US Futures Continue to Pare Last Week’s Gains

US equity markets are expected to open in the red again on Wednesday, tracking losses in Europe as stocks continue to pare last week’s strong rebound.

It’s been a relatively quiet start to the morning and the week, with the bank holiday in the US and Canada contributing to this. The European session has been dominated by economic data releases so far and that’s likely to continue, with flash manufacturing and services data due from the US shortly after the open. It’s the FOMC minutes that will be released later in the day though that will likely be the standout event from a US perspective, particularly as the statement caused quite a stir at the end of January.

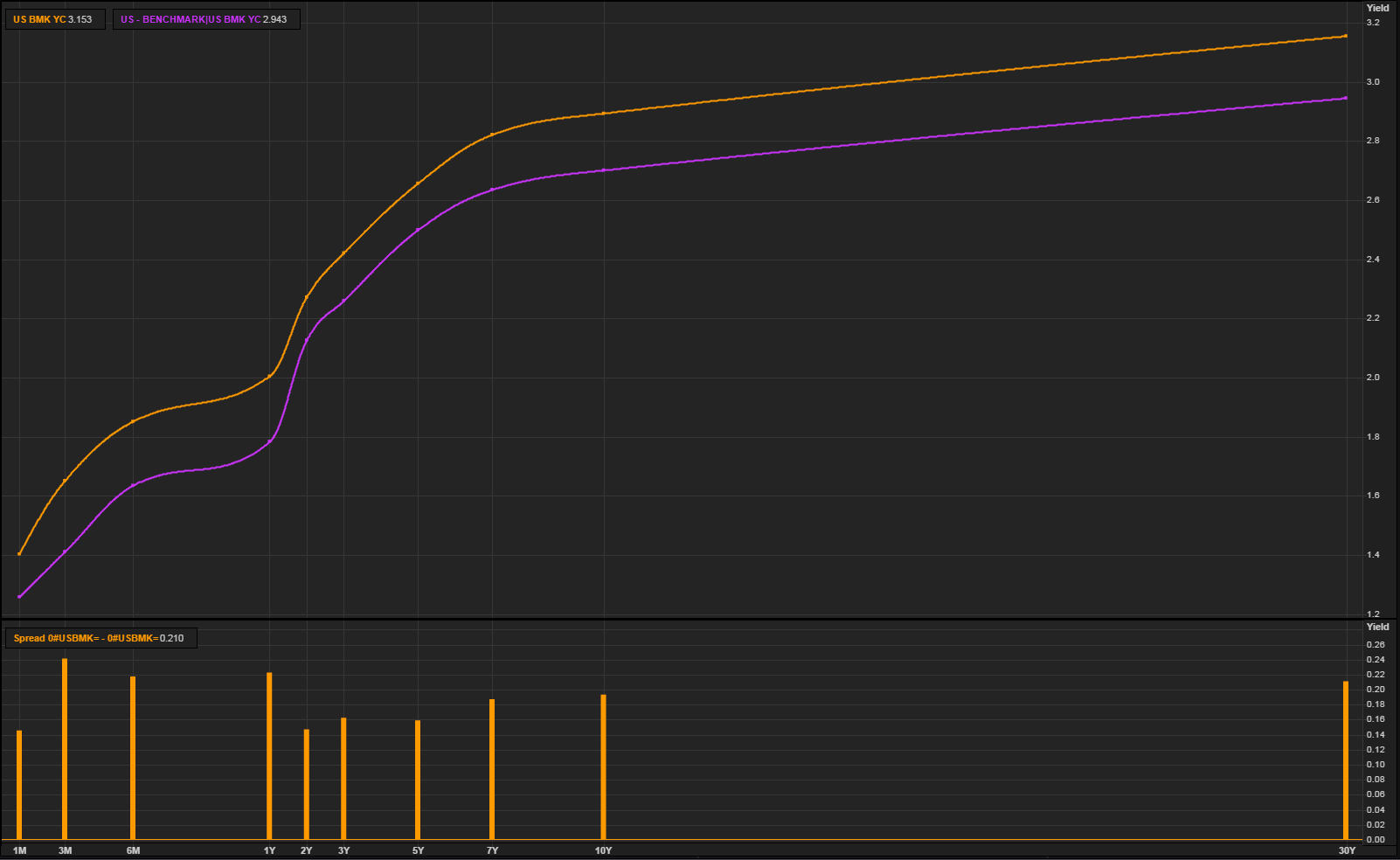

US Yield Curve Now (Orange) and on 29 January 2018 (Purple)

Source – Thomson Reuters Eikon

The sell-off in the markets may have come a couple of days later but part of the initial trigger was a more hawkish sounding Fed, with the jobs report then being the straw that broke the camel’s back two days later. While the minutes may not generate quite the same response, traders will likely monitor what they say very closely for signs that policy makers are now leaning more towards three to four rate hikes this year, rather than two or three.

EUR/USD – Euro Ticks Lower as German Manufacturing PMI Softens

GBP Slips as Unemployment Ticks Higher

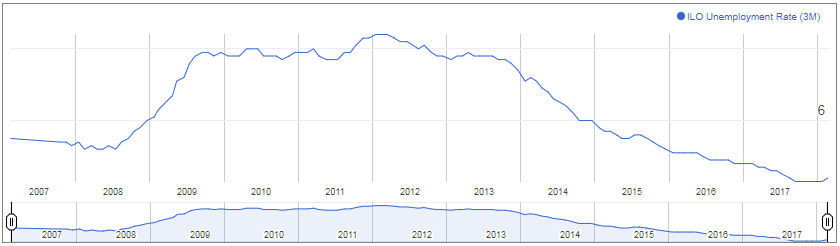

Sterling is coming under a bit of pressure this morning after UK jobs data for the three months to December showed wages still growing at a moderate pace and unemployment ticking up to 4.4%. While a higher reading on wage growth may have triggered a more bullish response from the pound, the data turned out to be quite insignificant as it’s unlikely to change the views at the Bank of England.

UK Unemployment Rate

Wages have been slowly ticking higher recently and they could continue to do so as workers demand more due to the higher cost of living and a tight labour market. The move higher in the unemployment rate won’t be a concern at this moment with it potentially being a one-off move and still very low. As long as inflation remains at upper range of what is deemed acceptable, the central bank seems intent on raising rates at least once more this year, despite the temporary factors driving it and economic uncertainty that lies ahead.

BoE Inflation Report Hearing Eyed as Markets Price in Rate Hikes

Members of the Monetary Policy Committee including Governor Mark Carney will appear before the Treasury Select Committee later on today, during which they will be questioned on their latest inflation report forecasts and expectations for interest rates going forward. While it’s always interesting to get the views of policy makers and the pound will likely be volatile throughout, I wonder how much of what they have to say will now already be priced in, with at least one rate hike now expected this year.

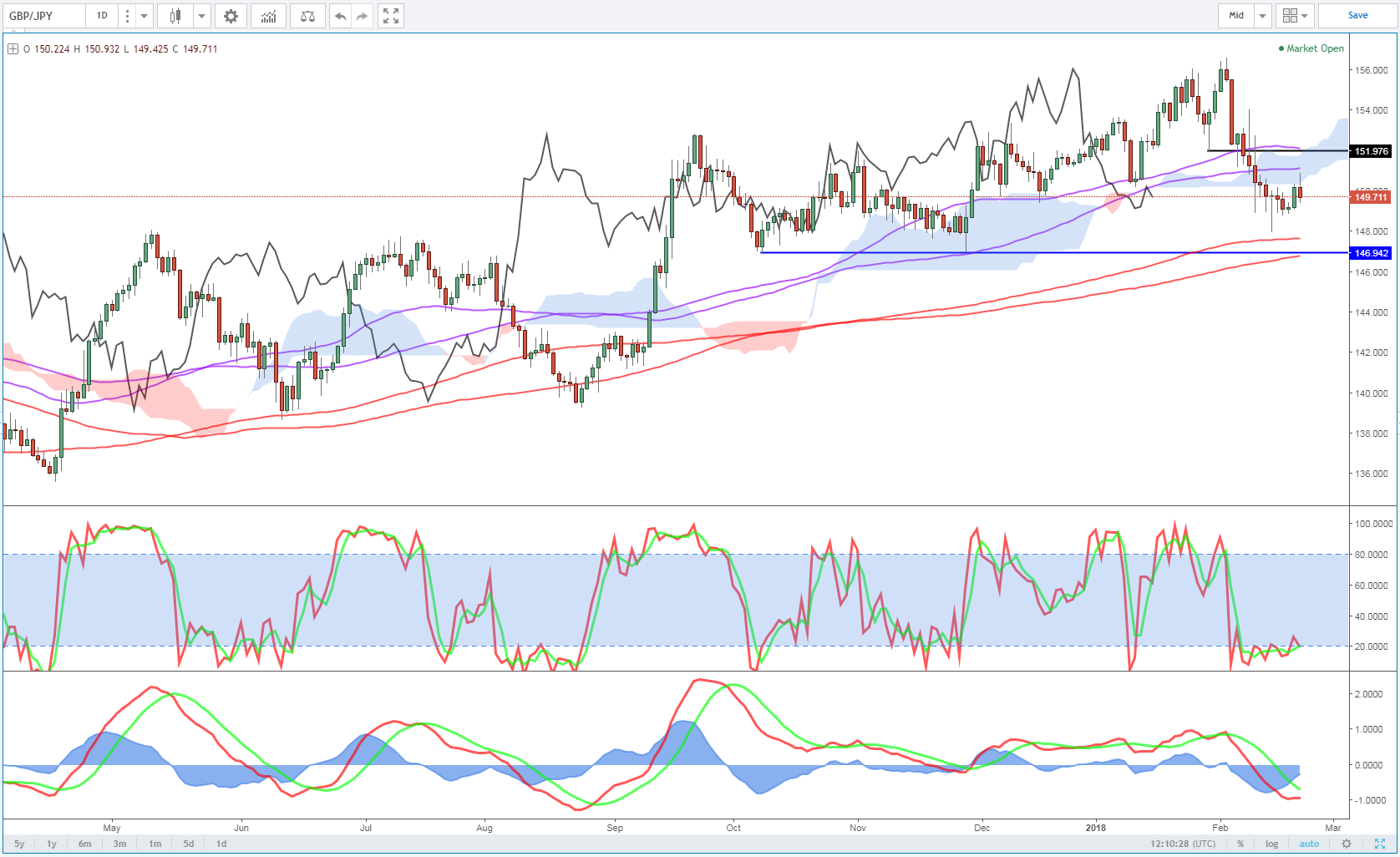

GBPUSD Daily Chart

OANDA fxTrade Advanced Charting Platform

With that in mind and with Brexit transition negotiations likely to dominate the next month, we could see the pound lose some of the momentum that’s been gathering over the last six months or so. It’s recent failed to make new highs on two occasions against the dollar and it’s also slipping against the yen in a possible sign that traders are beginning to lock in profits ahead of what could be a difficult month.

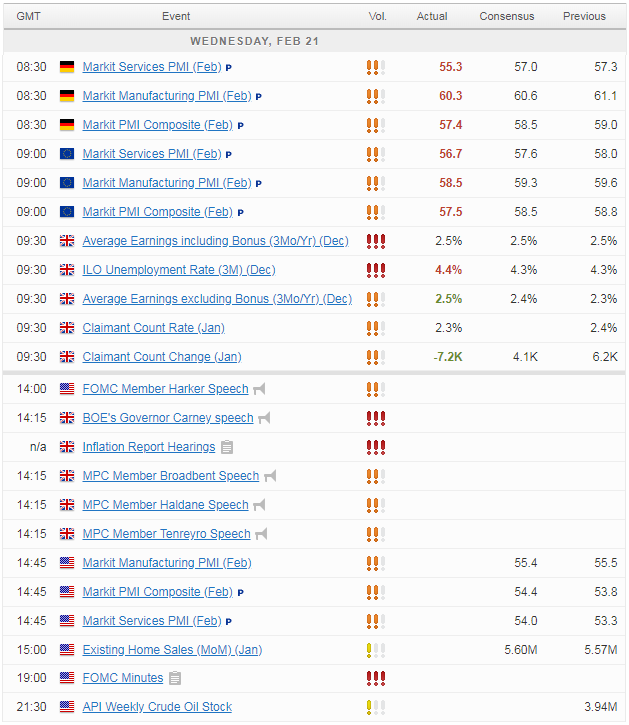

Economic Calendar

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Craig Erlam

His views have been published in the Financial Times, Reuters, The Telegraph and the International Business Times, and he also appears as a regular guest commentator on the BBC, Bloomberg TV, FOX Business and SKY News.

Craig holds a full membership to the Society of Technical Analysts and is recognised as a Certified Financial Technician by the International Federation of Technical Analysts.

Latest posts by Craig Erlam (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024