- US Dollar Index rally continues and the impact of a strong US dollar on global markets.

- Examining upcoming PMI data from the Euro Area and UK CPI figures, and their potential market implications.

- Assessing the likelihood of further rate cuts by the Federal Reserve and the Bank of England.

- Providing insights on market trends and potential volatility in the coming week.

Read More: Trading USD/CHF: What to Expect After the US Dollar’s Multi-Month Highs

Week in Review: Soft Landing in Jeopardy?

A week that promised much is drawing to a somber close. Following two action packed weeks, this week which included US CPI and PPI data was muted in comparison. However, the week was not a waste by any means and provided some valuable insights while at the same time raising some key questions.

The biggest takeaway for the week is, whether or not a soft landing is still on the cards?

An uptick in PPI coupled with rising US Yields and stubborn CPI data have brought the question back to the fore.

In Q3, the chance of a soft-landing went up from 40% to 42%. At the same time, the likelihood of a recession dropped from 30% to 28%, and the chance of stagflation went down from 28% to 27%. The highest probability is for a soft-landing, meaning there’s a greater chance of steady growth over the next year.

The chances for different growth scenarios stayed mostly the same as last quarter. However, the election results have added uncertainty to the economic outlook, which might lead to changes in these chances going forward.

Given the comments by Fed Chair Powell and the history of the Fed, another monetary policy pivot in early 2025 is unlikely. Powell has made it clear that the Fed will gauge the impact of Government policy before making any decisions, which will mean a Q1 or potentially Q2 pivot remains unlikely as markets come to terms with a Trump return to the White House.

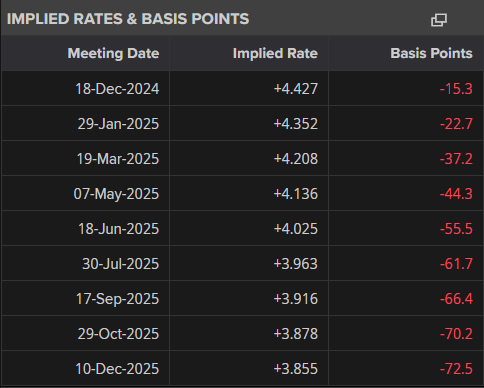

Taking into account all of the above however, market participants do not seem fazed by Fed Chair Powell’s comments. The probabilities and implied rates for 2025 remain muted with less rate cuts the base case, as market participants continue to see increased inflation in the new year. The impact of this continues to be felt by the US Dollar and US Yields in particular both of which have enjoyed bullish weeks.

Markets are now pricing in around 72 bps of rate cuts through December 2025, down from 77 bps on Wednesday. This was down to a rise in US PPI and strong retail sales and NY Fed manufacturing data. Adding fuel to this were some announcements by President elect Trump where he touted some key foreign policy positions to known China Hawks. This will no doubt exacerbate concerns of a more aggressive stance toward China and increase trade war concerns.

Moving forward, these developments might be more important than the pricing of the December meeting where the likelihood of a cut still remains above the 60% mark.

Source: LSEG (click to enlarge)

The surprise of the week came from US Indices with the SPX and Nasdaq 100 giving back the majority of its post election gains. The SPX and Nasdaq 100 are 2.03% and 3.17% down for the week at the time of writing.

The biggest winner of the week was the crypto space with Bitcoin (BTC/USD) roaring to fresh ATH highs around the $93k handle. Markets remain optimistic that President Trump will follow through on his pro-crypto stance with various opinions floating around.

Commodity markets came under strain again this week with rising yields and the DXY pushing Gold down to lows around $2536/oz, as much as 5% down for the week. Oil pisces also struggled to gain any favor as OPEC downgraded their forecasts for a fourth consecutive month. Brent was down around 3% for the week at the time of writing.

All in all a confusing week, one that is likely to keep markets guessing heading into a busy festive season.

The Week Ahead: Muted Week in APAC, PMI Data Rules

Asia Pacific Markets

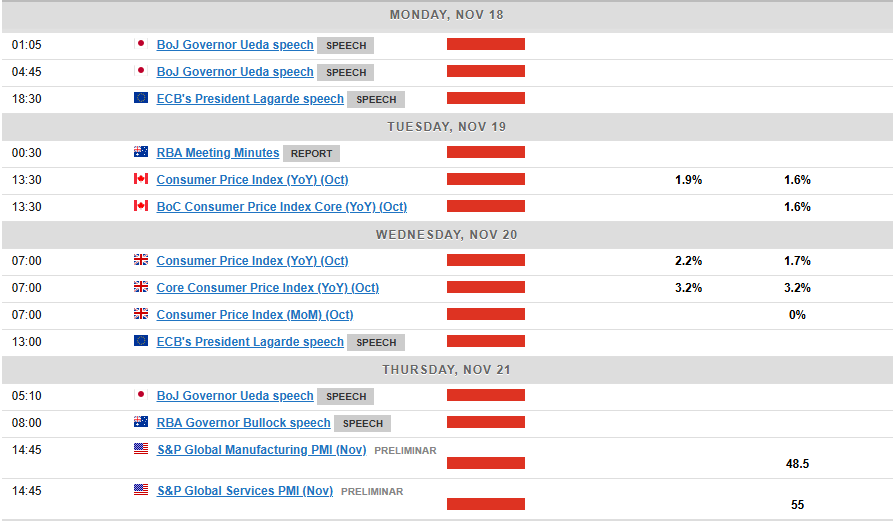

The week ahead in the Asia Pacific region will see a slowdown with a surprise meeting called by the Bank of Japan (BoJ) likely to be a highlight.

Japan’s data is likely to show that things are slowly getting back to normal after some temporary disruptions. This should lead to better PMI figures. The manufacturing PMI might stay below average, but the services PMI should improve thanks to temporary tax cuts and rising incomes.

Exports are expected to grow by 1.7% compared to last year, following a 1.7% fall in September, while imports might drop by 4.5% due to lower global commodity prices. Inflation is predicted to decrease to 2.3% compared to last year, mainly because of a high base from last year. However, monthly growth should rise to 0.6%, helped by the end of energy subsidies and strong price increases in services.

The surprise may come on Monday however, per a Reuters report BoJ Governor Ueda will deliver a speech and hold a news conference in Nagoya on Monday, the BOJ said, an event (which wasn’t previously scheduled) that will be closely watched by markets for hints on whether it might raise interest rates next month. The comments by Ueda could spark volatility in Yen pairs following a bout of weakness in recent weeks.

In China, data is thin next week. The loan prime rates will be announced on Wednesday, where no change is expected after the People’s Bank of China has so far held rates unchanged this month.

In Australia the highlight of the week will be the RBA minutes scheduled to be released Tuesday. The report could shed some light on the recent RBA meeting and provide insight into rate policy moving forward.

Europe + UK + US

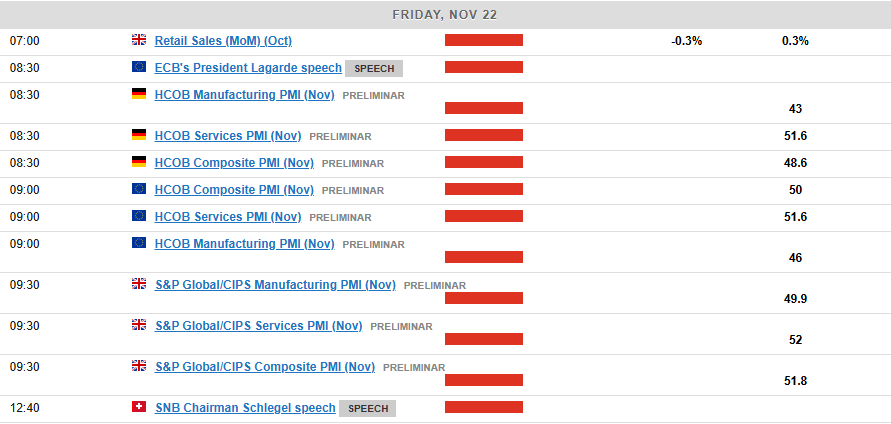

In developed markets, the Euro Area returns with high impact data and more specifically PMI numbers. This is crucial for the Euro Area as growth is now the primary source of concern for the region given the struggle by its manufacturing powerhouse, Germany. The Euro having lost so much ground in recent weeks to the greenback in particular could face renewed selling pressure if a lackluster PMI print is revealed.

In the UK, Q3 GDP showed the UK economy slowed to 0.1% with the economy in September shrinking by -0.1%. This makes the upcoming CPI data even more important and intriguing with the services inflation print in focus once more.

At the start of October, household energy bills went up by about 10%, which means overall inflation might go above 2% again. However, the Bank of England is more concerned with inflation in services which could rise toward 5% once more. ‘Core Services’ inflation is expected to drop significantly from 4.8% to 4.3%. This small detail probably won’t lead to a rate cut in December, but it suggests that the BoE might cut rates more sharply than the 2-3 cuts currently expected over the next few years.

In the US next week markets enjoy a pause on the data front with one high impact release on the agenda. The S&P PMI report will be released on Thursday which should not have a huge impact.

The next important updates will be the core personal consumer spending figures and the crucial November jobs report, coming out in two and three weeks, respectively.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week

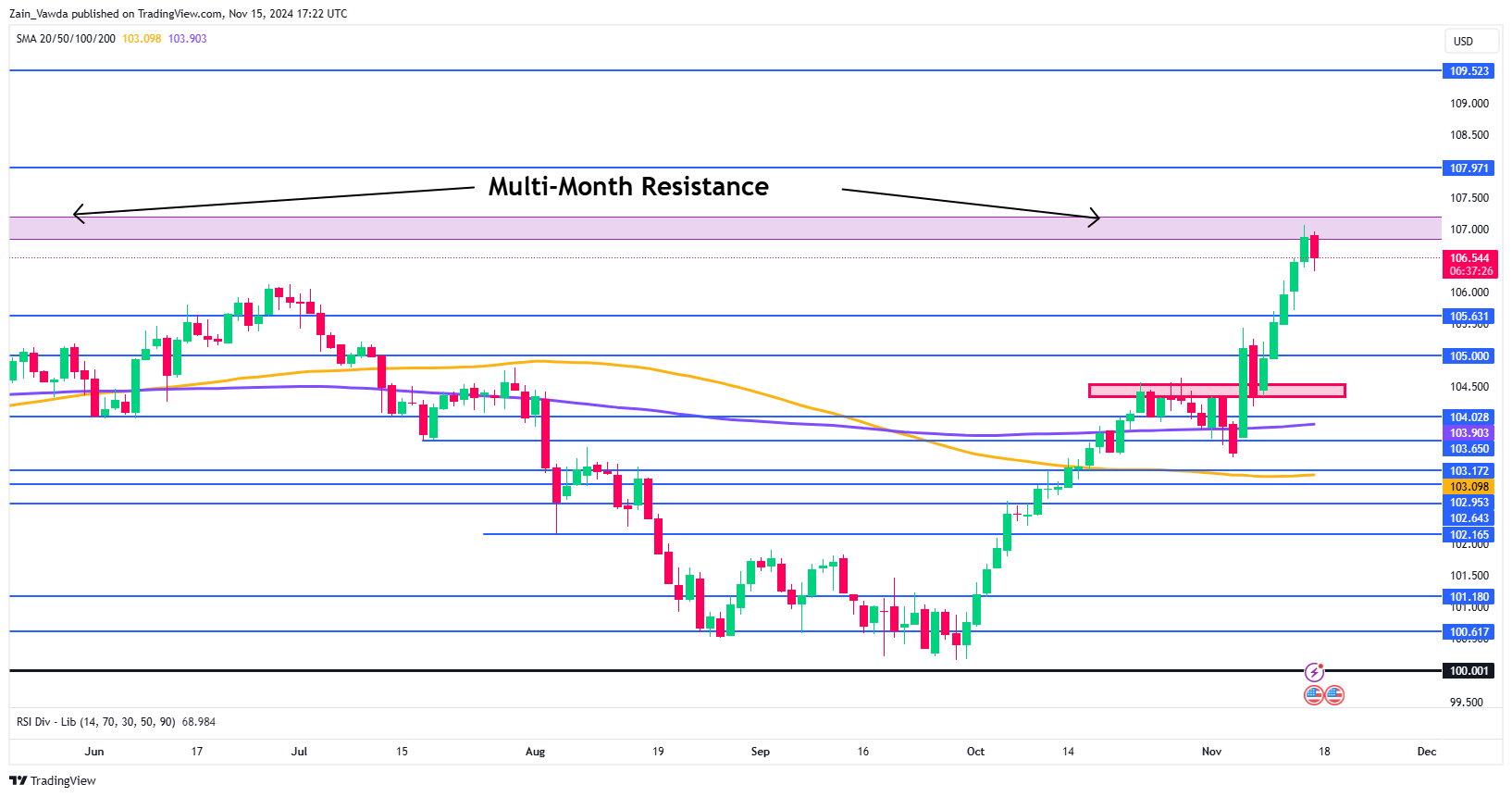

This week’s focus remains the US Dollar Index (DXY), which has run into multi-month resistance around 107.00 handle. The DXY has been having an effect across global markets together with US Yields and thus my intrigue into where we could head next.

The DXY chart below and you can see the pink box where price is currently hovering which is a key area of resistance that the index has to navigate. Friday saw a significant pullback in the European session, but US Data later in the day provided USD bulls with renewed impetus.

A break above the 107.00 handle may find resistance at 107.97 with a break above this level bringing 109.52 into focus.

Looking at the downside and immediate support rests around 105.63 before the 105.00 handle and the red box on the chart around 104.50 come into focus.

The DXY has been driving price action in all Dollar denominated instruments and this could continue in the week ahead.

US Dollar Index Daily Chart – November 15, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 105.63

- 105.00

- 104.50

Resistance

- 107.00

- 107.97

- 109.52

Follow Zain on Twitter/X for Additional Market News and Insights @zvawda

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Zain Vawda

He has spent the last 3 years in an analyst role honing his skills across various financial domains, including technical analysis, economic data interpretation, price action strategies, and analyzing the geopolitical impacts on global markets. Currently, Zain is advancing in obtaining his Capital Markets & Security Analyst (CMSA) designation through the Corporate Finance Institute (CFI), where he has completed modules in fixed income fundamentals, portfolio management fundamentals, equity market fundamentals, introduction to capital markets, and derivative fundamentals.

He is also a regular guest on radio and television programs in South Africa, providing insight into global markets and the economy. Additionally, he has contributed to the development of a financial markets course approved by BankSeta (Banking Sector Education and Training Authority) at NQF level 6 in South Africa.