The US dollar has been on a decent run over the last month but there are reasons to believe it doesn’t have the legs to continue its ascent for much longer, not in the short term anyway.

Ultimately, a lot of people are in agreement that the greenback is likely to be one of the better performing currencies in the longer term. Its central bank is the only one of the majors in a tightening cycle and while it may have got off to a stuttering start, it’s likely to pick up the pace of rate hikes this year.

That said, the Fed has gone from failing miserably to convince market participants that we’d see three hikes last year – investors correctly anticipated only one – to getting them largely onside at the start of the year, to the two now largely being in agreement.

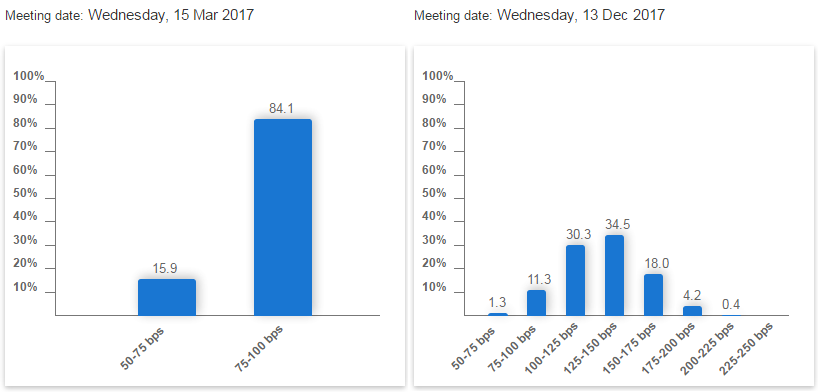

As of today, the implied probability of a rate hike in March are 84% – up from less than 20% only a few weeks ago – while the probability of three rate hikes in December is up to 57%.

Source – CME Group FedWatch Tool

With the markets so on side with the Fed, barring a faster pace of expected tightening than the central bank currently anticipates, the upside based on interest rate expectations may be fairly limited in the short term (of course, the economy running hot would likely change this).

It’s also worth noting that on the first two occasions the Fed raised rates in this tightening cycle, we saw an initial pop in the dollar, followed by a few more attempts to break higher – which is did, marginally – followed by a correction. Could we see the same again in the coming weeks?

GBP/USD – Steady as Dollar Quiet at Start of Week

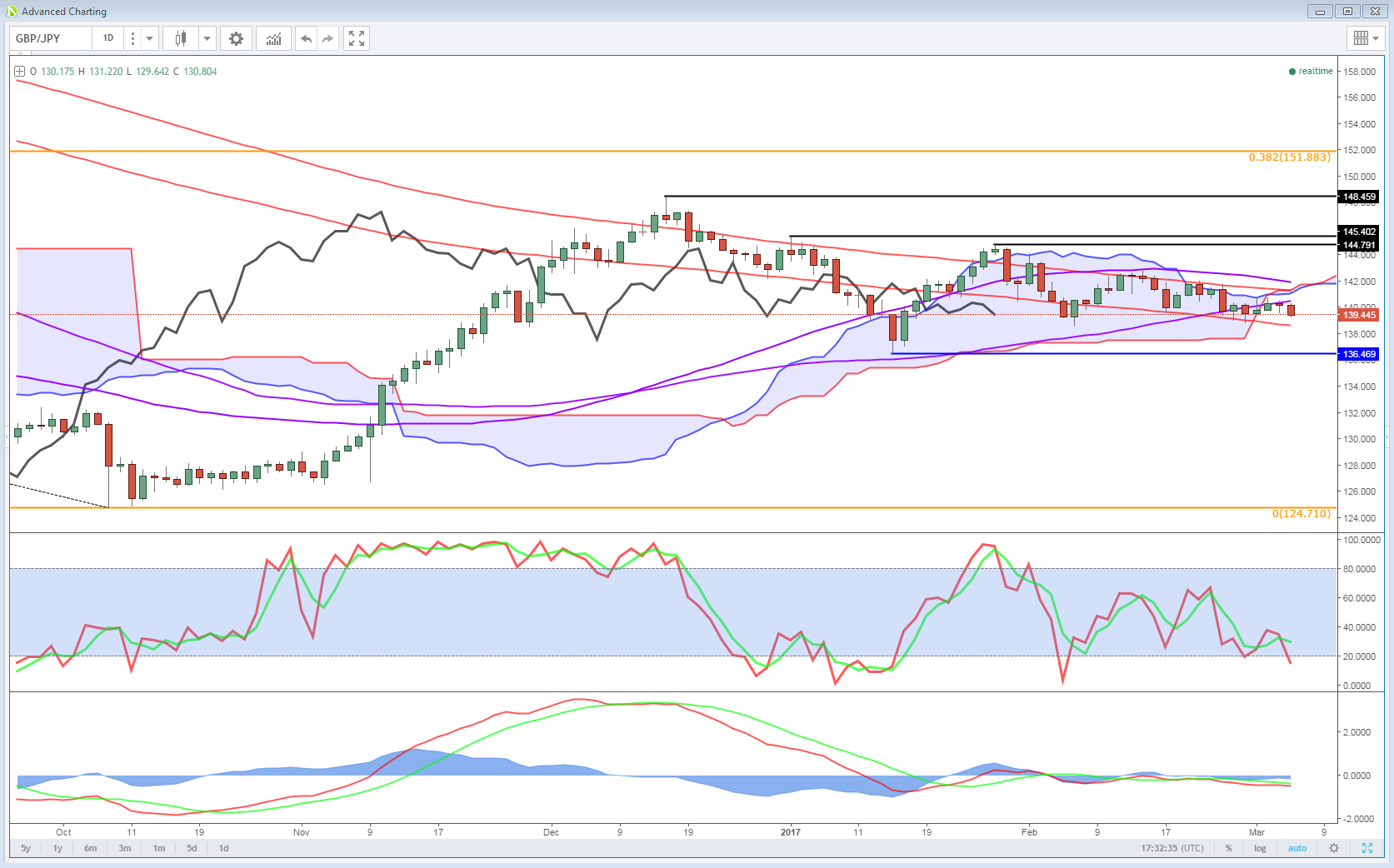

The charts may support this near-term view. Take the USDJPY, this pair pitches a central bank that’s intent on tightening against one that’s determined to keep rates extremely low. And yet, we could be about to break below the Ichimoku cloud on the daily chart, a move that would knock the pair into bearish territory.

OANDA fxTrade Advanced Charting Platform

Since the dollar’s resurgence at the start of February, it has at times made some decent gains against the yen but each time it’s been pushed back again, with support coming around 111.50. Throughout this time, it’s also made a worrying series of lower highs, a technically bearish signal as it prepares for its first big test of cloud support.

What’s more worrying for this pair – and may be more indicative of the real reason behind what continues to drag it lower – is that both sterling and the euro have already crossed the cloud threshold. This begs the question, is this a dollar move or a yen one? Perhaps it’s both, but I suspect it’s probably more so the latter. There is other evidence of underlying risk in the market, just look at Gold since the start of February, not exactly consistent with an appreciating dollar.

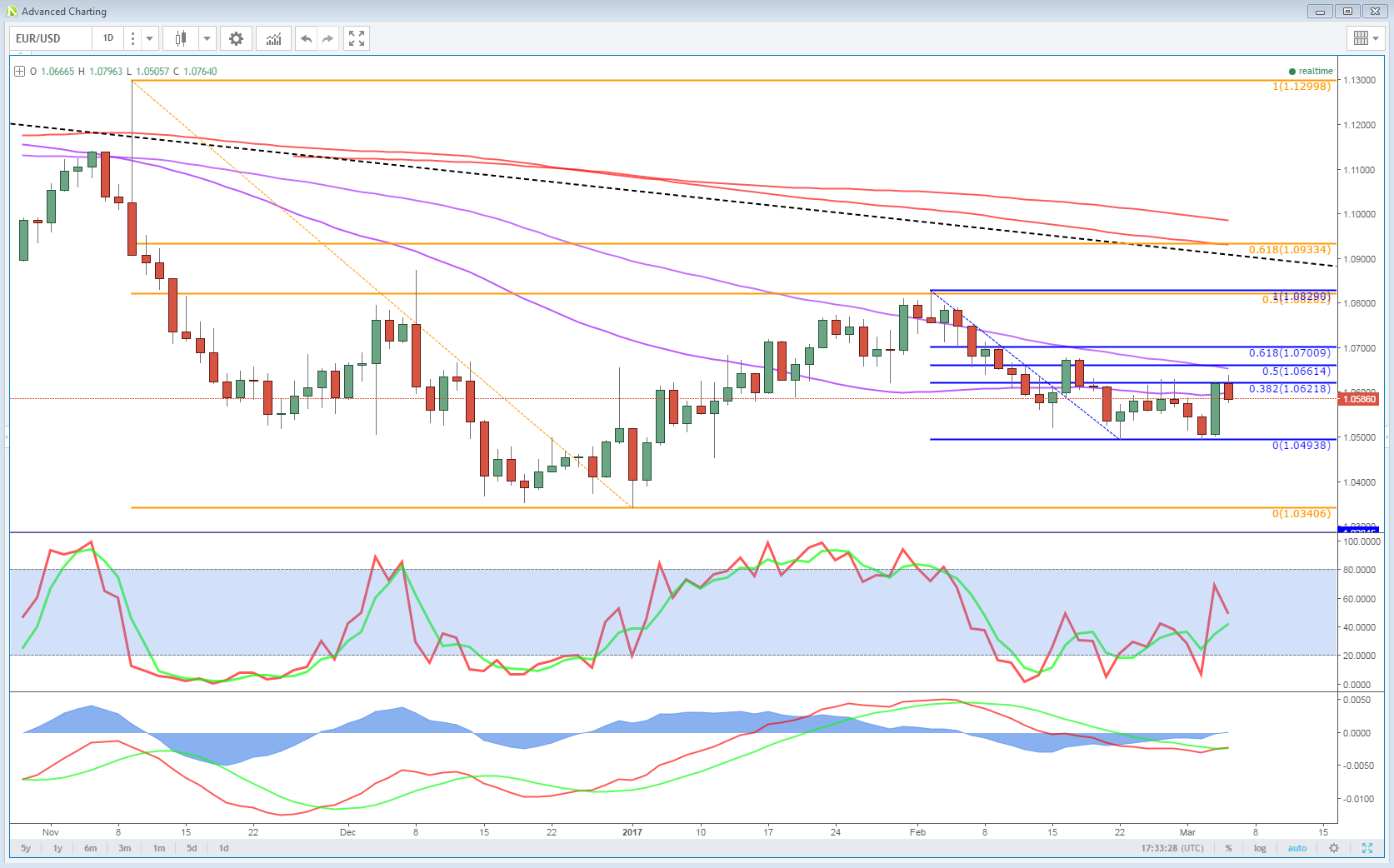

But the dollar is also running into a barrier against the euro, where 1.05 continues to provide a floor. Of course, it should be noted that we have also seen a series of lower highs here as well so momentum remains with the bears but for now, there continues to be bullish appetite. A close above 1.0630, which would break the double bottom neckline, could be the trigger for a break of this series of lower highs.

Then we look at the commodity currencies and the greenback is running riot, particularly over the last week or so, not exactly consistent with what we’re seeing above. Perhaps we can put this down to softer commodity prices, with oil looking toppy, Gold undergoing a correction and copper coming under pressure.

Lower China Growth Spooks Markets

So what does this all mean? Put simply, the outlook for the dollar may be bullish in the longer term but in the near term, it may come under some pressure, particularly against certain currencies. And should we get a rate hike next week, while the dollar may be supported in the short-term, this hasn’t lasted on the last two occasions. Will this time be different?

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Craig Erlam

His views have been published in the Financial Times, Reuters, The Telegraph and the International Business Times, and he also appears as a regular guest commentator on the BBC, Bloomberg TV, FOX Business and SKY News.

Craig holds a full membership to the Society of Technical Analysts and is recognised as a Certified Financial Technician by the International Federation of Technical Analysts.

Latest posts by Craig Erlam (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024