- AUD/USD has been the worst performer among the major currencies in the past 4 weeks due to a double whammy slow-down growth effect from the US and China.

- RBA’s “hawkish hold” monetary policy stance on Tuesday may offer a relief for the AUD/USD.

- The recent 6.6% decline in the AUD/USD has almost reached an extreme oversold condition since December 2021.

In the past four weeks, the Aussie dollar has faced similar bloodshed with the major benchmark stock indices ranging from the US, and Europe to Asia on a synchronized global risk-off episode that intensified last week after the odds of a hard-landing recessionary environment in the US have increased.

Global markets witnessed a flight to safety to longer tenure US Treasury bonds and gold (XAU/USD) that outperformed in a mixed-bag US dollar environment.

The Aussie dollar is considered a higher-beta currency as it tends to be referenced as a proxy for growth, in turn also commodities-related due to Australia being the world’s largest iron ore producer that supplied most of its iron ore to China, its biggest export market.

Hence, the Aussie dollar is being hampered by a double whammy economic growth slow-down effect from two of the world’s largest economies, the US and China. In addition, China after the recent conclusion of its Third Plenum, top China policymakers emphasized the continuation of piecemeal stimulus policies rather than massive accommodative policies via heavy infrastructure spending to jumpstart the current lackluster internal demand environment.

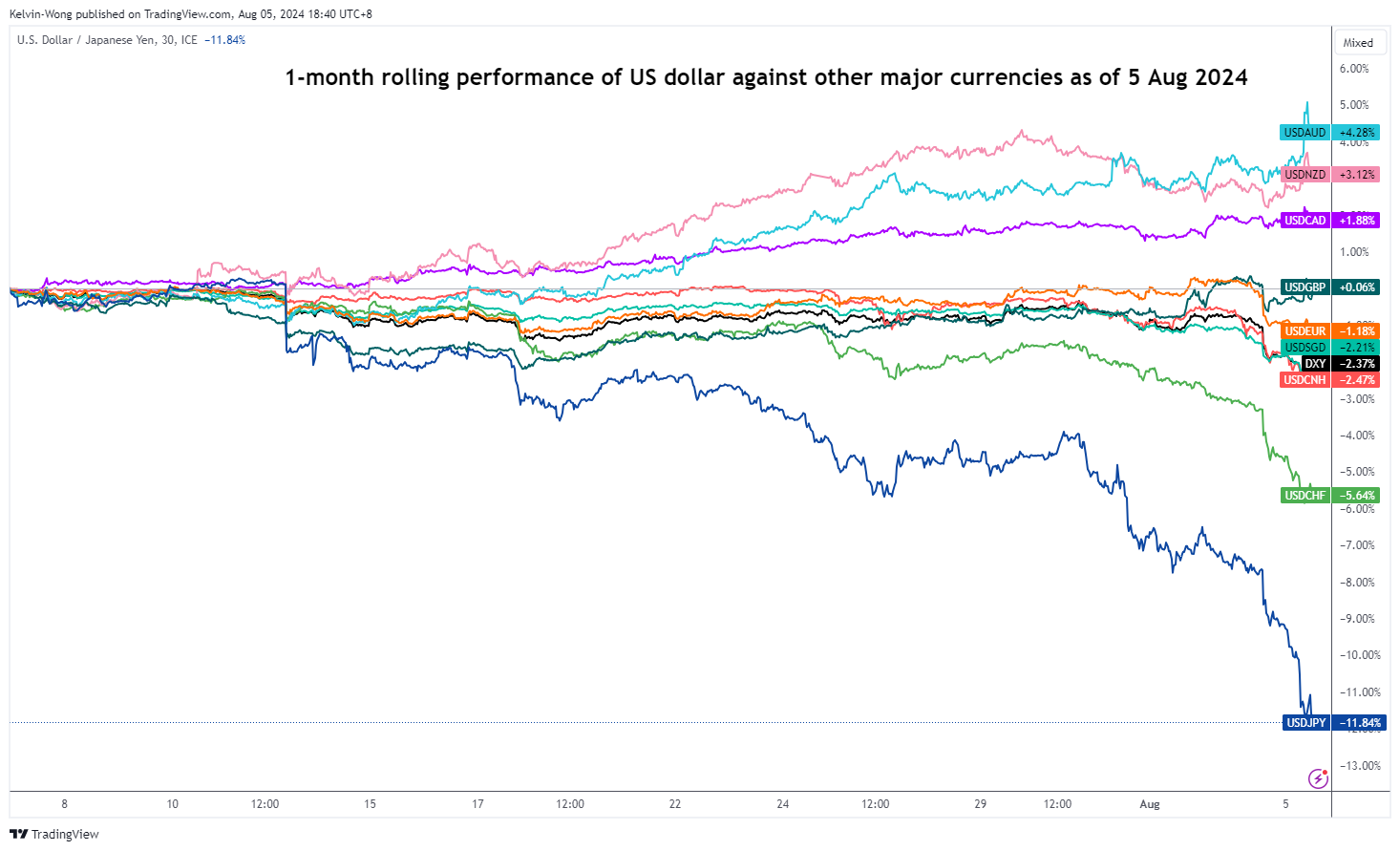

The Aussie dollar is the worst-performing major currency against the US dollar

Fig 1: 1-month rolling performance of the US dollar against major currencies as of 5 Aug 2024 (Source: TradingView, click to enlarge chart)

Thus, the Aussie dollar has been the weakest currency among the majors. Based on a one-month rolling performance basis, the US dollar has gained by 4.20% against the Aussie dollar and in contrast weakened against the safe haven proxies; the US dollar underperformed against the Swiss franc and Japanese yen by 5.60% and 11.85% respectively at this time of the writing.

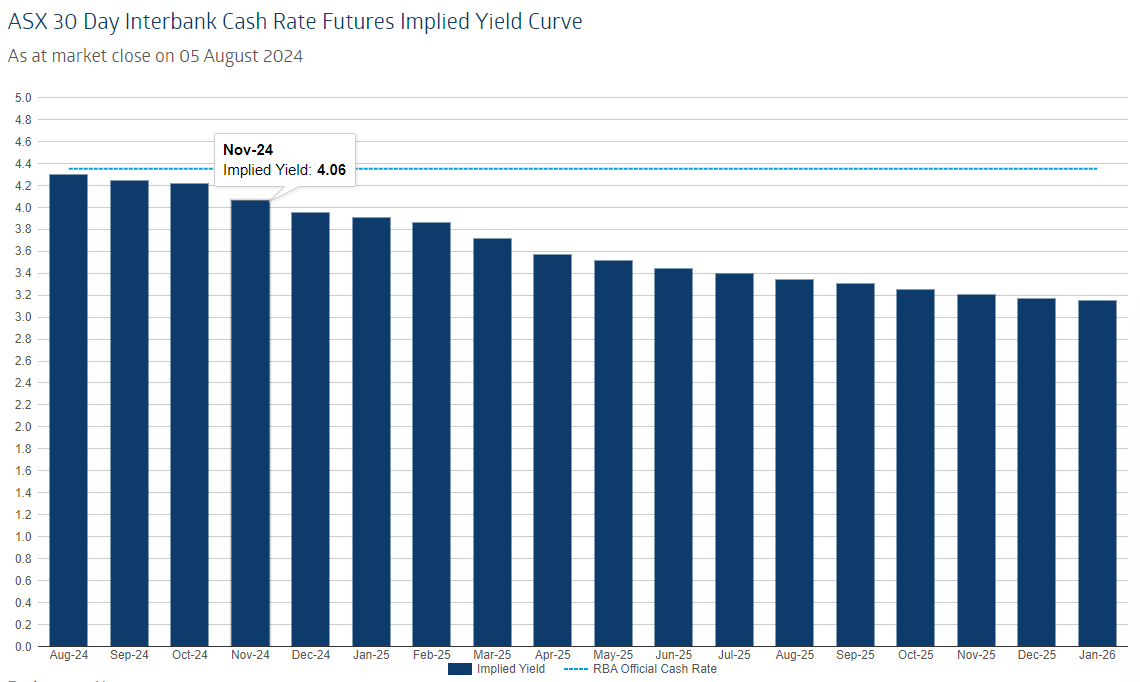

RBA may offer a relief to the battered down AUD/USD

Fig 2: ASX 30-day interbank cash rate futures implied yield curve as of 5 Aug 2024 (Source: RBA Rate Tracker from ASX, click to enlarge chart)

Despite Australia’s core inflation decelerated unexpectedly to 3.9% y/y for the second quarter from 4% in the first quarter, most economists expect RBA to hold its policy cash rate at 4.35% for a sixth consecutive meeting on Tuesday, 6 August, and leave the options open for its remaining monetary policy meetings in 2024.

Another potential impact on the AUD/USD is likely to come from its latest quarterly update of economic forecasts that will be released on Tuesday as well; so far past remarks from RBA Governor Bullock implied that RBA is not in a hurry to cut interest rates as current inflationary trend in Australia is still well above of its 3% to 2% target.

At this juncture, as of Monday, 5 August, the ASX 30-day interbank cash rate futures implied yield curve indicated an implied yield of 4.06% for the November 2024 contract which suggests a potential first RBA rate cut to occur towards the end of the year, in the November meeting versus a much more dovish US Federal Reserve (see Fig 2).

Latest data from the CME FedWatch tool has priced in with almost certainty that a 50 basis points cut in the Fed funds rate is to be enacted in the September FOMC meeting followed by a high chance of 78% for another 50 bps cut to bring it down to 4.25%-4.50% in the November meeting.

AUD/USD has almost reached an extremely oversold condition

Fig 3: AUD/USD medium-term trend as of 5 Aug 2024 (Source: TradingView, click to enlarge chart)

The 6.6% decline seen in the AUD/USD from its 12 July high of 0.6798 in the past 4 weeks has caused the daily RSI momentum indicator to hit an oversold condition of 23.40 at this juncture, its most extreme oversold level reached since 3 December 2021 reading of 20.25.

If the 0.6360 key medium-term pivotal support holds, the AUD/USD may see a potential mean reversion rebound to retest the intermediate resistances of 0.6565 and 0.6630 (also the 20-day and 50-day moving averages).

However, failure to hold at 0.6360 may ignite a bearish “Symmetrical Triangle” range breakdown scenario to expose the first major support of 0.6200.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Kelvin Wong

Passionate about connecting the dots in the financial markets and sharing perspectives around trading and investment, Kelvin Wong is an expert in using a unique combination of fundamental and technical analyses, specializing in Elliott Wave and fund flow positioning, to pinpoint key reversal levels in the financial markets.

In addition, over the last ten years, Kelvin has conducted numerous market outlook and trading-related seminars, as well as technical analysis training courses, for thousands of retail traders.

Latest posts by Kelvin Wong (see all)

- Gold Technical: Medium-term uptrend damaged, spooked by rapid rise in 10-year US Treasury yield - 14 November 2024

- Hang Seng Index: Medium-term bullish trend in jeopardy after China stimulus disappoints - 12 November 2024

- AUD/USD: “Trump Trade” overshadowed a cautiously hawkish RBA, at risk of further downside - 8 November 2024