It’s been another mixed start to trading in Europe on Monday and U.S. futures suggest it’s not going to be too different on the other side of the pond.

We have another big week in store in the markets, with particular focus falling on Thursday’s Bank of England monetary policy decision and Friday’s U.S. jobs report. The BoE opted last month to go against expectations and hold off on easing monetary policy following the Brexit vote in June as it wanted to gather more data before deciding on the best course of action. Once again, it’s widely expected that the BoE will announce a new round of stimulus measures at the meeting this week although it’s not clear what form they will take. We could see something as simple as a rate cut, possibly even down to zero percent, maybe with some more asset purchases. Alternatively, they may look at funding for lending again, or something along the same lines, as a way to prevent funding to businesses and households drying up.

Week Ahead Central Bank Stimulus in Focus

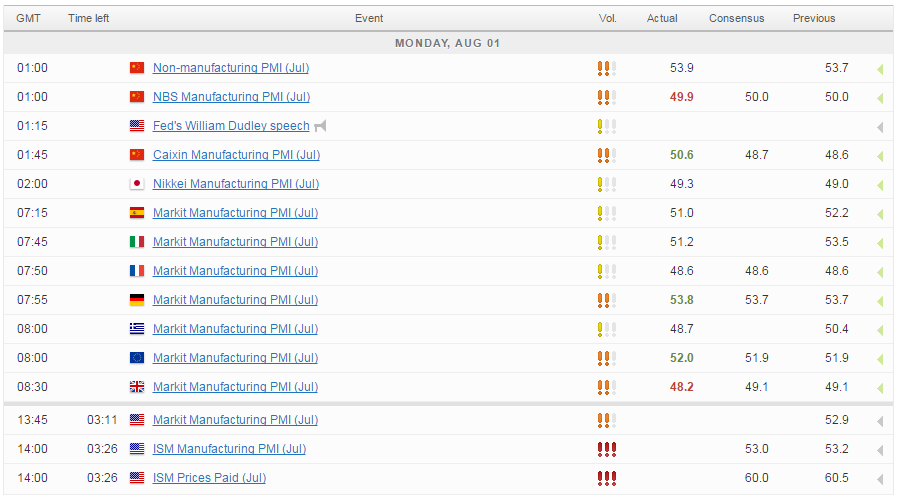

As for today, attention has very much been on the manufacturing PMIs, with China and Japan releasing their results overnight, a number of countries in Europe releasing them throughout the morning session and the U.S. releasing figures after the open on Wall Street. So far the numbers have been a bit of a mixed bag, with the official Chinese PMI dipping into contraction territory for the first time since February while the Caixin reading rose back into growth territory, comfortably beating expectations, for the first time since February last year. On the one hand, it’s positive that the small to medium private firms that are covered more by the Caixin reading are finally seeing the benefit of all the stimulus efforts, the flip side of this though is that the official number which covers large state owned businesses is clearly struggling with the transition. The services PMI, which covers an increasingly important sector for the economy, helped to offset this pessimism, rising to 53.9.

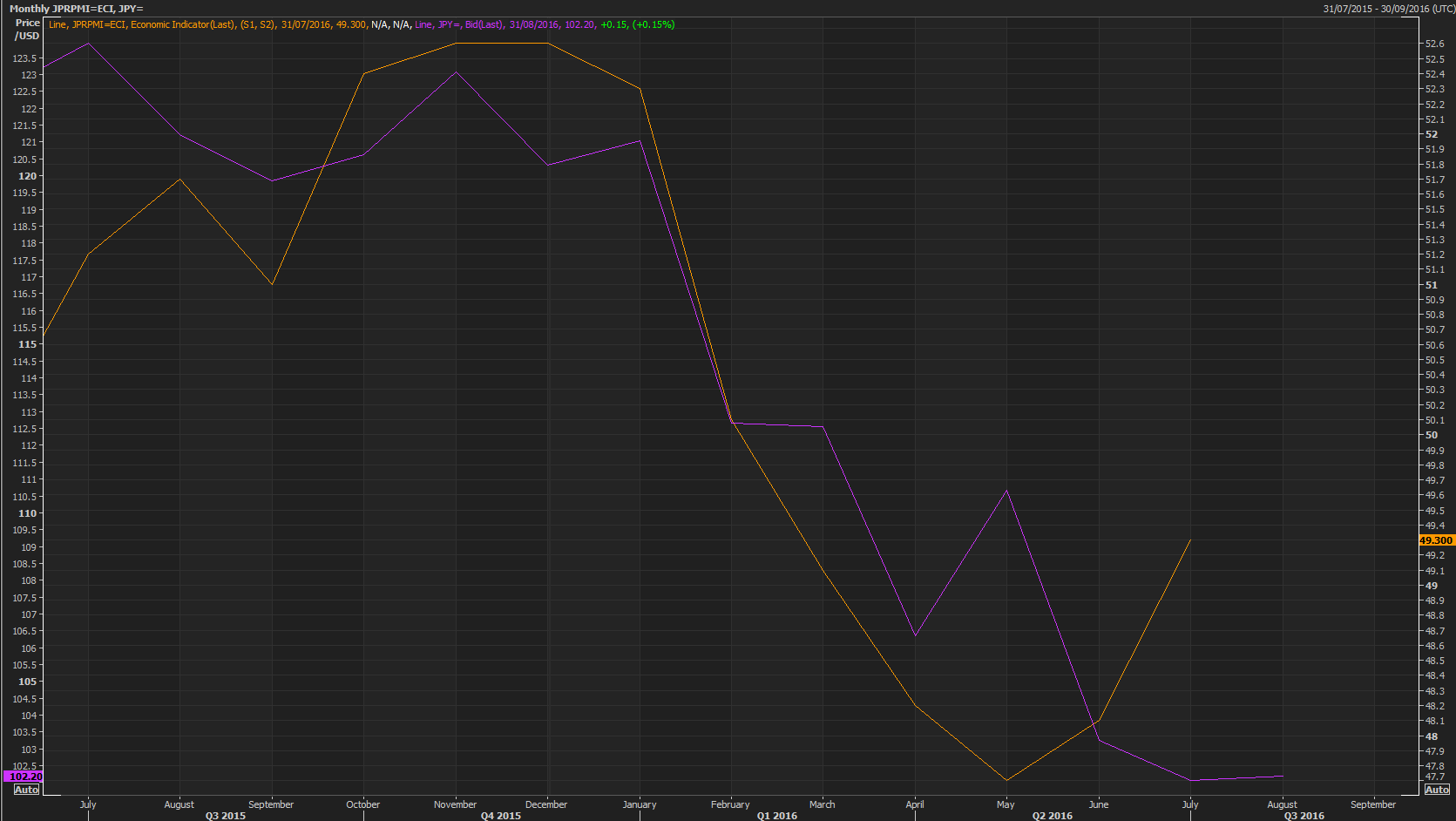

It was a familiar story for Japan, where the stronger yen appears to be weighing on the outlook for the manufacturing sector. New export orders contracted at the fastest pace in more than three and a half years, a trend that may continue in the coming months with upwards pressure on the yen not seen easing up, barring any intervention. The PMI did indicate that the sector contracted at a slower pace overall but still, it doesn’t paint an optimistic picture for Japanese manufacturing.

The below chart shows the moves in USDJPY (purple) against the manufacturing PMI (orange) over the last year. While this doesn’t necessarily suggest that a stronger yen is responsible for the decline in the PMI, it does suggest that, over the last year at least, there may be a relationship between the two.

Source – Thomson Reuters Eikon Terminal

In Europe we saw only a marginal upward revision to the German data from the preliminary release, which helped drive a similar revision in the eurozone figure. The U.K. manufacturing sector is worse off than the preliminary release indicated, with the number falling back to 48.2, rather than 49.1 a couple of weeks ago. It seems the services industry isn’t the only one that had a very negative knee jerk reaction to Brexit. It will be interesting now to see whether this eases up in the coming months as the dust settles or if sentiment continues to deteriorate ahead of article 50 being triggered.

EUR/USD – Euro Yawning, PMIs Meet Expectations

Next up we’ll get two readings from the U.S., the final official reading and the ISM number. Both numbers are expected to point to moderate growth in the sector, despite the Brexit vote which has dampened economic sentiment globally. Earnings will remain in focus this week although there are less companies due to report as we move towards the back end of the season. Eleven S&P 500 companies are scheduled to release second quarter results today.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Craig Erlam

His views have been published in the Financial Times, Reuters, The Telegraph and the International Business Times, and he also appears as a regular guest commentator on the BBC, Bloomberg TV, FOX Business and SKY News.

Craig holds a full membership to the Society of Technical Analysts and is recognised as a Certified Financial Technician by the International Federation of Technical Analysts.

Latest posts by Craig Erlam (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024