European equity markets are expected to start the week relatively unchanged, following a similar session in Asia overnight where a lack of notable data or news flow failed to provide much direction for traders.

Japanese stocks had a rough start to the week after the yen strengthened considerably against the dollar on Friday on the back of a woeful U.S. jobs report. The report seriously damaged the chances of a U.S. rate hike at the meeting next week and effectively undid all the Fed’s efforts over the last month or so of guiding the markets towards the real possibility of a summer move.

APAC Currency Corner – NFP fallout gets ugly

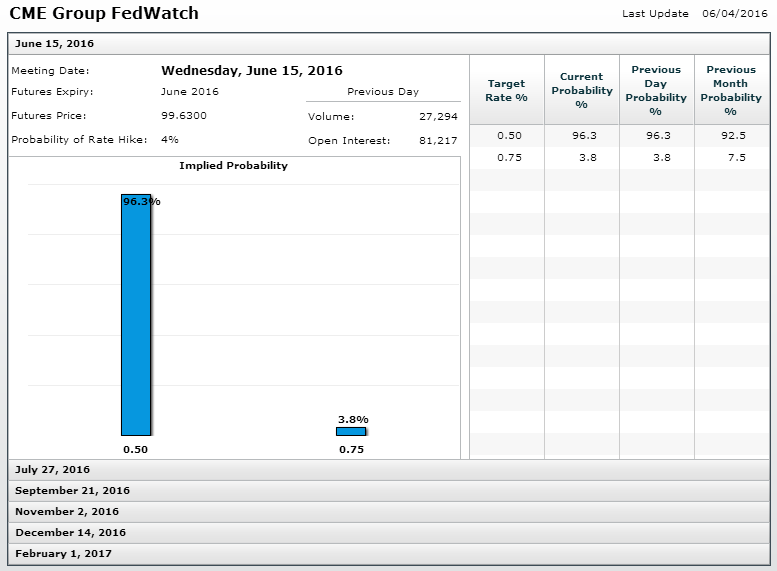

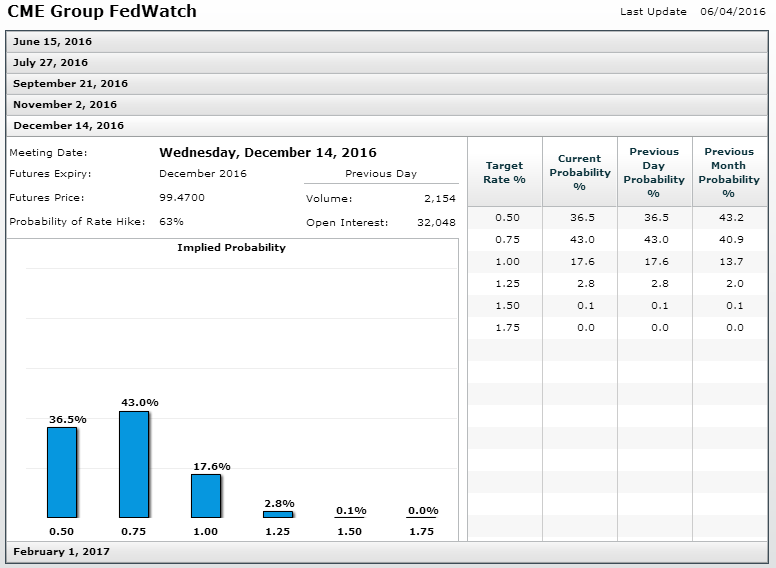

Once again, the markets are now not pricing in a hike until December which goes to show just how little belief there was in a summer move all along.

Source – CME Group FedWatch Tool

I still believe the Fed will want to raise again this summer which would allow them to go again later on in the year but Friday’s report, combined with more polls in the U.K. showing increasing support for a Brexit, has probably now taken June off the table.

The job now for the Fed is to convince the markets once again that July is still “live” and there is significant support for a move at the meeting, assuming of course that they have not in fact been deterred by Friday’s report. I imagine we’ll get more insight into this later on today, when Fed Chair Janet Yellen speaks about the economic outlook and monetary policy at the World Affairs Council of Philadelphia’s luncheon.

With the week ahead looking relatively quiet, I imagine there’ll be a growing focus on the U.K. referendum, especially with the “leave” campaign having appeared to have made significant strides over the last week or so. Two polls over the weekend actually showed support for the “Leave” campaign to be ahead of “Remain”, in one case considerably so.

Still, we’ve seen in the past that the polls can be quite unreliable while the betting odds, which have been far more accurate, still show the “Remain” camp far ahead. Regardless, the polls are likely to make people rather uneasy and we can see that quite clearly today in the pound, currently down almost 1% against the dollar, having hit three week lows earlier in the session. With both sides likely to step up their game over the next couple of weeks, I imagine we’ll see a lot more volatility in the pound and the closer the polls get, or if “Vote Leave” continues to push ahead, the pound may find itself back towards April’s lows before too long.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Craig Erlam

His views have been published in the Financial Times, Reuters, The Telegraph and the International Business Times, and he also appears as a regular guest commentator on the BBC, Bloomberg TV, FOX Business and SKY News.

Craig holds a full membership to the Society of Technical Analysts and is recognised as a Certified Financial Technician by the International Federation of Technical Analysts.

Latest posts by Craig Erlam (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024