Monday September 17: Five things the markets are talking about

The possibility of a new round on tariffs on Chinese goods is not helping equity markets this Monday morning. The ‘big’ dollar is holding onto Friday’s gains as investors try and acclimatize themselves to the ever-fluid trade situation that President Trump seems to be creating himself.

Deflection or negotiation, whatever the reason, markets continue to wait for the counter punch before throwing all in. China is not expected to be a willing dance partner in proposed trade talks later this month if the Trump administration goes ahead with the additional tariffs expected later today.

Note: Tariff level likely to be around +10%, and below the +25% previously announced.

Last week, the outlook for global trade looked improved, however, true to form, inconsistency seems consistent with this Trump administration.

This week, on the central bank front, the Bank of Japan (BoJ) dominates proceedings (Sept 18). However, recent domestic data remains mixed – Q2 GDP was revised upward while monthly core-machine orders rebounded from June’s decline and PPI edged downward – and certainlgly disappointing news to Governor Kuroda’s inflation fight.

On tap: AUD monetary policy minutes (Sept 17), BoJ rate announcement (Sept 18), U.K CPI and NZD GDP (Sept 19), SNB monetary policy decision & U.K retail sales, CAD retail sales (Sept 21)

1. Stocks see mostly red

The Nikkei 225 was closed for a bank holiday.

Down-under, Aussie stocks were the best performer in the region, as other Asia-Pacific indexes struggled with Sino-U.S trade worries. The ASX 200 rose +0.3% as energy and financial stocks logged solid gains and telecom rallied +1.5%. The negatives were elder care providers due to a planned government probe into the sector. In S. Korea, the Kospi closed down -0.66% on global trade worries.

Stocks in Hong Kong finished lower while China’s main Shanghai Composite index fell to its lowest close in four-years overnight on fears that Washington is expected to unveil new tariffs on imported Chinese goods this week.

In Hong Kong, the Hang Seng index ended -1.3% lower, while the China Enterprises index closed down -1.1%. In China, the Shanghai Composite index dropped -1.1%, while the blue-chip CSI300 index also declined -1.1%.

In Europe, regional bourses reverse earlier losses to trade mostly unchanged after weakness in Asia.

U.S stocks are set to open in the ‘red’ (-0.1%)

Indices: Stoxx50 +0.1% at 3,348, FTSE -0.2% at 7,291, DAX -0.2% at 12,100, CAC-40 flat at 5,351; IBEX-35 +0.6% at 9,417, FTSE MIB +0.7% at 21,019, SMI -0.3% at 8,936, S&P 500 Futures -0.1%

2. Oil higher as U.S Iran sanctions raise supply concerns, gold higher

Oil prices remain better bid as the market focuses on the potential impact of U.S sanctions on Iran despite promises by Washington that the Saudis, Russia and the U.S could together raise output fast enough to offset falling supplies.

Brent crude oil is up +45c a barrel at +$78.54, while U.S light crude (WTI) is up +43c at +$69.44.

Note: Washington aims to cut Iran oil exports to force Tehran to re-negotiate a nuclear deal. Iran exports have declined by -580k bpd in the past 90-days.

On Friday, U.S Energy Secretary Rick Perry said that he did not expect any price spikes and that the world’s top three oil producers could raise global output in the next 18-months.

Also capping oil prices, U.S drillers added two oilrigs in the week to Sep. 1, bringing the total count up to 749 according to Baker Hughes energy services.

Note: A Joint Technical Committee of OPEC and non-OPEC producers are due to meet today to coordinate production.

Ahead of the U.S open, gold prices have inched a tad higher as speculators look for short-term gains, amid increasing Sino-U.S trade tensions and prospects of further Fed interest rate hikes. Spot gold is up +0.2% at +$1,195.83 an ounce, after falling -0.6% on Friday when it marked its third straight weekly decline. U.S gold futures are down -0.1% at +$1,199.80.

3. Sweden’s Riksbank ready to hike despite low inflation

This morning minutes from Sweden’s Riksbank suggests that the board has become more tolerant of downside surprises to inflation and that it is now ready to hike rates before core-inflation has returned all the way to target.

Board members indicated that inflation expectations are “firmly anchored at the target, indicating that this is sufficient to start a very gradual tightening of the currently very expansionary monetary policy.” The bond market is pricing in a +25 bps hike in early Q1, 2019. The SEK is rallying, with EUR/SEK down -0.4% at €10.4774.

Elsewhere, the yield on U.S 10’s has fallen -1 bps to +2.99%. In Germany, the 10-year Bund yield is unchanged at +0.45%, while in the U.K, the 10-year Gilt yield has rallied less than -1 bps to +1.53%. The spread of Italy’s 10-year BTP’s over Bunds has narrowed -8 bps.

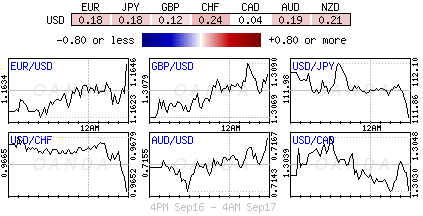

4. Sterling rallies on Irish border hopes

GBP (£1.3095) trades atop of the psychological £1.31 handle on optimism of progress on the Irish border question ahead of this week’s E.U summit.

E.U chief negotiator Michel Barnier is supposedly working on a plan to minimise physical checks at the Irish border by tracking goods using barcodes on shipping containers.

Note: The first of three Brexit summits will be held on Thursday, and E.U leaders hope a deal can be struck within the next two months.

EUR/USD (€1.1636) little changed. The ‘big’ dollar is expected to remain contained this week due to the absence of Tier 1 U.S data releases, while EUR gains may be capped on ongoing Italian concerns.

Emerging market currency’s trade under pressure once again on tariffs threats, with the USD/TRY over +1.6% ($6.2554) higher, while the USD/INR is +0.8% higher as the Reserve Bank of India (RBI) plans over the weekend to curb INR’s fall fail to lift the rupee.

5. Annual inflation down to +2.0% in the euro area

Data this morning from Eurostat showed that the euro area (19 members) annual inflation rate was +2.0% in August, down from +2.1% in July. A year earlier, the rate was +1.5%.

For the European Union (28 members) annual inflation was +2.1% in August, down from +2.2% in July. A year earlier, the rate was +1.7%.

Digging deeper, the lowest annual rates were registered in Denmark (+0.8%), Ireland and Greece (both +0.9%). The highest annual rates were recorded in Romania (+4.7%), Bulgaria (+3.7%), Estonia (+3.5%) and Hungary (+3.4%).

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019