It was not even an April fool prank – just do not take dollar strength for granted. The mighty dollar dropped its guard yesterday and lost some of the previous night’s gained ground in the wake of a lower than expected US March ISM manufacturing data. It was only last week that global investors bobbed and weaved; shrugging off some near market misses, proving that the dollar love fest experience of late is not eternal starting the second-quarter. The EUR bears will have been startled awake from their holiday slumber and may even become a tad more apprehensive ahead of Friday’s US non-farm payroll number. Any sign of a disappointing jobs report could send the dollar on a more dramatic retreat.

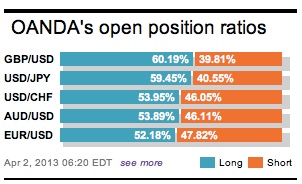

Being a EUR bear and suffering from ‘ostrich syndrome’ would be painful, but out of sight and mind would not be too bad either. However, yesterday’s post US ISM blues, supported by most of the components being weaker, was only capable of squeezing the ‘weaker’ 17-member single currency short positions. Now, if only they had the stomach to wait for this morning’s European manufacturing numbers.

Activity in the Euro-zone manufacturing shrank last month at its fastest rate in three-months (46.8 vs. 47.9) and new-orders also declined at a faster pace, suggesting the industry will continue to struggle further. Not good news for Euro leaders, just more proof that a recovery will not be beginning any time soon. This will only increase the duration of the already 15-month downturn. The worsening state of the Euro-zone factory activity only puts more pressure on the bloc’s leaders who have been banking on any increasing activity to reduce some of the fiscal burden and the need for additional financial handouts.

Digging deeper, factories in Germany (49.0) and Ireland lost momentum, having grown in previous months, while falls in output accelerated in Austria, the Netherlands, Italy (44.5 – 20th straight month of contraction), Spain (44.2), France and Greece. Germany, the anointed backbone of Europe, is a major concern. A return to falling new order levels was the main factor behind the contraction headline. Manufactures continue to cite the uncertain economic outlook as the reason for Germany’s slowdown. With manufacturing accounting for +20% of the German economy worries about Q1 German growth rate will be reinforced after today’s headline release. Will the ECB be persuaded that a euro-rate cut is needed sooner rather than later now that her ‘Knight’ could be in trouble?

The ECB meet Thursday and consensus is for the refi-rate to remain on hold at +0.75%. However, a more dovish stance is to be expected and the door for more stimuli most likely will be kept open. The highlight of the morning should be the post press conference – especially after the decisions over the Cypriot bailout and its implications for the euro area as a whole.

The pace in decline in the UK’s manufacturing sector was little changed last month (48.3 vs. 47.9). However, it remains below 50 confirming that the sector continues to shrink. The average for Q1 was 49, below the average 49.2 for Q4, 2012. The data confirms that demand remains subdued, while prices increased and job cuts continued, suggesting that the sector will have likely weighed on output for Q1. This also means that the UK service sector, which accounts for +77% of the economy, must provide a strong showing in order to bypass a second straight contraction in GDP in Q1. The weaker headline also increases the likelihood that the BoE will extend QE at Thursday’s meeting.

What about Sterling? In truth, it needs to be much weaker if it’s going to help rebalance the weakening UK economy. So far, despite a much weaker exchange rate this year, the UK has made little progress in addressing its external imbalances. Some analysts foresee a requirement of another -7% correction, relative to 2012 levels in order to put the “UK net international investment position on a sustainable path.”

The number of people out of work in the Euro-zone climbed to new heights in February, as the regions fiscal and debt crisis continues to take its toll. Officially +19.071 million or +12% of the working population are unemployed across the 17-member union. The demographic and regional breakdown shows continued divergence between the stronger and weaker economies within the union: the stronger north, Germany (+5.4%) and Austria (+4.8%) versus the weaker south, Cyprus (+14%) and Spain (+26.3%).

The typical fiscal year-end selling of US treasuries by Japanese investors for window dressing purposes did not transpire last month. Treasury yields remained persistently consistent, and in fact some maturity yields happened to fall on the month. Historically, Japanese fund managers would typically repatriate foreign earnings by cashing out US bonds and equity positions – lock in profits and “window dress” balance sheets. To many, this week supposedly could become the watershed moment for interest rates or monetary policy for the Bank of Japan. Investors remain single-mindedly focused on the new Governor Kuroda of the BoJ policy meet tomorrow. Expectations for aggressive easing are high due to the banks +2% inflation target. If he disappoints then this market will end up being merciless. So far this week, the Yen has managed to strengthen outright and against the EUR amid the disappointing Tankan result and slightly weaker than expected manufacturing data out of China (50.9). Investors have been happily locking in more profits rather than fresh buys in front of this week’s policy meeting.

This morning’s weaker Euro PMI’s should present further downside risk for the 17-member single currency (1.2850). So far during the European session, Swiss sellers have succeeded in taking the EUR’s off its highs (1.2880), with EUR/JPY long liquidation continuing to prove highly influential for the EUR’s direction. Some positive Cyprus news has managed to offset the disappointing PMI’s for now. The country has happened to raise the approval ceiling for financial transactions to +EUR25k and unblock part of the deposits frozen under the bail-in. If anything, the positive Cypriot news would likely promote further top picking. Resistance remains at 1.2880-1.29 and with further stops positioned just above. This market needs to close above 1.2929 for the single-currency to maintain its upward momentum.

Other Links:

EURO: Is It Too Late For Holiday Surprises?

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019