Chinese Manufacturing sector is indeed slowing down, if recent PMIs have us believe. Official Manufacturing PMI for April released yesterday came in at 50.6 versus 50.7 expected, lower than previous month’s 50.9. Today’s HSBC numbers agree with the slowdown, coming in at 50.4 vs 50.6 estimated, suffering an even greater drop from previous month’s 51.6. According to RBA and also PBOC members, Chinese current growth is “sustainable”, but you would not believe the assertion if you look at the official PMI data which has now missed market expectations for 5 consecutive months.

Well, perhaps we have misinterpreted what RBA and PBOC has said. Sustainability in their terms does not refer to maintaining current pace of growth, but rather, as long as China is growing however slowly, it is considered “sustainable”. If we look at it this way, then certainly one must say that China is growing. PMI for Manufacturing sector has been consistently above 50.0 par level since Dec 2012.

Hourly Chart

However, most readers will not associate such tepid interpretation to the relative hawkish and upbeat RBA recent statements. And hence it is no surprise to see AUD/USD making a huge U-turn after the official PMI numbers yesterday. Prices took a huge hit yesterday due to more negative numbers coming out from the Atlantic shores – US ADP Employment came in 119K vs 150K expected, ISM manufacturing 50.7 vs 51.0 expected, dragging risk appetite down and risk correlated assets such as Aussie lower. FOMC statement that came in later in the afternoon was much more dovish than before – Fed saying that it will “increase or reduce the pace of its purchases”, the first time QE3 has been given an option to expand. This had zero impact on prices though, as stocks remain muted and stayed in the red. AUD/USD did rally slightly higher, but did not move more than 20 pips as price bounced from 1.028 to just under 1.03.

Bears quickly took initiative again but price found interim support around 1.027, which was also broken during early Asian hours due to a slew of red numbers coming out from Australia. Y/Y Building approvals fell to 3.9% vs 13.6% expected, while export price index grew at 2.8% Q/Q, a significant miss from the 4.5% forecast. The HSBC miss was simply the icing of the bearish cake that market has been eating since the decline yesterday, and looking at current momentum, there is no evidence that dessert is over.

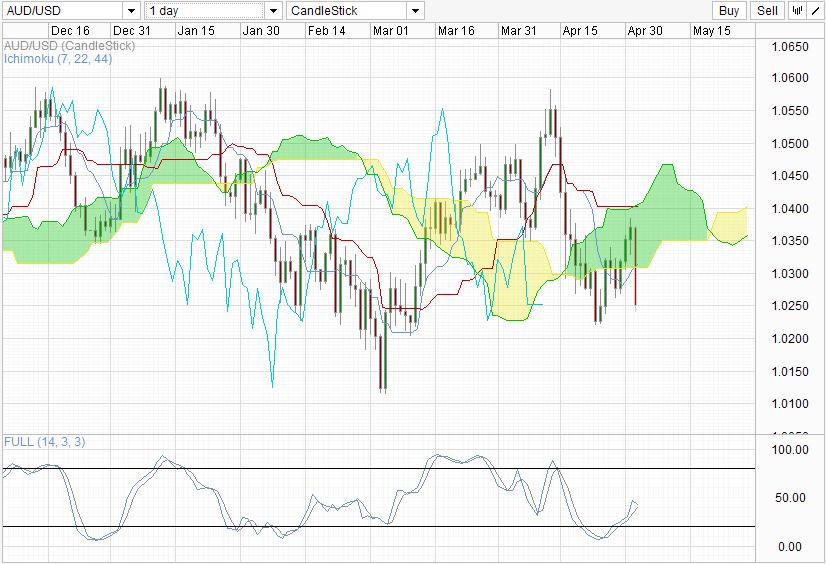

Daily Chart

From the Daily Chart, price is looking bearish due to the failure to reclaim 1.035 convincingly. Ichimoku forewarned us about the bearish possibility with a Kumo twist last week even as price traded into the Kumo. With a breakout of current Kumo, current price action is aligned with the bearish bias the forward kumo twist has given us, and we could see a retest of April lows, and potential bearish acceleration towards March low if the aforementioned level has been broken.

Fundamentally, inflation levels in Australia is still within RBA target range but it is clear that pace of inflation growth has come down significantly. With Building Approvals shrinking, and yesterday’s AIG Manufacturing Index coming in weaker than before, RBA may have more wiggle room to ease further if they wish. However, their intention has been leaning to the hawkish side for a few months, and has not shown any evidences that it may change. With that in mind, traders may wish to wait for the upcoming RBA rate decision to see if the new economic data has swayed any closet doves within RBA to come out stronger in 2013.

More Links:

AUD/USD – Falls Sharply Back Under 1.03

EUR/USD – Reaches Highest Level in Two Months Above 1.32

GBP/USD – Moves Higher Again to Above 1.56

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

centers on forex and macro-economic trends impacting the Asia Pacific region.

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014