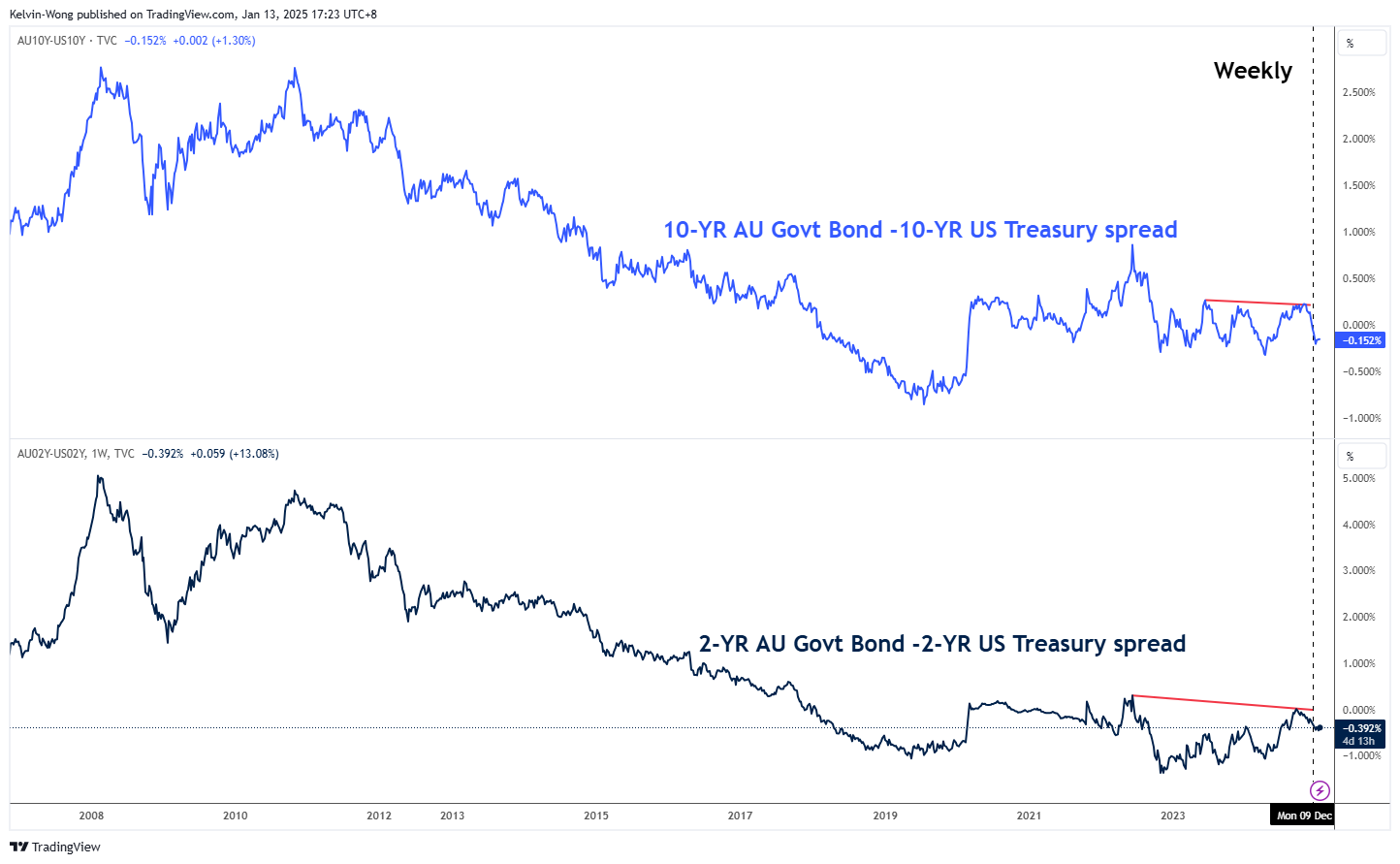

- A higher 10-year yield premium of the US Treasuries over Australian sovereign bonds has reduced the attractiveness of the Aussie dollar as a “high-yielding” currency.

- Deflationary risk in China coupled with potential higher trade tariffs policy from the US has reinforced recent languish movements in the Iron Ore CFR China futures.

- Major bearish breakdown in AUD/USD with next medium-term support at 0.6030/5990.

This is a follow-up analysis of our prior report “AUD/USD: Surviving at the 0.6360 key support (for now) but the long-term trend remains bearish” published on 13 December 2024. Click here for a recap.

The price movements of the AUD/USD have continued their bearish momentum and staged a major breakdown below 0.6360. In the last four weeks, it has tumbled by 3.50%, and on Monday, 13 January, it had printed a fresh 52-week low of 0.6131 at the time of the writing.

Bond vigilantes are back with a vengeance in the US Treasury market

Fig 1: Major trends of 2-year & 10-year yield spreads of AU sovereign bonds/US Treasuries as of 13 Jan 2025 (Source: TradingView, click to enlarge chart)

The incoming Trump administration’s proposed policies with steep corporate tax cuts and higher trade tariffs targeted toward US key trading partners stoked fears of further widening the US budget deficit and resurgence of inflationary pressures.

The US Treasury market in the long end has responded and reacted to such fears. The US 10-year Treasury yield has continued its relentless climb northwards after a bullish breakout on 18 December last year from almost a year of consolidation from its October 2023 swing high area of 5%.

Also, since the start of the new year in 2025, the rise in the 10-year US Treasury yield has increased at a faster pace than its lower-end two-year Treasury yield; an increase of 22 basis points (bps) over 15 bps respectively.

Hence, the 10-year yield spread between the Australian government sovereign bond and the US Treasury note has continued to narrow since 13 December from -0.05% to -0.15% at this time of the writing, potentially triggering further downside pressure on the AUD/USD currency rate (see Fig 1).

Lacklustre iron ore prices have exerted downside pressure on AUD/USD

Fig 2: AUD/USD & Iron Ore futures correlation movement as of 13 Jan 2025 (Source: TradingView, click to enlarge chart)

Given that iron ore is one of Australia’s key resource exports and a significant portion of it goes to China; if China’s economic growth remains feeble, there will be likely less demand for iron ore, in turn, put downside pressure on Australia’s trade balance that may trigger a negative feedback loop into the AUD/USD.

Since late September 2024, the movement of the Iron Ore CFR China futures contract listed on the Singapore Exchange has resumed its positive correlation with the AUD/USD.

Given that China’s deflationary risk spiral narrative is back on the radar screen again coupled with potential higher trade tariffs from the US that may put a drag on the export growth prospects of China, these double whammy factors have caused the Iron Ore CFR China futures contract (SGX) to languish below its 200-day moving average (see Fig 2).

These negative price action observations on the Iron Ore CFR China futures contract may have negative knock-on effects on the AUD/USD.

Major bearish breakdown in AUD/USD below 0.6360

Fig 3: AUD/USD medium-term trend as of 13 Jan 2025 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the bearish breakdown of their former 0.6360 support (also the former ascending trendline from 13 October 2023) on 17 December 2024 is considered a major price movement development where the AUD/USD has consolidated for almost a year before 17 December which suggests the start of a potential medium-term (multi-week) to major (multi-month) downtrend phases.

These bearish downtrend phases are also supported by the current negative reading seen in the daily MACD trend indicator that has steadily inched downwards below its centreline since 15 October 2024.

0.6360 key medium-term pivotal support and a break below 0.6120 exposes the next medium-term support at 0.6030/0.5990 on the AUD/USD (see Fig 3).

On the flip side, a clearance above 0.6360 Invalidates the bearish scenario for a potential mean reversion rebound scenario to unfold for the next medium-term resistances to come in at 0.6470 and 0.6560.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Kelvin Wong

Passionate about connecting the dots in the financial markets and sharing perspectives around trading and investment, Kelvin Wong is an expert in using a unique combination of fundamental and technical analyses, specializing in Elliott Wave and fund flow positioning, to pinpoint key reversal levels in the financial markets.

In addition, over the last ten years, Kelvin has conducted numerous market outlook and trading-related seminars, as well as technical analysis training courses, for thousands of retail traders.

Latest posts by Kelvin Wong (see all)

- AUD/USD: Aussie bears have taken a foothold reinforced by longer-term US Treasury yield premiums - 13 January 2025

- Hang Seng Index: Transforming into a medium-term bearish trend despite improving Services PMI from China - 8 January 2025

- Nasdaq 100 Technical: At risk of staging a multi-week corrective decline - 20 December 2024