US yields have gone down in recent weeks, pulling away from the fabled 3.00% line in the sand due to a myriad of reasons.

On the economic front, we have weaker than expected US NFP numbers, while minutes of latest FOMC meeting reflected a more dovish Fed than expected, favoring higher bond prices.

Social political factors aren’t encouraging either – Ukraine has just declared they will be rolling out a “large-scale antiterrorist operation” in response to the armed protests sprouting across the eastern region which borders Russia. Unlike the much more peaceful referendum seen in Crimea, Ukraine seems bent on using military efforts to thwart current uprising with President Olekasndr Turchynov saying that they will prevent “the repetition of the Crimean scenario” during a televised address on Sunday. Unfortunately it seems that Russia is going for tic for tac, with reports suggesting that up to 40,000 Russian troops have been amassed along Ukraine borders ready to march in if necessary. This may all turn up to be a hoax, but it is genuine enough that U.N. security council has called for an emergency meeting to address the situation. With the sound of war drumming nearer, it is no surprise that safe haven flow has been pumping commodities such as Gold and Oil higher, while traders are flocking to USD and US Treasuries for safe keeping.

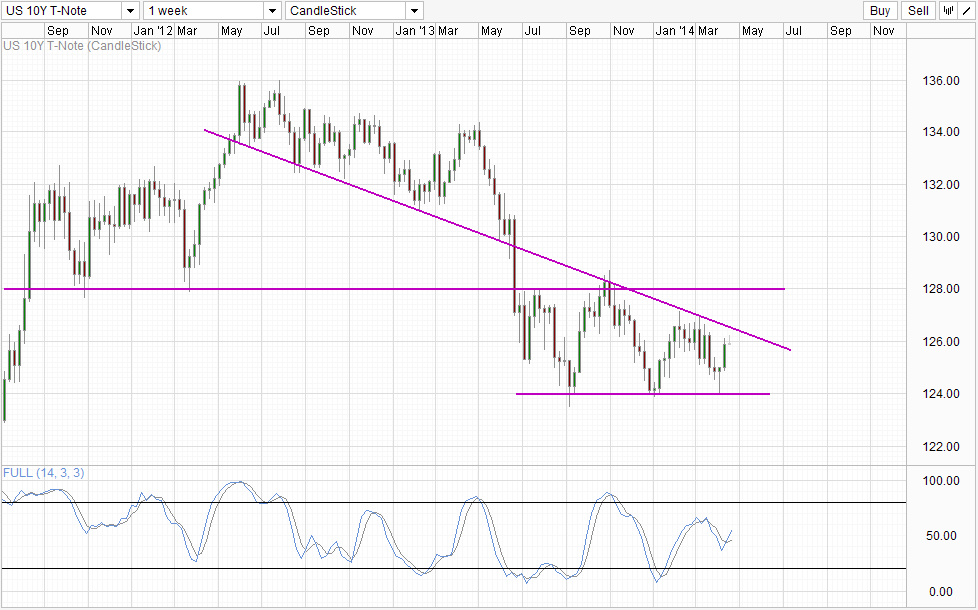

Where does that bring us? Implied yield is currently standing at just under 2.62% while 10Y short-dated Futures are just under 126.0 round figure. From a price action perspective, staying below 126.0 suggest that long-term bearish trend remains in play since prices is staying below the descending trendline and perhaps more importantly below the 2014 high. Looking for a relative yield perspective, 2.62% is also not really that low considering that we were trading at 1.63% just under a year ago. Furthermore, there is also a “support” level seen at the 2.5% implied yield level (not visible from chart), suggesting that trend has not reversed.

This makes sense because all the factors mentioned earlier are all in the short-term. Even if there is a war breaking out, it is going to be localized between the eastern European front. Similarly, even though US economic numbers have been below expectations, the recovery narrative remains intact and we should be able to see continued tapering of Quantitative Easing and eventual higher rates to push Treasuries yields up. It is all simple mathematics really. Can the increased demand from safe haven flow be enough to offset the reduction in Fed’s purchases? In the short run it is certainly possible, but it is unlikely that this can continue indefinitely. As such, demand for Treasuries will eventually fall and yields will climb closer to 3% once again.

More Links:

WTI Crude – Bullish Momentum Stalling At 104.0 Resistance

Gold Technicals – Marching Towards 1,330 On Sound Of Ukraine Unrest

Week In FX Europe – BoE To Judge Slack Before Hike

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014