Monday March 18: Five things the markets are talking about

Global equities start Monday on the front foot in a week that is packed with geopolitical (Brexit, E.U summit – Mar 21/22), economic releases and central bank meetings (FOMC, BoE, SNB), events that are expected to have a significant impact on both markets and volatility.

Last week, U.K parliament rejected for the second time PM May’s exit deal and also voted to delay the final Brexit deadline, currently set for March 29. However, any extension needs to be agreed by all 27 EU member governments. Nevertheless, May is expected to put ‘her’ withdrawal agreement to a third vote, as early as tomorrow, only if she’s able to incite consensus amongst her party.

On the central banks front, the Fed (Mar 20), BoE and SNB (Mar 21) are all expected to sound ‘dovish’ when they make interest rate decisions. Fed officials are not expected to signal any appetite for rate increases this year and how long this pause will last is what the market is after. The BoE is likely to suggest interest rates staying put as Brexit uncertainty continues.

On the trade front the meeting between China President Xi and US president Trump is now delayed to June. Thus far, it has had little impact on markets.

On tap: RBA minutes (Mar 18), U.K average earnings (Mar 19), U.K CPI, FOMC monetary policy meeting, U.K Brexit vote, NZD GDP, Japan bank holiday & AUD employment (Mar 20), SNB monetary policy assessment, U.K retail sales & BoE monetary policy summary (Mar 21), EUR German flash PMI, CAD CPI & retail sales (Mar 22).

1. Stocks get the green light

In Japan, the Nikkei rallied overnight as chip-related stocks tracked their U.S counterparts higher, but weak February export data capped gains. The Nikkei share average ended +0.6% higher, while the broader Topix rose +0.7%.

Down-under, Aussie shares rose, as mining stocks tracked gains in iron ore prices after Brazil indicated it would cut output, although broader gains were capped by a jaded performance in bank stocks. The S&P/ASX 200 index closed +0.25% higher. The benchmark was little changed on Friday. In S. Korea, stocks rose for a third session, but the advance was modest. The Kospi only climbed +0.2% as index giant Samsung Electronics fell -1.1%.

In China, stock indexes closed atop of their six-month highs overnight, as sentiment was supported by an expected ‘dovish’ Fed stance this week and Beijing’s policy boost for growth. At the close, the blue-chip CSI300 index settled +2.9% higher, while the Shanghai Composite Index ended up +2.5%.

In Hong Kong, stocks tracked the mainland Chinese markets higher and closed at a nine-month peak. The Hang Seng index rose +1.4%, while the China Enterprises Index gained +1.5%.

In Europe, regional bourses trade mostly higher across the board tracking their Asian peers higher and mixed U.S Index futures this morning.

U.S stocks are set to open little changed (+0.0%).

Indices: Stoxx600 +0.15% at 381.66, FTSE +0.70% at 7,278.75, DAX -0.03% at 11,682.54, CAC-40 +0.08% at 5,409.55, IBEX-35 +0.40% at 9,379.81, FTSE MIB +0.61% at 21,173.50, SMI +0.01% at 9,484.20, S&P 500 Futures 0.00%

2. Oil prices caught between supply and demand constraints, gold higher

Oil prices are mixed, weighed down by concerns that an economic downturn may reduce fuel consumption, but supported by OPEC+ supply cuts and U.S sanctions against Iran and Venezuela.

Brent crude oil futures are at +$67.24 per barrel, up +8c from Friday’s close, while U.S West Texas Intermediate (WTI) futures are at +$58.43 per barrel, down -9c from their close.

OPEC announced this morning that’s it’s set to scrap its planned meeting in April and decide instead whether to extend oil output cuts in June – members want to be able to assess the full impact of U.S sanctions on Iran and the crisis in Venezuela.

OPEC and a group of 10 oil-producing nations led by Russia are deepening their crude production cuts but remain split on whether the curbs should remain in place through the end of the year. The next regular talks would be held on June 25-26.

Note: On Sunday, Saudi energy minister Khalid al-Falih said “the job of OPEC and its allies was not done yet” and indicated that the group of oil producers needed to “stay the course” at least until June when the current global supply cut agreement is due to expire.

Ahead of the U.S open, gold prices are a tad higher for a second consecutive session, as the ‘big’ dollar slipped after recent toned-down U.S data increased chances that the Fed will signal a ‘dovish’ policy stance this week. Spot gold has rallied +0.2% to +$1,303.92 per ounce, while U.S gold futures have gained +0.1% to +$1,303.80.

3. German Bund yields little changed ahead of summit

The German 10-year Bund yield is little changed ahead of this week’s critical EU summit (Mar 21/22), with UK PM May set for a visit to Brussels on Thursday to request an extension to Brexit negotiations beyond the scheduled departure date of March 29. Investors should expect headline noise to have an impact on yields. Trading atop of their record low yields, the danger remains to the upside in yield – on any sign for a benign exit plan. The yield on Germany’s 10-year Bund currently trades at +0.087%.

Elsewhere, the yield on 10-year Treasuries increased +1 bps to +2.59%, while in the U.K the 10-year Gilt yield advanced less than +1 bps to +1.214%. In Italy, the 10-year BTP yield is lower by -5 bps to test a fresh 10-month low around the +2.44%, on market relief that the credit rating agency Moody’s did not take any action on Italy late last week.

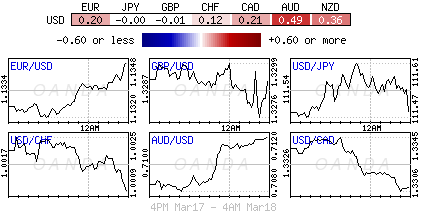

4. Sterling dips on Brexit concerns

GBP/USD is softer by -0.4% at £1.3238 as the market begins to focus on a possible third meaningful vote on PM May’s Brexit deal, which could happen tomorrow. PM May is trying to bring her already twice defeated “Withdrawal Agreement” back to the House of Commons. However, this move would depend on whether the Northern Irish DUP party agree to back it.

Sterling is under pressure with reports suggesting that the PM is unlikely to garner enough support to get her deal through Parliament.

What then? If the meaningful vote failed for a third time, it’s over to the EU at their council summit on Mar 21/22 to decide what length of extension they would offer the UK to Article 50 and what the conditions will be.

EUR/USD (€1.1339) trades atop of its fortnight high with focus now on the Fed. A “no change” in policy is expected and many expect the meeting should reinforce the message that the Fed would remain patient for the foreseeable future.

Note: German flash PMI is released on Mar 22.

With the Fed expected to reduce its forecasts for future interest-rate rises, investors should expect this to boost appetite for risk assets later this week, which could be positive for high yield and EM FX, while the ‘big’ dollar should be able to hold its own against low-yielding currencies.

5. Euro trade data

Data from Eurostat this morning showed that the EU’s trade surplus with the U.S and its deficit with China both increased in January, serving as potential fuel for trade conflicts between the world’s largest economies.

The EU surplus in goods trade with the U.S expanded to +€11.5B in January, from +€10.1B in January 2018, while with China, the EU deficit also increased to +€21.4B, from €20.8B a year earlier.

As a whole, the EU trade deficit in goods was -€24.9B in January from -€21.4B in January 2018. For the eurozone, its trade surplus dropped to -€1.5B from -€3.1B.

Note: President Trump has complained about Europe’s trade surplus, imposing tariffs to curb imports of EU steel and aluminum and threatening to do the same for the much larger trade in cars and car parts.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019