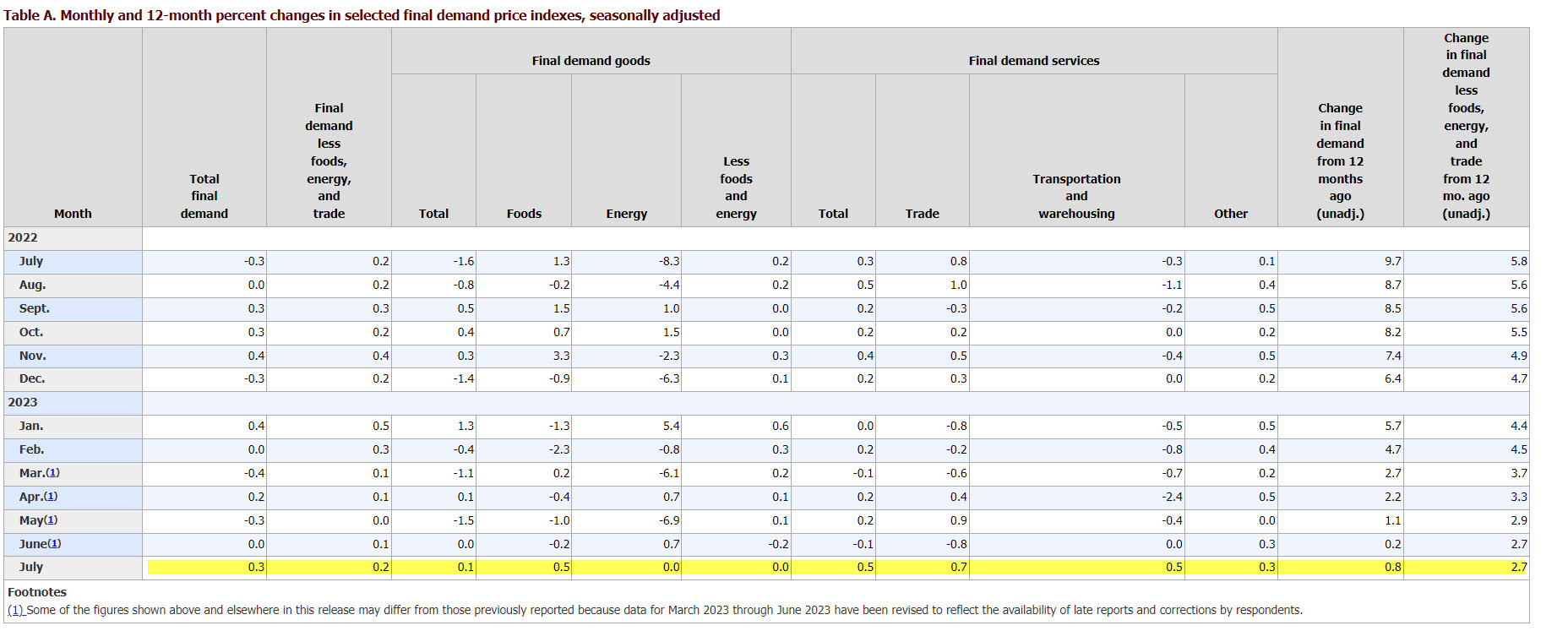

- US PPI posts first gain in three months (last month revised to a flat reading)

- Dollar eyes a fourth week of strength

- 10-year Treasury rises 2.9bps to 4.135%; November rate hike odds rise to 26.3%

The dollar pared losses after supplier inflation in July came in mostly hotter-than-expected. Hold your horses on calls that the Fed is done raising rates. This was a notable increase for producer prices and that could very well keep the risk of a November Fed rate hike on the table.

The producer-price index (PPI) for final demand rose 0.3% in July from the prior month. This PPI report suggests stubborn inflation pressures remain in the economy. Given the recent trends with the economy, expectations for the August readings could rise even further. The Fed is likely done raising rates, but the data might not support that call over the next month or two.

Following the hot PPI report, the dollar rebounded against the euro and yen. The British pound remained mostly firmer, still riding momentum from a GDP beat that confirmed the BOE has a lot more rate hiking to do.

This PPI report also showed some downward revisions with the monthly final demand figures. Overall, the strength in July pricing pressures came from the service sector. Service costs posted the biggest gain in almost a year. The August report will probably won’t be cool, so we might see markets fret over back-to-back monthly increases. Producers will pass these costs onto the consumer, so we might here a lot about inflation being sticky as we close out the summer.

EUR/USD – lower lows eyed as dollar gains for a fourth week

EUR/USD earlier in the week was making a strong move higher, but that stalled at the 1.1060 level, following knee-jerk reaction to the soft US inflation report. Much of that rise triggered some technical buying that ultimately quickly evaporated. Given seasonality and the rising fear of a reacceleration with pricing pressures, the dollar might remain bid here.

From a technical perspective, EUR/USD downward momentum could target 1.0825 on a daily close of the 1.0912 August low. Given summer trading conditions, if the macro drivers don’t support a stronger dollar, price could continue to pivot around the 1.10 level.

If we see broader signs of economic moderation, the bullish case for the euro could be revived, but that will need a confluence of data points to confirm that the Fed is done.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Ed Moya

His particular expertise lies across a wide range of asset classes including FX, commodities, fixed income, stocks and cryptocurrencies.

Over the course of his career, Ed has worked with some of the leading forex brokerages, research teams and news departments on Wall Street including Global Forex Trading, FX Solutions and Trading Advantage. Prior to OANDA he worked with TradeTheNews.com, where he provided market analysis on economic data and corporate news.

Based in New York, Ed is a regular guest on several major financial television networks including CNBC, Bloomberg TV, Yahoo! Finance Live, Fox Business, cheddar news, and CoinDesk TV. His views are trusted by the world’s most respected global newswires including Reuters, Bloomberg and the Associated Press, and he is regularly quoted in leading publications such as MSN, MarketWatch, Forbes, Seeking Alpha, The New York Times and The Wall Street Journal.

Ed holds a BA in Economics from Rutgers University.

Latest posts by Ed Moya (see all)

- Market Insights Podcast – Powell struggles to deliver a hawkish hold - 1 November 2023

- Fed React: USD/JPY softer after Fed fails to deliver hawkish hold - 1 November 2023

- EUR/USD: Dollar wavers on slower pace of Treasury Refunding Sales and mixed labor data - 1 November 2023