Jerome H. Powell took office and began his four-year term as Chairman of the Board of Governors of the Federal Reserve System on February 5, 2018. He has delivered three rate increases since taking the lead post and has continued unwinding the Fed’s balance sheet. Since the November meeting, the US economy has still generated good, albeit softer data, but the risks to the economy have grown. This by far will be his most difficult decision as the Fed has been very clear in signaling a December hike is coming and market expectations are for him to lower the dot plot forecast.

- Will the Fed deliver the highly anticipated dovish hike?

- How low can oil go?

- Canadian inflation expected to decline

Neutral Mistake

On October 3rd, Powell said that the Fed “may go past neutral. But we’re a long way from neutral at this point.” That comment ended the bull market run with US equities. Powell’s pivot eventually occurred at the NY Economic Club on November 28th. He stated that interest rates are “just below” a range of estimates of the so-called neutral level. Equities rebounded as Powell appeared to have taken his foot off the interest rate accelerator. Equities however resumed their bearish correction as slower growth globally and concerns of the shrinking balance sheet could pull liquidity from money markets during a weakening economy.

Interest Rate Decision

The probability that the Fed will raise the funds target range by 25 basis points, is no longer a slam dunk. At the end of Tuesday, expectations hovered around two-thirds, well off the 80% certainty we saw at the end of November. They will probably deliver a rate hike, but if they didn’t, we should not be surprised. The Fed historically does not like to raise rates during extreme periods of market turmoil. Another option for the Fed would be to say that rates are at neutral, however this unlikely to happen.

Dot Plot Expectations

The September FOMC Economic Projections targeted three hikes in 2019 and two in 2020. The market is widely expecting them to reduce the forecast in 2019 to only two hikes, with some analysts’ expecting one hike. The Fed could also cut the outlook for 2020 and 2021. The market is highly pricing in a dovish hike and it is unlikely that it will be as dovish as expected.

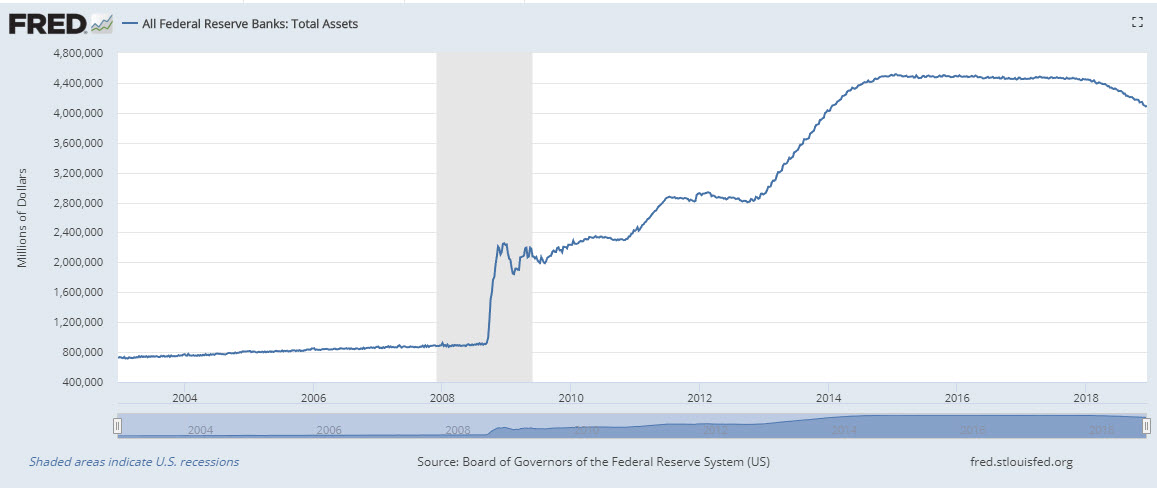

Balance Sheet

The Fed began shrinking its balance with Janet Yellen back in October of 2017. It has been lowered from around $4.51 trillion to $4.14 trillion. The current tightening schedule has been removing $50 billion of Treasury and mortgage-backed securities holdings on a monthly basis. We have not heard of a specific target from the Fed, but Powell did state during his confirmation hearing last year the balance sheet could target $2.5 to $3 trillion. Most analysts currently see the balance sheet settling between $3.5-$3.8 trillion. The Fed may provide some clarity on economist concerns of the effects of pulling liquidity from a softening economy.

Trump & Central Bank Independence

President Trump has been very vocal on discouraging the Fed from raising interest rates. However, his comments may actual drive the Fed to actual raise rates to assert its independence.

This week the President has tweeted the following:

“I hope the people over at the Fed will read today’s Wall Street Journal Editorial before they make yet another mistake. Also, don’t let the market become any more illiquid than it already is. Stop with the 50 B’s. Feel the market, don’t just go by meaningless numbers. Good luck!”

It is incredible that with a very strong dollar and virtually no inflation, the outside world blowing up around us, Paris is burning and China way down, the Fed is even considering yet another interest rate hike. Take the Victory!

What could we expect?

A dovish hike is firmly expected since the outlook is weaker and market sentiment is deeply negative. The Fed is also expected to remove the statement that “further gradual increases” in rates are likely to be required. The Fed’s dot plots should come down, with 2019 falling from three hikes to two. The 2020 and 2021 dots could also come down with the longer run outlook also falling. The Fed is likely to emphasize being data dependent. The US dollar will likely react to how much the forecasts change. If the Fed does not provide any major downgrades to the dots and highlights the strong labor market, rising wages, and inflation near their target, the dollar could climb higher. If the Fed is successful in providing a clear dovish tone with lower projections, we could see high-beta currencies rally.

Oil’s Sell-off Accelerates

The fundamentals for oil remain very bearish. One day oil is lower on global growth concerns, the next day it falls on supply worries, and sometimes it drops on a risk off trading day. US West Texas Intermediate crude is now at 15-month lows after falling below the $50 a barrel level. OPEC and allies have now seen their production cut completely wiped out. The $42 level remains major support for oil.

Canada’s inflation data in focus

Inflation expectations for the November readings are expected to decline. The annual reading is expected to fall from 2.4% to 1.8% and the monthly reading from 0.3% to -0.4%. The Bank of Canada has already warned that rate hikes could be interrupted and if we see inflation fall below the 2% target, that could help keep BOC on hold.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Ed Moya

His particular expertise lies across a wide range of asset classes including FX, commodities, fixed income, stocks and cryptocurrencies.

Over the course of his career, Ed has worked with some of the leading forex brokerages, research teams and news departments on Wall Street including Global Forex Trading, FX Solutions and Trading Advantage. Prior to OANDA he worked with TradeTheNews.com, where he provided market analysis on economic data and corporate news.

Based in New York, Ed is a regular guest on several major financial television networks including CNBC, Bloomberg TV, Yahoo! Finance Live, Fox Business, cheddar news, and CoinDesk TV. His views are trusted by the world’s most respected global newswires including Reuters, Bloomberg and the Associated Press, and he is regularly quoted in leading publications such as MSN, MarketWatch, Forbes, Seeking Alpha, The New York Times and The Wall Street Journal.

Ed holds a BA in Economics from Rutgers University.

Latest posts by Ed Moya (see all)

- Market Insights Podcast – Powell struggles to deliver a hawkish hold - 1 November 2023

- Fed React: USD/JPY softer after Fed fails to deliver hawkish hold - 1 November 2023

- EUR/USD: Dollar wavers on slower pace of Treasury Refunding Sales and mixed labor data - 1 November 2023