- A potential uptick in Japan’s core-core CPI led by PPI may increase the odds of a BoJ’s interest rate hike in September.

- Republican presidential nominee Donald Trump’s betting odds have slipped after US President Biden decided to bow out of the US Presidential Election race.

- A resurgence of Trumponomics that may be challenged which in turn may lead to a US dollar mixed-bag to negative environment in the short term.

- Another daily close below 156.50 on the USD/JPY may trigger a multi-week corrective decline sequence.

This is a follow-up analysis of our prior report, “USD/JPY: Soft US data offers a potential relief rally for JPY” published on 8 July 2024. Click here for a recap.

Since the publication of our last analysis, the USD/JPY has indeed shaped the expected decline in the following two weeks; it declined by 538 pips/-3.35% to print an intraday low of 155.37 on Thursday, 18 July 2024 before it closed higher at 157.36 by the end of the US session that held above its key medium-term support at 156.50.

Two key catalysts for the recent weakness seen in the USD/JPY (Japanese yen strength revival); firstly, it has been the increased odds of a more dovish US Federal Reserve expectations to kickstart in the September FOMC meeting after a slew of soft key US economic data in terms of spending and inflationary trends.

Secondly, in an earlier Bloomberg interview with Republican US Presidential candidate Donald Trump published on Tuesday, 16 July, Trump implied that he favored a weaker US dollar against the Japanese yen and Chinese yuan (due to US exports losing competitiveness) despite the medium-term fundamental impact of the FX market is likely still a US dollar strength narrative as policies of Trumponomics of higher tax cuts yield a wider US budget deficit, in turn, drives up longer-term US Treasury yields which is US dollar positive.

Let’s now discuss the current factors (fundamentals, politics, and technical) that may support another leg of JPY strength at least in the short term.

Japan’s consumer inflation deceleration trend has started to stall

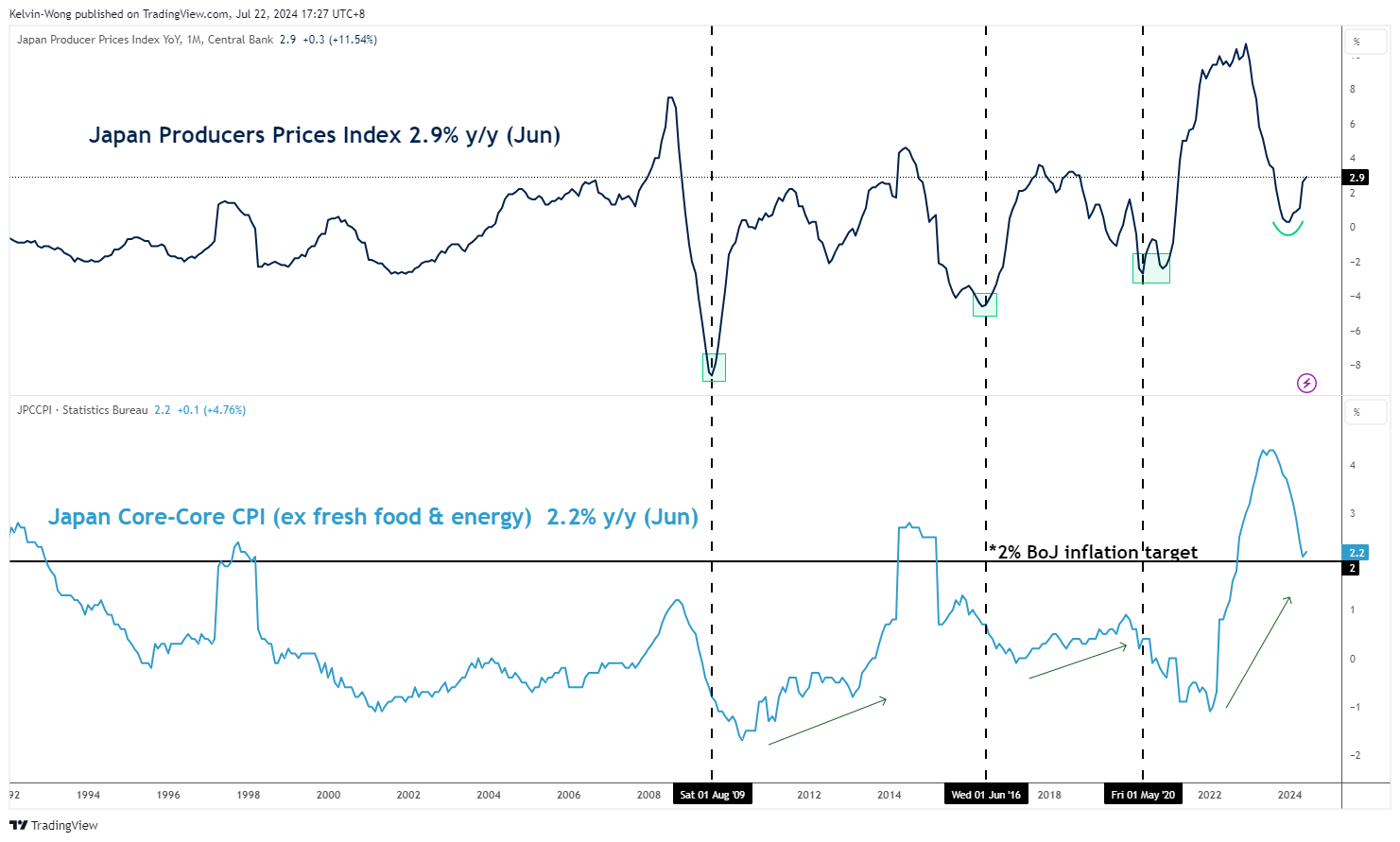

Fig 1: Monthly Japan’s PPI & CPI trends (y/y) as of Jun 2024 (Source: TradingView, click to enlarge chart)

Japan’s nationwide core-core CPI (excluding fresh food and energy) has inched slightly higher in June to 2.2% y/y from 2.1% y/y in May (see Fig 1).

An interesting observation to highlight in terms of Japan’s producer prices index (manufacturers input costs) leading correlation with Japan’s core-core inflationary trend.

Based on the past three periods in August 2009, June 2016, and May 2020, the producer prices index (PPI) bottomed out first before core-core CPI trended higher, and the recent PPI has started to inch higher for six consecutive months to hit 2.9% y/y in June which suggests that the deceleration trend of Japan’s core-core CPI from its August 2023 reading of 4.3% y/y may have hit an inflection level in June and could follow the current upward bias trend of PPI.

A further uptick in core-core CPI above Bank of Japan (BoJ) inflation target of 2% is likely to set the stage for another potential interest rate hike in September after it enacted the first rate hike in March after 17 years, and such a signal or guidance may come in the upcoming 31 July monetary policy decision via a potential announcement of a further reduction in the purchase of 10-year Japanese Government Bonds (JGB).

Overall, a further potential reduction in the yield premium gap between US Treasuries and JGBs may support a further strengthening of the JPY.

Trump’s chances of winning the US presidency have slipped

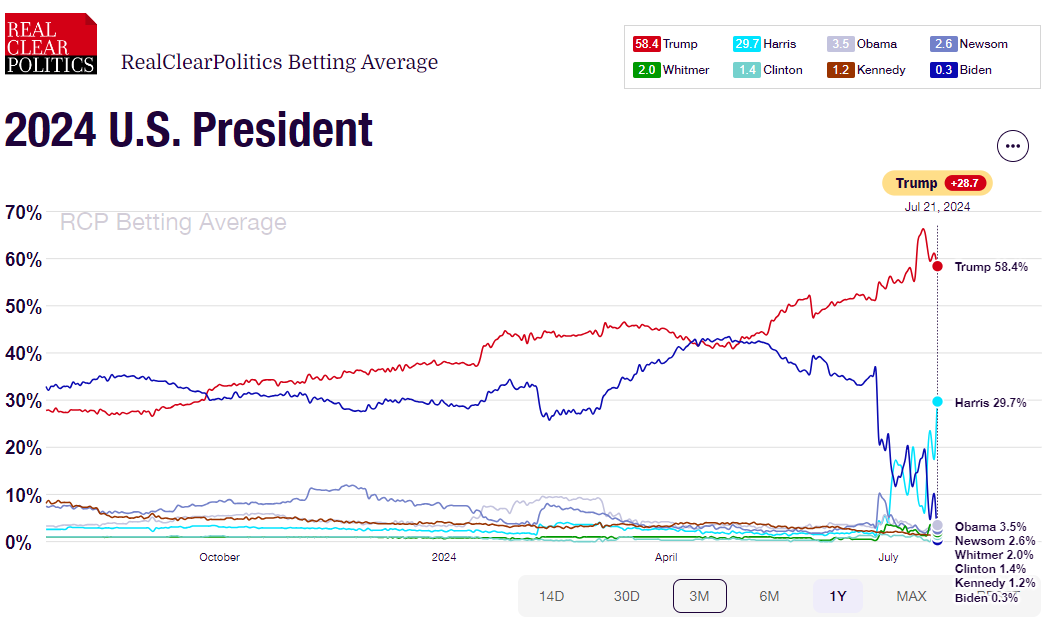

Fig 2: Average betting odds of 2024 US Presidential Election result of 21 Jul 2024 (Source: Real Clear Politics, click to enlarge chart)

After weeks of urging by senior leaders within the Democrat camp, US President Biden has decided to step down from the US Presidential Election race on Sunday, 21 July, and announced his endorsement for Vice President Kamala Harris to be the Democrat US presidential nominee

So far, several prominent Democrats and will-be presidential nominee contenders have thrown in their support to endorse Harris as their preferred choice to face off against Trump as reported by various media outlets, such as Bill and Hillary Clinton, California Governor Gavin Newsom, and all 50 Democrat party state chairs.

The latest average betting odds on the 2024 US Presidential Elections result compiled by Real Clear Politics as of 21 July has indicated Republican presidential nominee, Trump has slipped to 58% from a significantly high level of 66% on 15 July (after the failed assassination attempt). Meanwhile, the odds for Democrat Harris have increased to 30% significantly from 7% over the same period.

Hence, betting markets suggest Trump’s margin of winning has been reduced which may be US dollar negative as the odds of the passage of Trumponomics policies have inched down as well.

More bearish medium-term technical conditions sighted

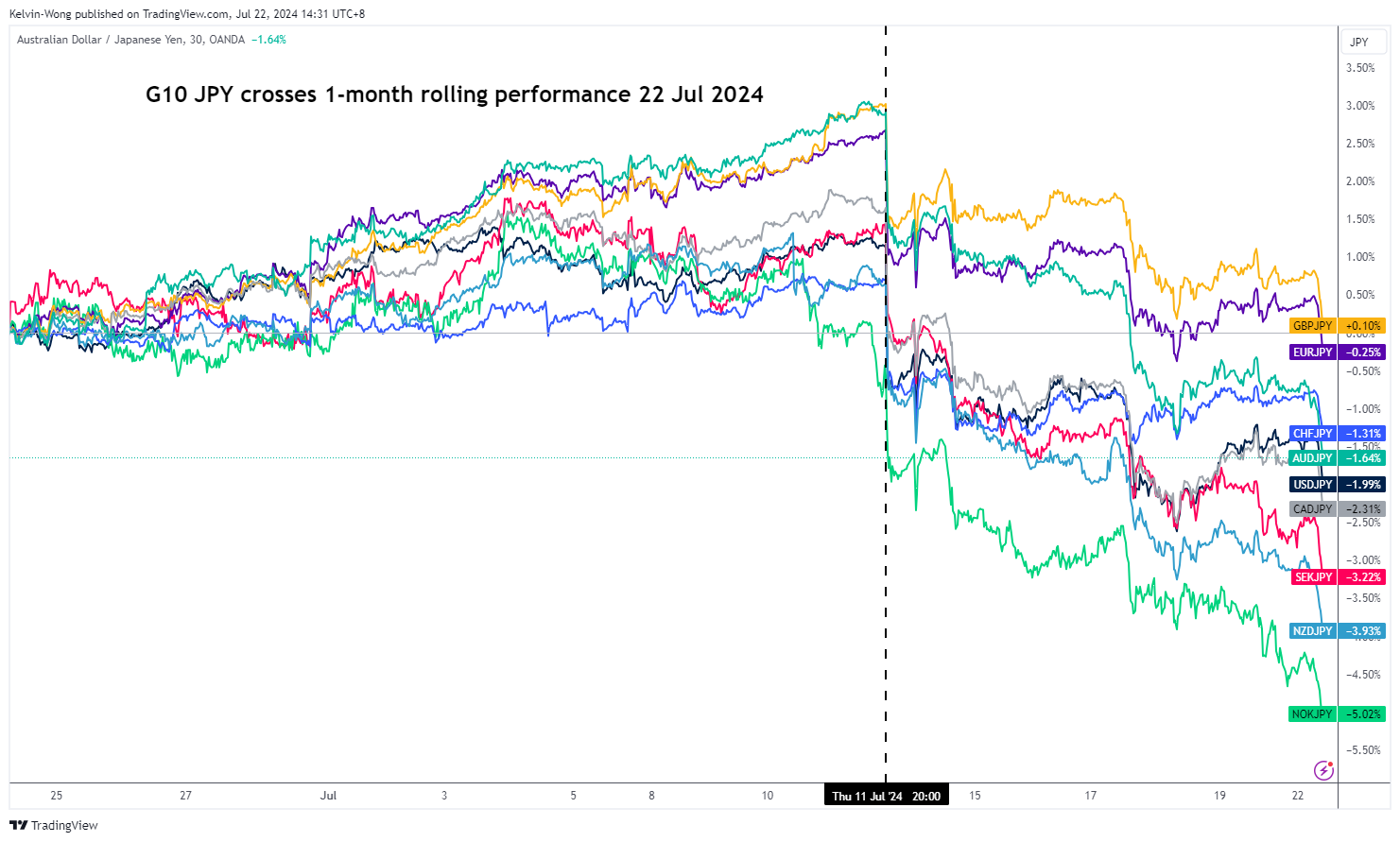

Fig 3: 1-month of rolling performances of G-10 JPY crosses as of 22 Jul 2024 (Source: TradingView, click to enlarge chart)

Fig 4: USD/JPY medium-term & major trend phases as of 22 Jul 2024 (Source: TradingView, click to enlarge chart)

After a bearish divergence condition sighted on the daily RSI momentum indicator on 3 July, there has been another negative price action following through on the USD/JPY.

It has staged a bearish breakdown below its 50-day moving average, the first time since 8 March 2024, and the lower boundary of the medium-term ascending channel in place since the 28 December 2023 swing low.

These negative observations suggest that USD/JPY may be on the brink of a potential multi-week corrective decline phase if its price action has another daily close below 156.50 that exposes the next medium-term pivotal support at 151.70 (also the 200-day moving average) (see Fig 4).

On the other hand, a clearance above 162.40 sees the continuation of the impulsive upmove sequence for the next medium-term resistances to come in at 164.20/164.90 and 167.10 next.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Kelvin Wong

Passionate about connecting the dots in the financial markets and sharing perspectives around trading and investment, Kelvin Wong is an expert in using a unique combination of fundamental and technical analyses, specializing in Elliott Wave and fund flow positioning, to pinpoint key reversal levels in the financial markets.

In addition, over the last ten years, Kelvin has conducted numerous market outlook and trading-related seminars, as well as technical analysis training courses, for thousands of retail traders.