Asia Pacific region.

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014