Monday December 3: Five things the markets are talking about

Global equities have rallied overnight, alongside U.S Treasury yields, while the ‘big’ dollar trades under pressure after the U.S and China declared a temporary truce in their Sino-U.S trade war.

No progress was made on key differences regarding intellectual property and forced technology transfers. The U.S was promised to see China buying more goods to narrow the trade gap, while China received reprieve on increased tariffs for the time being.

Crude oil has rallied on optimism OPEC+ will address a glut in global supply later this week, while the EUR has found some support on news that the Italian government may accept a lower deficit target.

This week there are three central bank meetings; the Reserve Bank of Australia (Dec 3), the Reserve Bank of India (Dec 5) and Bank of Canada (Dec 5) will hold policy meetings. Market consensus expects the respective policies to remain unchanged.

Elsewhere, there is also a slew of updated economic data including final manufacturing, services and composite PMI’s for last month. Down-under, Australia will deliver Q3 GDP, while on Wednesday Fed chair Powell is expected to testify on “The Economic Outlook” before Congress’s Joint Economic Committee (tentative).

On tap: U.S financial markets will close on Wednesday (Dec 5) for a national day of mourning to honour former President George H.W. Bush.

1. Stocks rally hard

The truce between the world’s two largest economies at the G20 summit in Argentina on the weekend has gone some way in calming investor fears over the state of global growth.

In Japan, the Nikkei surged to a six-week high overnight after the U,S and China suspended the imposition of new tariffs and agreed to try to reach a trade deal within three months. The index share average rallied +1.0%, the highest closing level since Oct. 22. The broader Topix rallied +1.3%.

Down-under, Aussie stocks tracked global gains on the Sino-U.S truce pact. The S&P/ASX 200 index rallied +1.8%, posting its best intraday gain in 15-months. The benchmark index finished -1.6% lower on Friday. In S. Korea, the Kospi closed +1.67% higher, supported by tech giant Samsung and other large caps.

In China, stocks, commodities and the yuan currency surged even as uncertainty remained about the deal. The benchmark Shanghai Composite index closed +2.6% higher and the blue-chip CSI300 index rallied +2.8%. Both posted their best daily gains since Nov. 2.

In Europe, regional indices trade sharply higher following G20 summit agreements. On the corporate front shares of oil and automobile giants trade higher on President Trump’s tweet that China agreed to reduce and eliminate tariffs on U.S made cars.

On Wall Street, futures point to an opening gain of +1.8% for the S&P 500 and +1.9% for the DJ Industrial Average.

Indices: Stoxx600 +1.92% at 364.08, FTSE +2.25% at 7,137.18, DAX +2.61% at 11,550.95, CAC-40 +2.04% at 5,105.39, IBEX-35 +1.72% at 9,234.00, FTSE MIB +2.18% at 19,607.50, SMI +1.68% at 9,152.60, S&P 500 Futures +1.8%

2. Oil surges +5% on trade truce, gold higher

Oil prices jumped by more than +5% after the Sino-U.S 90-day trade truce, and ahead of this week’s OPEC+ meeting (Dec 6), where producers are expected to cut supply.

Brent crude has rallied +5.3% or +$3.14 to a high of $62.60, while U.S light crude oil rose +$2.92 a barrel to a high of +$53.85, up +5.7%, before easing to around +$53.00.

The U.S/China trade war has weighed heavily on global trade and has generated concerns of an economic slowdown. Despite oil not been included in the list of products facing import tariffs, the market sees the positive sentiment of the truce.

Oil also received support from Canada, where Alberta indicated that it would force producers to cut output by -8.7%, or -325Kbpd, to deal with a pipeline bottleneck that has led to crude building up in storage.

OPEC+ will meet on Dec. 6 to decide output policy. The group, along Russia, is expected to announce cuts aimed at reining in a production surplus.

Note: Qatar indicated this morning that they would leave OPEC in January – their oil production is only around +600K bpd, but it is the world’s biggest exporter of liquefied natural gas.

Ahead of the U.S open, gold prices have hit a three-week high on a weaker dollar, as a trade ceasefire between the U.S and China revived investor demand for riskier assets. Spot gold has climbed +0.7% to +$1,230.78 per ounce. U.S gold futures are up +0.8% at +$1,235.2 per ounce.

3. Budget compromise hopes push Italian yields lower

Italy’s borrowing costs fell to their lowest level in two-months earlier this morning after a number of reports that Italy is negotiating with the E.U to reduce its 2019 target for the budget deficit to +2.0% of GDP.

Also, demand for riskier assets, like Italian BTP’s, was supported by the weekend’s Sino-U.S trade truce. That in turn dented safe-haven German debt, with 10-year yields pulling away from their three-month print last week.

Ten-year Italian bond yields fell -6 bps to a two-month low at +3.15%. That narrowed the gap over benchmark German Bund yields to around +279 bps — its’ tightest in two-months.

Elsewhere, Germany’s 10-year Bund yield has backed up +2 bps to +0.33%, the largest advance in a week. The yield on U.S 10-year note has rallied +5 bps to +3.04%, the biggest increase in a month. In The U.K, the 10-year Gilt yield has climbed +2 bps to +1.381%, the first advance in a week.

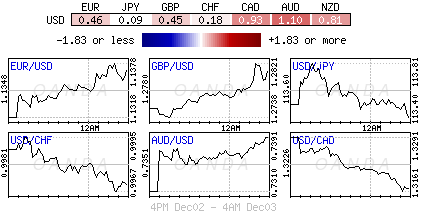

4. For now, dollar under pressure

The U.S dollar is under pressure following the breakthrough in trade talks between the world’s two largest economies over the weekend as the market opts to take on more risk.

U.S dollar ‘bears’ will remain wary of a sustained breakthrough in trade tensions that could encourage the Fed to deliver more monetary tightening next year.

Sterling briefly traded above £1.28 before fading down -0.37% to £1.2731. The balance of risks for the pound remains skewed to the downside in the near-term, as Brexit uncertainty is set to remain elevated.

Note: U.K Politicians have signed a letter arguing the government was in contempt of parliament for not publishing the AG Cox’s legal advice pertaining to the Brexit agreement.

The EUR (€1.1350) trades over +0.2% higher as overall risk-on dominates for now, as well as Italian Budget deficit target compromise is helping to lift the pair. The Japanese yen has climbed +0.1% to ¥113.45, the strongest in more than a week.

5. U.K man-PMI leaves Brexit driven pound under pressure

The pound stays atop of its intraday lows despite the U.K manufacturing purchasing managers’ survey for November rising to a two-month high of 53.1 from October’s 27-month low of 51.1.

Brexit worries continue to weigh on the currency and with that, economic data takes a backseat in terms of importance.

Presently, the fate of the pound now rests on the U.K vote on Brexit next week (Dec 11) rather than on fundamentals.

IHS Markit stated, “the performance of the sector remained comparatively lacklustre, with the latest PMI reading still among the weakest registered over the past two-and-a-half years.”

Elsewhere, European PMI’s were mixed, France, Spain, Germany among those which beat forecasts, while Italy misses, reaching an almost four-year low.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019