Risk aversion is rife once again in the markets on Thursday, with the brewing political storm surrounding President Donald Trump in the US largely being blamed for the moves.

Europe playing catch up but US facing another tough session

Europe is partly playing catch up today, with indices deep in negative territory, but sentiment is far from improved, as seen by US futures which are pointing to another rough open. Prior to yesterday’s open, major indices in the US were trading very close to their record highs, levels that have only been achieved on the belief that Trump will deliver on his tax reform and spending pledges. While I don’t believe at this stage that these reports regarding Trump will jeopardise his agenda, markets must reflect the challenges he now faces which ultimately make it more difficult. At the very least, this distraction may delay the implementation of his plans which the markets won’t like.

DAX Slips as Trump Crisis Spooks Markets

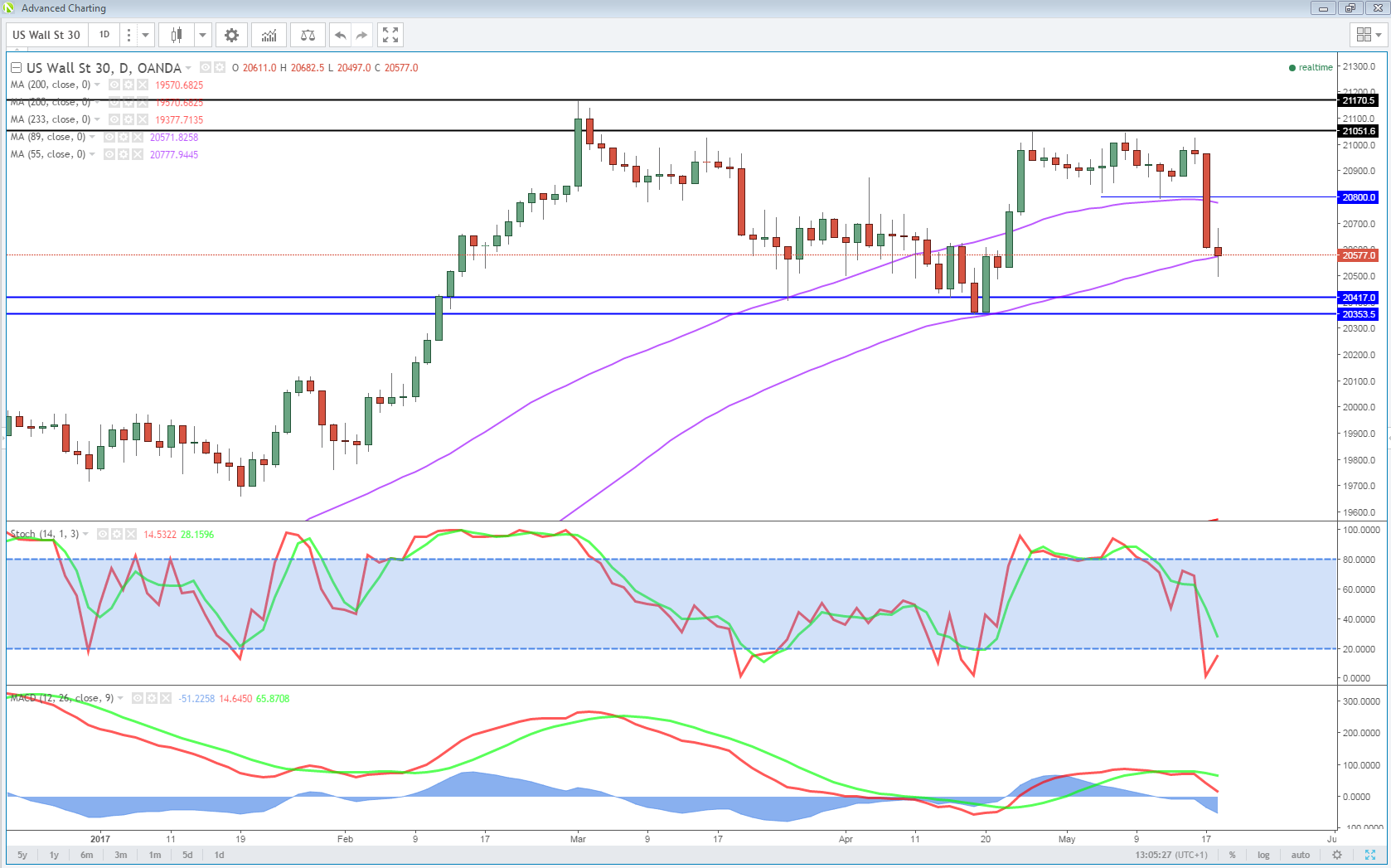

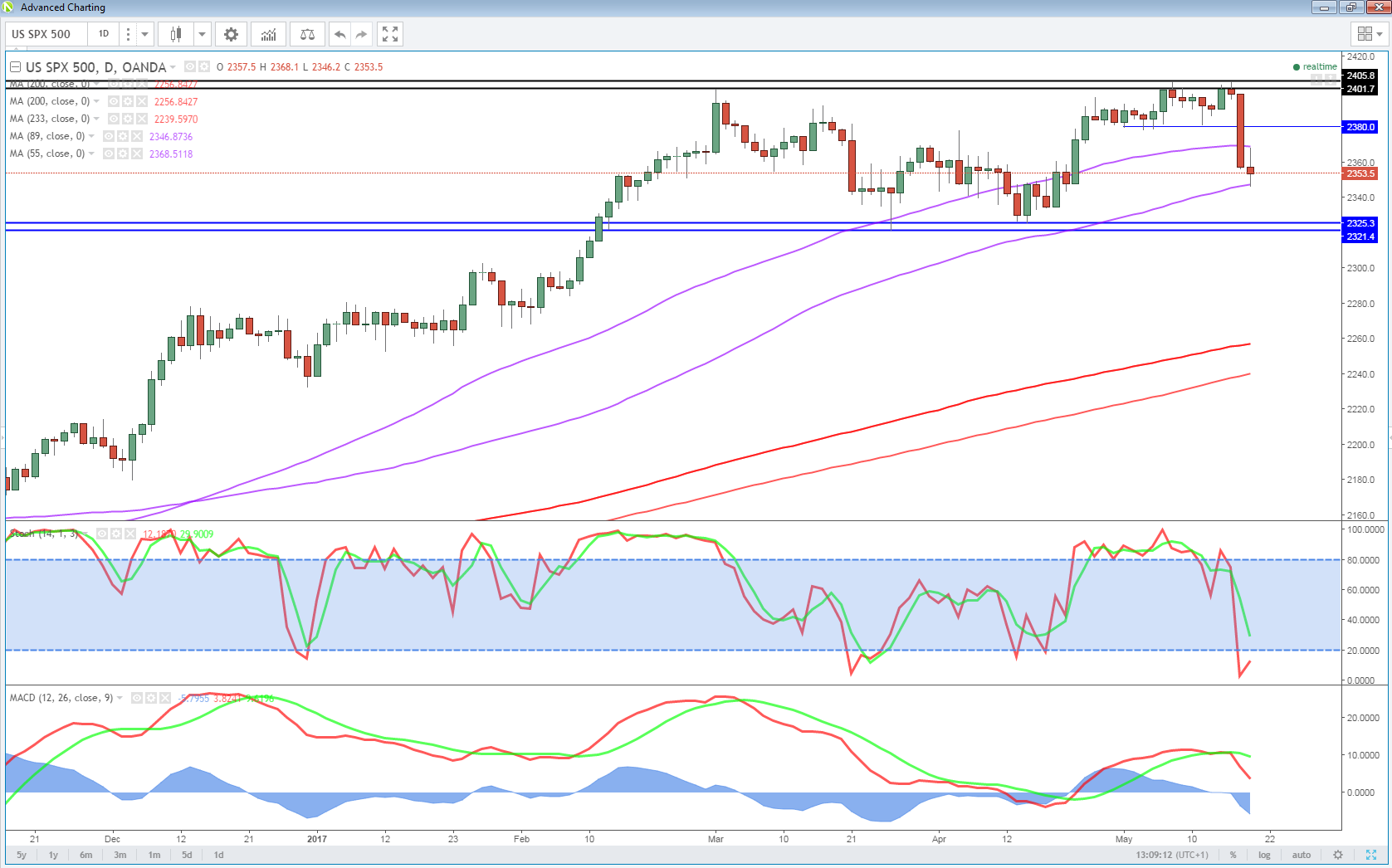

While the sell-off in risk markets is largely being attributed to the political circus in the US, I do think there’s a technical element at play here as well. Prior to yesterday, the S&P had traded in a tighter range for the last few weeks between 2,380 and its highs, while the Dow had done similar between 20,800 and its highs.

OANDA fxTrade Advanced Charting Platform

A break below these levels has likely triggered more selling which has contributed to the fear that we’re currently seeing in the markets. As long as the S&P stays above 2,320 and the Dow above 20,350 – meaning both indices remain in their three month ranges – then I don’t think there’s anything to be concerned about. As long as this remains the case, it would suggest that what we’re seeing is nothing more than consolidation while we await further progress on taxes and spending. A break below here may signal something more concerning.

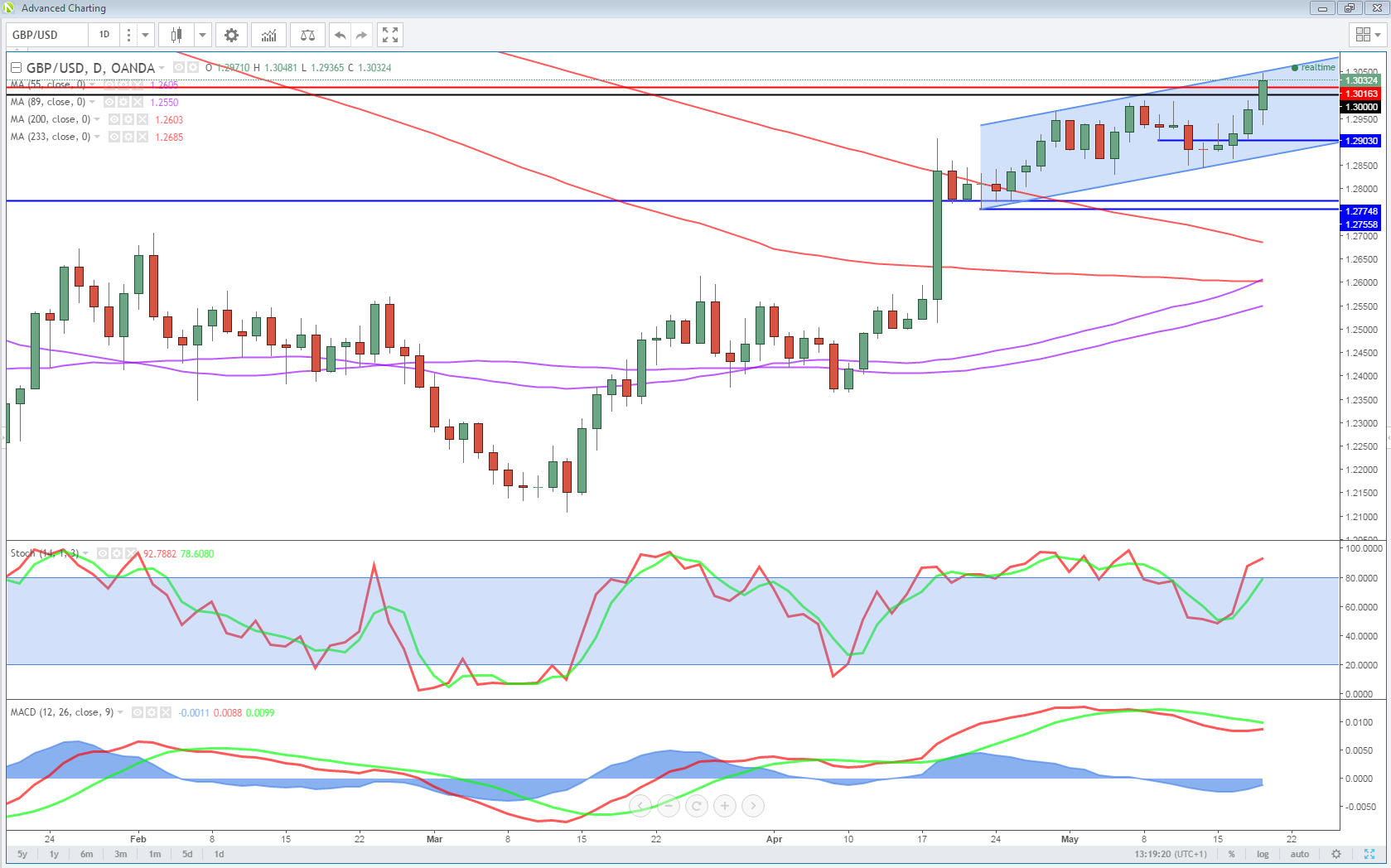

UK retail sales rebound strongly in April sending GBPUSD above 1.30

It’s not all bad news today, particularly for the UK which has already had a mixed bag of numbers this week. Yesterday we learned that while unemployment has fallen to its lowest level in more than 40 years, wages are falling in real terms thanks to subdued wage growth and higher inflation. Today we got the latest retail sales report which comes following the worst quarter of spending since 2010. Not only did we see a rebound in April but it would appear the nicer weather sent people to the shops in droves, with sales rising 2.3% from March – more than double what was expected – and 4% from a year ago. While these numbers will come as a relief, I don’t think one good month in isolation is worth getting carried away with, not given the near-term outlook for real wage growth and the impact that often has on spending.

Lame Duck Scenario has Dollar on Defense

Still, the numbers did give a boost to the pound which has seen it break above 1.30 against the dollar for the first time since September last year. Should the pair hold above here today, it could signal significant further upside in the pair in the coming weeks and months. Of course, sterling is always going to be vulnerable to Brexit related news, but should we see a calm few months on this front and the data continue to perform relatively well, then we could see the pair trading back toward 1.35. Of course, this will also depend on how things develop in the US and whether the Fed follows through on rate hike plans, but there’s certainly scope for upside in the pair which prior to this was pricing in a relatively dire scenario in the UK and quite the opposite across the pond.

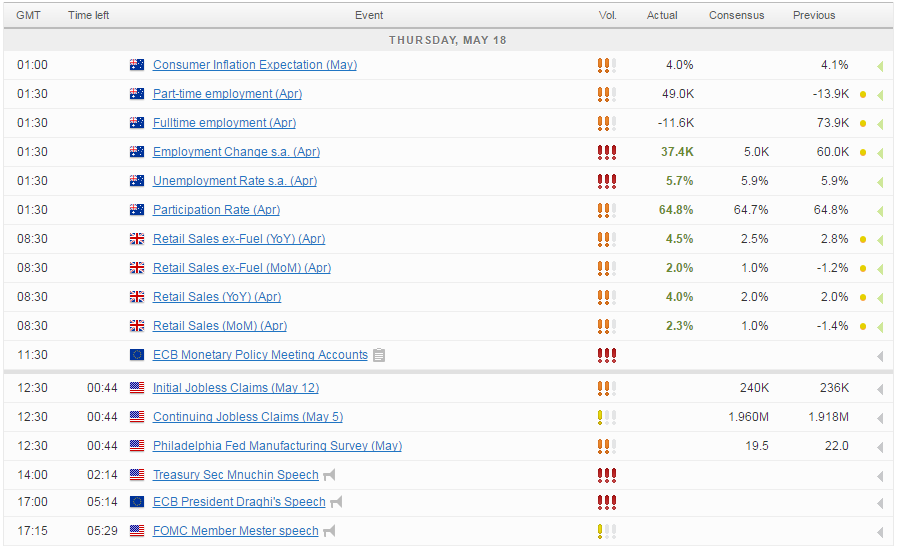

The focus today is likely to remain on developments relating to Trump. On the data side we’ll get jobless claims from the US, while ECB President Mario Draghi is due to speak, as is the Fed’s Loretta Mester, a voter on the FOMC in 2018.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024