The DAX has edged lower in the Wednesday session, as the index trades at 12,485.50. On the release front, German Unemployment Claims came in at -15 thousand, beating the estimate of -10 thousand. Eurozone Preliminary Flash GDP remained unchanged in the first quarter at 0.5%, matching the forecast. In the US, the Federal Reserve is expected to maintain interest rates at 0.75%. On Thursday, we’ll get a look at Services PMI in Germany and the Eurozone, as well as Eurozone Retail Sales.

All eyes are on the Federal Reserve, which holds its monthly policy meeting on Wednesday. A rate hike is extremely unlikely, with the CME Group pricing in a hike at just 5%. This means that the markets will be focusing on the rate statement and the views of policymakers concerning economic conditions. The Fed has two key goals which have been achieved, namely full employment and an inflation rate of 2%. One area of concern which policymakers have circled is the Fed’s balance sheet, which stands at $4.5 trillion. The minutes of the March meeting stated that policymakers want to start reducing this figure before the end of 2017, so the markets will be looking for another reference to the balance sheet in the rate statement or the minutes of the meeting. The markets are fairly confident that the Fed will press the rate trigger in June, as the odds for a hike have improved to 63%. If the rate statement is more hawkish than expected, we could see these odds increase.

The eurozone has been hampered by years of high unemployment, but the labor situation has improved considerably. The eurozone economy continues to expand, and more growth has meant more jobs and lower unemployment figures. Just a year ago, the eurozone unemployment rate was at 10.3%, but the rate has been steadily decreasing since then. The March release remained unchanged at 9.5%, within expectations. Germany has led the way, with the unemployment rate dropping to 5.9% in February. Unemployment rolls continue to shrink in Germany, and the decline of 15,000 unemployed persons was better than the estimate of 10,000. US employment numbers will also be in the spotlight this week, with ADP Nonfarm Payrolls kicking things off on Wednesday. The indicator is expected to drop sharply to 178 thousand in March compared to 263 thousand a month earlier. On Friday, we’ll get a look at wage growth and the official nonfarm payrolls report. If these indicators are not close to the estimates, we’re likely to see some movement from the DAX.

The DAX has not shown significant movement in the second quarter of 2017, but traders should keep in mind that the index has been trading at record highs this week. Will the trend continue? Current economic conditions point to the DAX continuing to climb higher. The index has outperformed most eurozone equity indexes in 2017, benefiting from a strong German economy, marked by steady growth and low unemployment. Stronger global demand has boosted Germany’s export sector and the Federal Reserve’s plans to continue to hike rates in 2017 has pushed German stocks to higher levels.

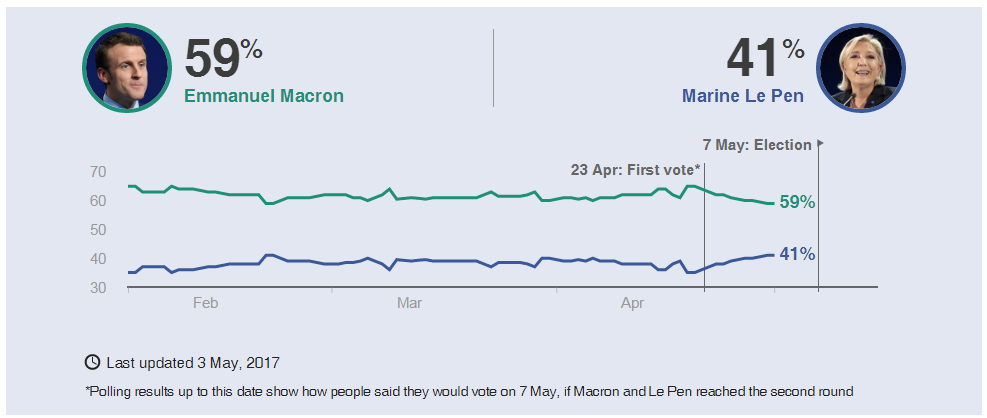

French voters will head back to the ballot box on Sunday, with Emmanuel Macron and Marine Le Pen vying for the next president of France. European stock markets have been very steady in the second round of the campaign, as opinion polls continue to show a comfortable majority for Macron:

The polling average line looks at the five most recent national polls and takes the median value, ie, the value between the two figures that are higher and two figures that are lower.

Source – BBC

French Election Timeline

May 3 – TV debate between the two remaining candidates

May 5 – [from midnight] Poll blackout

May 7 – Second round of French presidential elections. Last polls close at 19:00 BST / 14:00 EDT, with an exit poll result announced immediately.

May 11 – Official proclamation of the new President.

May 14 – [from midnight] End of Francois Hollande’s mandate

June 11 – First round of legislative elections

June 18 – Second round of legislative elections.

France Prepares for Fiery Presidential Debate

Economic Calendar

Wednesday (May 3)

- 3:55 German Unemployment Claims. Estimate -10K. Actual -15K

- 5:00 Eurozone Preliminary Flash GDP. Estimate 0.5%. Actual 0.5%

- 5:00 Eurozone PPI. Estimate +0.1%. Actual -0.3%

- 5:33 German 10-y Bond Auction. Actual 0.33%

- 14:00 US FOMC Statement

- 14:00 US Federal Funds Rate. <1.00%

Thursday (May 4)

- 3:55 German Final Services PMI. Estimate 54.7

- 4:00 Eurozone Final Services PMI. Estimate 56.3

- 5:00 Eurozone Retail Sales. Estimate 0.1%

- 12:30 ECB President Mario Draghi Speech

*All release times are EST

*Key events are in bold

DAX, Wednesday, May 3 at 6:45 EST

Open: 12,501.50 High: 12,502.50 Low: 12,477.50 Close: 12,485.50

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Kenny Fisher

Latest posts by Kenny Fisher (see all)

- Yen rises on stronger inflation - 20 December 2024

- USD/CAD steady ahead of retail sales - 20 December 2024

- British pound stabilizes as retail sales edge up - 20 December 2024