- Sovereign credit risk remains elevated in France despite yesterday’s rallies seen in the EUR/USD, CAC 40 & DAX ex-post first round of the French legislative election.

- Speculative net capital outflows & bearish sentiment in CAC 40 & DAX may trigger a negative feedback loop into the EUR/USD.

- EUR/USD at risk of breaking down below 1.0656

The EUR/USD gapped up by 26 pips at the start of yesterday, 1 July Asian session from last Friday, 28 June US session close of 1.0713 on a positive backdrop that preliminary results of the first round of the French legislation election that saw Le Pen’s far-right National Rally party took the lead but without a majority foothold ahead of the far-left coalition party, New Popular Front while French President Macron’s centrist alliance dwindled to third place. The National Rally party fell short of obtaining the absolute majority of 289 seats to control the French Parliament.

Together with news flow that reported horse-trading activities have taken place between the far-left and Macron’s centrist party to prevent Le Pen’s National Rally from securing a majority foothold in the upcoming second round of voting that occurs this Sunday, 7 July, the EUR/USD rallied further during the start of yesterday’s European session to print an intraday high of 1.0777, that’s summed up to an intraday gain high watermark of +64 pips/+0.60% from last Friday, US session close.

Similar intraday positive performances can also be observed on the benchmark stock indices for France and Germany where the CAC 40 and DAX recorded an intraday gain high watermark of +1.91% and +1.24% from their respective closing levels of last Friday.

Reversal of yesterday’s intraday gains in the EUR/USD, CAC 40 & DAX

However, these intraday rallies cannot be maintained, and the EUR/USD ended yesterday’s session,1 July with a meagre daily gain of just +0.25%, and a similar reversal can also be seen on the French and German stock markets where the CAC 40 and DAX pared back almost 50 percent or more of their early intraday gains yesterday to record closing daily gains of +1.09% and +0.30% respectively.

Sovereign credit risk remains elevated in France

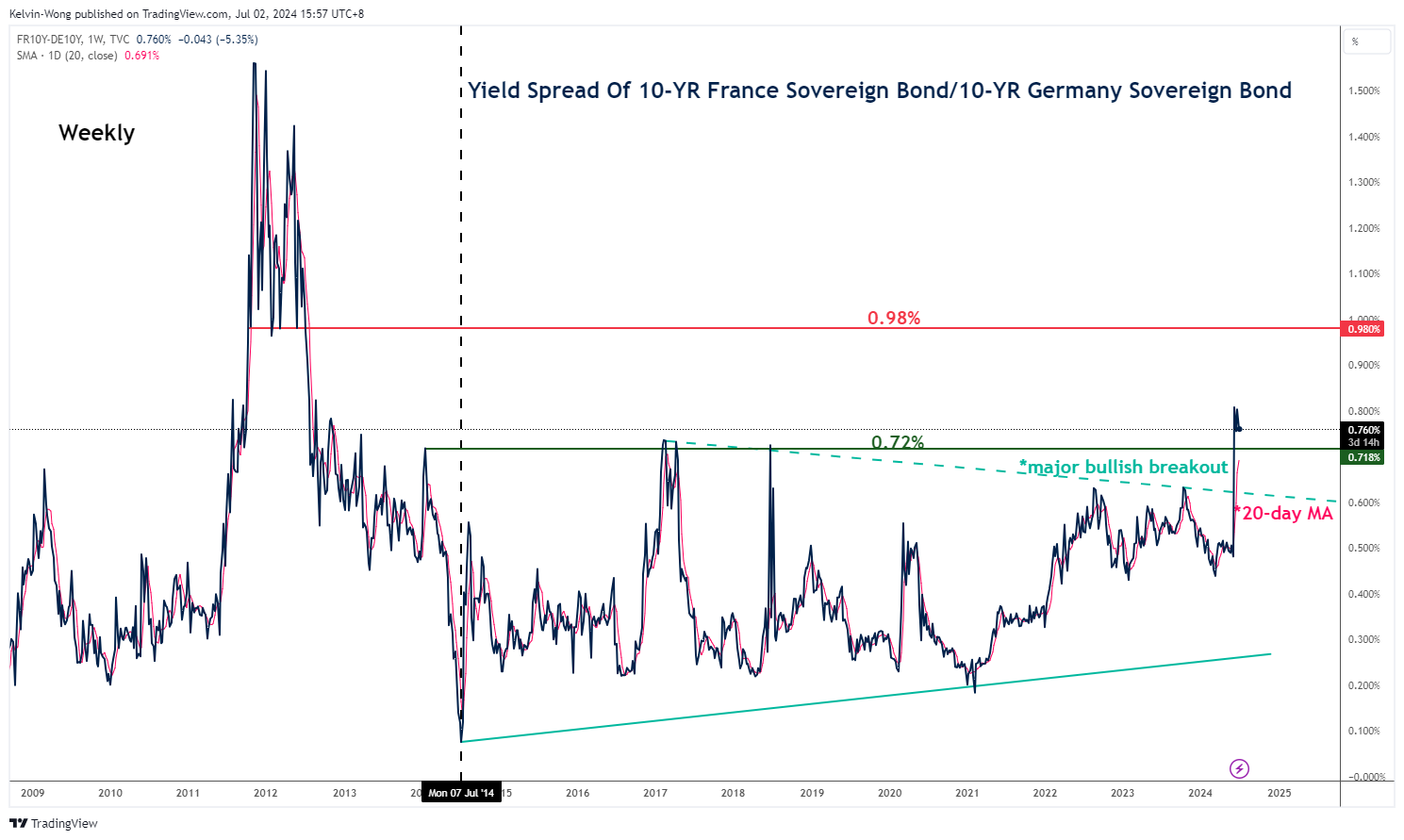

Fig 1: Yield spread of 10-year French & German government bonds as of 2 Jul 2024 (Source: TradingView, click to enlarge chart)

Even though, the yield spread between the 10-year France and German sovereign bond has inched lower slightly to 0.765% at this time of the writing from a 12-year high of 0.82% printed last Thursday, 27 June; it remains at an elevated level according to its trend analysis.

The yield spread is still evolving within a short-term uptrend phase after a major bullish breakout that occurred on the week of 10 June 2024 as it remains supported at 0.72% which corresponds to a rising 20-day moving average with the next medium-term resistance coming in at 0.98% (see Fig 1).

Also, if Macron’s centrist alliance decides to support the far-left coalition, the New Popular Front party now in second place after the first round of voting with a projected vote share of 28% to 29%, it may allow the far-left party an easier maneuver ticket in the France parliament to advocate their more aggressive fiscal spending policies and tax cuts as compared to the far-right which in turn is likely to widen France’s last year excessive budget deficit of 5.5% that breached EU’s benchmark budget deficit ceiling of 3%.

Therefore, the bond vigilantes are still on the lookout for a possible uptick in credit risk in France which in turn may spread to the wider Eurozone due to the contagion effect as European banks do have significant holdings of French sovereign bonds since France is one of the economic anchors in the EU other than Germany.

Current short-term bearish trends in CAC 40 & DAX trend may trigger negative sentiment towards the Euro

Fig 2: France CAC 40 medium-term trend as of 2 Jul 2024 (Source: TradingView, click to enlarge chart)

Fig 3: Germany DAX medium-term trend as of 2 Jul 2024 (Source: TradingView, click to enlarge chart)

As seen in the daily technical charts of the French CAC 40 and German DAX, both of them are still evolving in short-term bearish trends as their respective price actions remain below their respective downward-sloping 20-day moving averages with bearish momentum conditions seen in their daily RSI momentum indicators.

Interestingly, yesterday’s price actions of the CAC 40 and German DAX have shaped daily key bearish reversals right below their respective key short-term pivotal resistances of 7,725 and 18,465 respectively (see Fig 2 & 3).

The short-term movements in the FX market are also impacted by short-term speculative equities-related capital flows. Given the prevailing short-term bearish trends that are still intact on the CAC 40 and DAX, in turn, may see net short-term capital outflows that can likely trigger a double-whammy negative impact on the EUR/USD at least on a short-term horizon from both flows and sentiment perspectives.

Watch the 1.0770/0790 key short-term resistance on EUR/USD

Fig 4: EUR/USD short-term trend as of 2 Jul 2024 (Source: TradingView, click to enlarge chart)

Current price actions of the EUR/USD have wiped out yesterday’s post-French election results-induced rally after a bearish reversal right at the intersection of all three key moving averages (20-day, 50-day, and 200-day), and the 4-hour RSI momentum indicator has flashed out a bearish condition (see Fig 4).

These observations from a technical analysis perspective suggest low odds of a potential recovery or bottoming configuration at play for the EUR/USD.

If the 1.0770/0790 key short-term pivotal resistance holds, a break below 1.0656 support (lower limit of the “Symmetrical Triangle” range from 3 October 2023 low) may trigger further downside pressure to expose the next intermediate supports at 1.0620/0600 and 1.0530.

However, a clearance above 1.0770/0790 negates the bearish tone for a squeeze up towards the upper limit of the “Symmetrical Triangle “range to see the next intermediate resistances coming in at 1.0815, 1.0850, and 1.0925/0940.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Kelvin Wong

Passionate about connecting the dots in the financial markets and sharing perspectives around trading and investment, Kelvin Wong is an expert in using a unique combination of fundamental and technical analyses, specializing in Elliott Wave and fund flow positioning, to pinpoint key reversal levels in the financial markets.

In addition, over the last ten years, Kelvin has conducted numerous market outlook and trading-related seminars, as well as technical analysis training courses, for thousands of retail traders.

Latest posts by Kelvin Wong (see all)

- Nasdaq 100 Technical: At risk of staging a multi-week corrective decline - 20 December 2024

- Gold Technical: A less dovish Fed may reinforce a medium-term corrective decline - 16 December 2024

- AUD/USD: Surviving at the 0.6360 key support (for now) but the long-term trend remains bearish - 13 December 2024