Recent “risk on” pressure following Fed’s tapering has aided Crude oil prices greatly, pushing commodities higher. However, it should be noted that the largest bullish push in December wasn’t the post FOMC announcement, but due to the huge decline in Crude Oil Inventories (reported weekly by the DOE) released on 4th of December. Since then, DOE has been showing 3 more consecutive weeks of decline in inventories, with each week’s number beating the expected decline – showing a higher than expected implied demand and providing additional bullish driver on top of the improving risk appetite. Past 4 weeks data also suggest that the oversupply situation in US oil production which has depressed prices in September may be over, opening further bullish possibility and perhaps allow WTI to even catch up with Brent Crude.

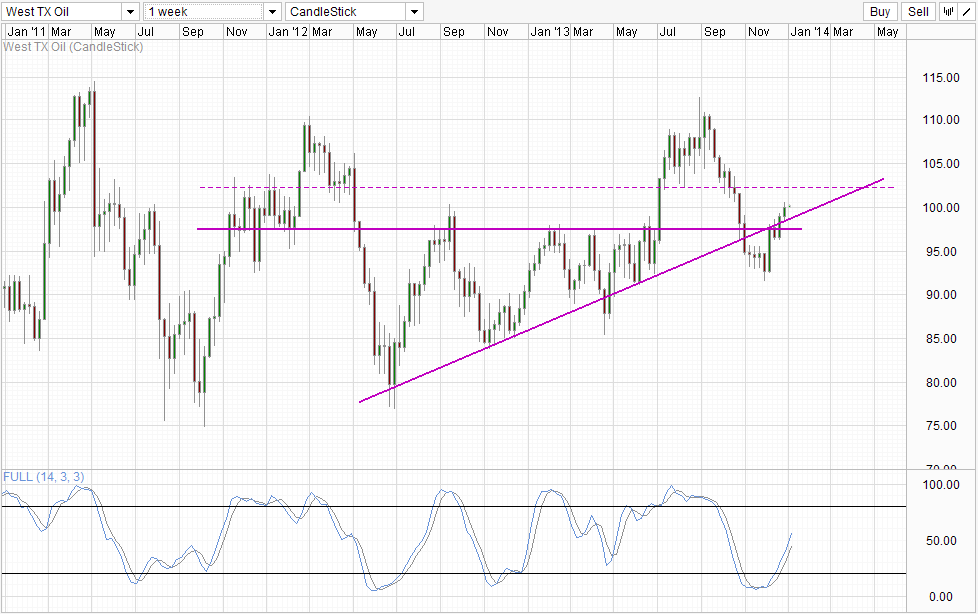

Weekly Chart

Price action agrees, as bulls have managed to break above the rising trendline and the 98.0 resistance, opening up a move towards the next level of resistance at 102.2. Stochastic readings agree as well with Stoch curve currently in the midst of a bullish cycle. Should bulls break above 102.2, 110.0 will open up as a viable bullish target.

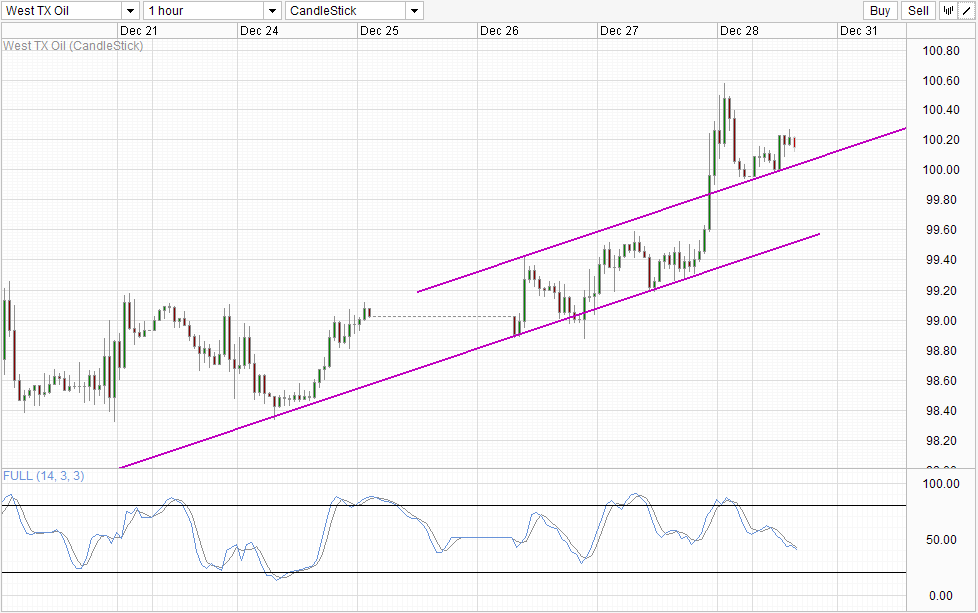

Hourly Chart

However, there are signs that bullish momentum may be fading. Bulls were not able to hold onto last Friday’s rally which was sparked by the latest bullish DOE numbers. We’ve seen some bullish action today, but we are far from recapturing last Friday’s high, with prices supported by the rising Channel Top. With Stochastic readings showing that bearish momentum is still in play, the possibility of Channel Top being broken remains which would open up the possibility of a larger correction towards Channel Bottom.

Fundamentally, the case for continued bullish push for WTI Crude remains weak. Global economic recovery may have improved, but production levels are far from pre financial crisis levels. Even after taking inflation into account, price should not be anywhere near the 100 USD per barrel level – where Oil was at before the crisis. Furthermore, oil production levels in US are hitting record highs after record highs, and current bout of decreasing inventory may simply be a short-term reprieve, with inventory expecting to build up strongly once again in 2014.

More Links:

AUD/USD Technicals – Strong Bearishness Seen In Thin Trade

EUR/USD – Hint Of Bearish Bias But Don’t Bet On It

Gold Technicals – Bullish Momentum Fading As Bears Enter

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

centers on forex and macro-economic trends impacting the Asia Pacific region.

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014