Monday May 6: Five things the markets are talking about

The latest U.S jobs report showed that hiring picked up in April, with the unemployment rate falling to its lowest level in 50-years. It gave a boost to major U.S stock indexes and weighed on the mighty U.S dollar and 10-year Treasury yields.

Nevertheless, a couple of Tweets from Trump over the weekend has managed to put global equities on the back foot, pressured Treasury yields even further and has investors seeking shelter by owning risk averse currencies.

President Trump is threatening to increase tariffs on Chinese imports – he planned to increase taxes on +$200B in Chinese imports to +25% from +10% starting Friday. He also plans +25% tariffs “shortly” on a further +$325B in Chinese goods – his threats are calling into question whether the next round of trade talks this week will be delayed.

Note: Chinese Vice-Premier Liu He is scheduled to arrive in Washington this Wednesday.

On the data front, Eurozone retail sales will start the week followed by German manufacturers’ orders and French merchandise trade. In the U.K, first-quarter GDP will be posted Friday. Down-under, Aussie trade and retail sales data will be posted early in the week followed by midweek policy announcement from the RBA amid expectations for no action. The RBNZ will also be issuing a statement this week. Chinese CPI data are also expected midweek.

Stateside, inflation will be the focus, but it will be late in the week, first producer prices on Thursday then a consumer price report on Friday that is not expected to show much acceleration. For Canada, housing starts will be posted on Wednesday, the trade balance on Thursday, and the labour force survey on Friday where a gain is expected.

On tap: JPY & GBP bank holiday, AUD retail sales and NZD (May 6), RBA & RBNZ monetary policy announcement (May 7), Fr. Bank holiday & NZD annual budget (May 8), CAD Trade balance & U.S PPI, RBA monetary policy statement (May 9), GBP GDP & CAD employment change (May 10).

1. Stocks in deep red

Global equities have plunged after the sudden intensification of Sino-U.S trade tensions, sowing fears the conflict could spill over into slower economic growth.

In Asia, both the Nikkei225 and the Kospi index were closed for a bank holiday. In Europe, the U.K was closed for the long weekend.

Down-under, Aussie shares closed atop a three-week low overnight after U.S’s threat to raise tariffs on Chinese goods spoiled hopes for an imminent trade deal between the world’s largest economies. Broad-based losses pushed the S&P/ASX 200 index -0.8% lower at the close of trade. The benchmark was little changed on Friday.

In China, investors were caught off guard by Trump’s tariff threats, but managed to dump equities and sell the yuan currency as a fresh deterioration in Sino-U.S trade tensions began. Regional bourses fell the most in more than three-years. The blue-chip CSI300 index and the Shanghai Composite Index both tumbled more than -5%. In Hong Kong, the Hang Seng index slumped -3.3%.

In Europe, regional indexes trade sharply lower across the board as U.S trade tensions weighs.

In the U.S, stocks are set to open deep in the ‘red’ (-1.8%).

Indices: Stoxx600 -1.54% at 384.34, DAX -2.13% at 12,148.00, CAC-40 -2.21% at 5,426.01, IBEX-35 -1.75% at 9,245.00, FTSE MIB -2.38% at 21,249.50, SMI -1.65% at 9,581.60, S&P 500 Futures -1.86%

2. Oil prices slump after Trump’s tariff threats, gold higher

Oil prices have tumbled overnight after Trump said he would sharply hike tariffs on Chinese goods this week, risking the derailment of trade talks between the world’s two biggest economies.

Brent crude oil futures fell below +$70 per barrel, trading at +$69.34 per barrel, down -$1.51, or -2.1% from Friday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$60.57 per barrel, down -$1.37 per barrel, or -2.2% from Friday’s close.

The prospect of months of trade talks being derailed by Trump has raised market concerns over future demand for oil.

Also providing pressure on prices is U.S data showing an increase in production. U.S crude production has already surged by more than +2M bpd since early 2018, to a record +12.3M bpd. This has made the U.S the world’s biggest producer. However, data from Baker Hughes Friday showed that the number of rigs drilling for gas in the U.S fell by -3 to +183 in the week to May 3, while oil-directed drilling rigs rose by +2 to 807.

Ahead of the U.S open, gold rallied overnight after U.S President Trump threatened to impose tariffs on Chinese goods, encouraging a sharp downturn in riskier assets. Spot gold is up +0.3% to +$1,282.96 per ounce, while U.S gold futures are up +0.2% to +$1,283.70 an ounce.

Note: Gold was in demand in India and Singapore last week as a correction in prices ahead of a key gold-buying festival supported purchases even as major centres were closed for most of the week due to holidays.

3. Yields plummet on safe haven buying

Core eurozone bonds yields fell after U.S President Trump said he would hike U.S. tariffs on +$200B worth of Chinese goods this week and target billions more soon.

German Bunds have risen sharply as investors buy safe haven assets. The Bund yield has fallen -2.5 bps to +0.004%. In France, the 10-year yield declined -2 bps to +0.348% on the biggest drop in more than a week, while down-under, Australia’s 10-year yield declined – 5 bps to +1.7395%.

The outlier this morning is Italian government bonds which have underperformed the rest of the Euro-periphery with renewed concerns about the stability of the Italian government. Italy’s anti-establishment 5-Star Movement raised pressure on its government partner to dismiss a junior minister under investigation for corruption.

Italy’s short-dated bonds are up +6 bps, while the spread of its 10-year debt over Germany widened to +260 bps.

In China, the PBoC cut the Reserve Requirement Ratio (RRR) for Small and Medium sized banks by up to -350 bps to +8.00% (effective May 15). Funds released would be used for lending to small and private firms.

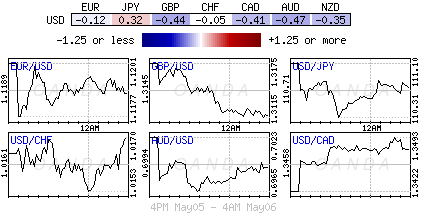

4. Safe haven currency flows dominate

Safe haven flows are dominating trading after Trump’s weekend tweets on China trade and planned implementation of tariffs.

EUR/USD is lower by -0.2% for the bulk of the session to trade around €1.1190 area.

GBP/USD is off -0.4% at £1.3120 area with cross party Brexit talks resuming tomorrow. Sterling is finding it difficult to build upon market optimism that a Brexit compromise seems to be taking shape and have the UK move forward with a plan to get a Withdrawal Agreement passed by Parliament.

USD/JPY is off -0.4% with Japan still on holiday. The yen currency (¥110.82) remained a beneficiary of safe-haven flows over trade concerns.

The Swiss franc is also rising, with EUR/CHF down -0.1% at $1.1375. The AUD is amongst the biggest fallers, given Australia’s close links to China, with AUD/USD down -0.7%, while emerging market currencies drop.

5. Euro moral improves

Data this morning showed that investor morale in the euro zone improved this month for the third month in a row to hit its highest level since last November, helped by a resilient global environment and the danger of a disorderly Brexit being averted until October.

The Sentix research group said that its investor sentiment index for the euro zone rose to +5.3 in May from -0.3 in April – the market was expecting a reading of +1.4.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019