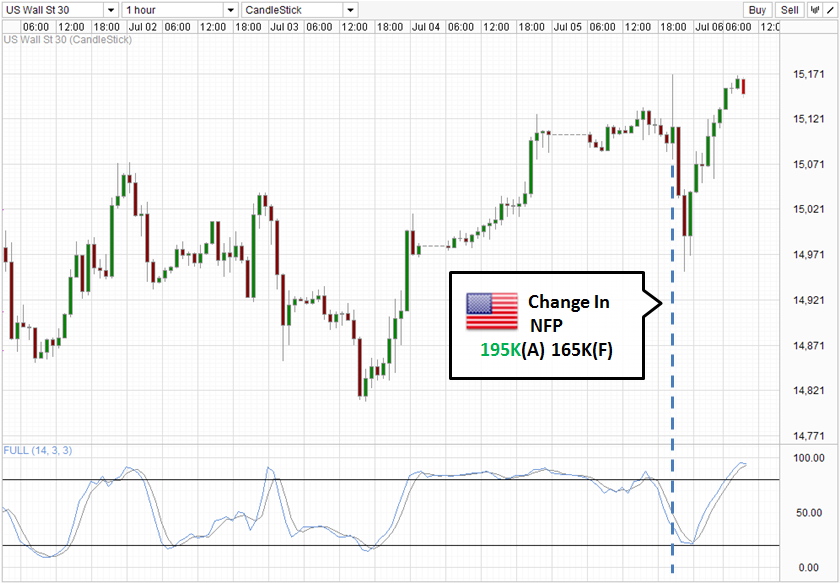

So the big reveal is over. US NFP came in at 195K, matching previous month’s growth rate and hitting the 190-200K monthly figure that economists believe will be needed to push unemployment rate back under 6.5%. This is a strong print, especially since initial analysts estimates expected a 165K growth (likely to have increased considering the over-expectation ADP employment print on Wed). However, despite the stronger NFP numbers, US unemployment rate remained at 7.6%, and not the 7.5% that everybody expected.

The bipolar nature of US employment numbers created yet another layer of issues to the interpretation of results. Before the news release, we already had the problem of “buy on Bad news, sell on Good” behavior which was noted ever since Ben Bernanke started his QE tapering talks. Market was looking forward to disappointing economic numbers, in hope that Bernanke will be forced to keep QE3 going in fear of destabilizing the modest economy. The problem with the 2 opposite numbers ( Strong NFP vs Weak Unemployment Rate) is that it is now difficult to ascertain for sure that the “buy on Bad News, sell on Good” behavior is still in play, as we do not truly know whether traders are favoring the stronger NFP figures and discounting the weaker Unemployment Rate (and vice versa) when making their buying/selling decisions.

If we were to look at historical behaviors – traditionally NFP absolute numbers tended to be more important that Unemployment Rate, as the latter tends to move about by 0.1% regularly due to sampling issues. If we were to use this interpretation this time round, the initial rally post NFP release makes sense – as stock market rally believing that US economy is healthy. The subsequent decline (almost immediately) also fits nicely into the rubric of “sell on Good” – as traders/speculators start to worry about the impending tapering of QE3. What is troubling is the resulting rally that followed the dip. Both S&P 500 and Dow 30 saw strong recovery rallies just before midday, with prices continuing to rally strongly, ending the week on the weekly high. If this assertion has been right so far, it would imply that market is now climbing out of the contra-ion news trading behavior, suggesting that we could see more straight forward trading moving forward, and the bearish reaction on an actual Bernanke’s QE taper action would be more muted.

The problem with the above interpretation is that we could easily assume market to be pricing in the weaker Unemployment Rate more, and follow the narrative to end up believing the contra-ion behavior is stronger than before. However, looking across all other risk correlated assets (commodities, non US equities), the initial reaction on NFP is much more bullish than the subsequent pullback, unlike US stocks. This favors the former assertion, as the contra-ion behavior is not apparent on all other assets except for US stocks.

Dow 30 Hourly Chart

Looking from a technical perspective, it is interesting to note that Future Prices did not manage to end on the weekly highs as the underlying equities did. Price did continue to rally this morning due to bullish optimism spilling over into the Asian markets, but we’re currently seeing signs of early topping with Stochastic indicator showing that a Stoch/Signal cross may occur fairly soon.

S&P 500 Hourly Chart

It is the same for S&P 500, with Stoch/Signal looking likely to cross. However, both indexes are mildly bullish right now, and price would need to break significant resistances (1,625- 1,630 for S&P 500 and 15,120 – 15,150 for Dow 30) in order for a stronger bearish bias to take hold. This is in line with the Stoch indicators which are still far away from providing a proper Bearish signal. A break of the significant resistances will likely result in readings pushing below 80.0 for both indexes, and hence forming bearish cycle signals.

On the USD front, the Greenback is the biggest trump on Friday, beating ALL major currencies. This is a significant breakthrough, as the positive correlation with US stocks is back, which also lends weight to the assertion earlier. Should market rally due to the contra-ion behavior, we should theoretically see USD weaker due to higher easing hopes.

More Links:

EUR/USD – Testing Long Term Support Level of 1.28

AUD/USD – Trying to Stay Above Key 0.90 Level

Week in FX Americas – The Fed Stills Needs to Convince

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

centers on forex and macro-economic trends impacting the Asia Pacific region.

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014