Seeing no progress on the US budget negotiations is not a surprise to investors – the markets knew what was to be expected and price action so far suggests that capital markets seem “resigned to living” with the US budget crisis. However, it’s the longer-term crux that is going to have a far greater consequence on the US economy and the ‘mighty’ dollar. If the debt ceiling happens to become a part of the equation then the greenback will have to deal with much further reaching consequences like a possible downgrade and additional emerging market woes.

Asian and European markets appear to be growing increasingly immune to US budget battles. The US fiscal cliff battle at the beginning of this year had minimal disruption on Asian and Europe. This morning’s US government partial shutdown was mostly priced in by dealers and investors alike. Global markets appear focused more heavily on the Fed’s plans to slow their bond buying efforts rather than a partial government shutdown. The flight of capital from the developing countries was staggering when investors were convinced that US liquidity was to be pared. Even the markets rebound was impressive when it became apparent that the Fed’s actions appeared less pending. The priority now is to figure out what US economic releases are affected by the shutdown, as taper becomes more data sensitive.

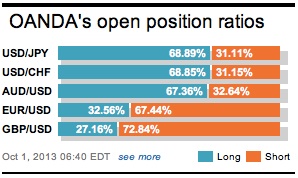

The AUD has rallied despite the US budget impasses uncertainty. A plethora of stronger Aussie economic reports of late and a decision overnight by governor Stevens and company at the RBA not to cut interest rates is supporting the mostly risk sensitive currency. Policy makers maintained a neutral bias in the crucial final paragraph of the RBA’s communiqué. However, the statement added cautious language, noting that household and business sentiment has improved.

Japanese investors were initially cheered by the fact that Prime Minister Abe is doing the fiscally prudent thing when he confirmed that his government would raise the sales tax from the current 5% to 8% in April 2014 earlier today. Despite being an important first step in curtailing the country’s debt levels, the move is expected to be accompanied by an economic stimulus package and possible corporate tax cuts to ensure the economy does not fall into a recession. Governor Kuroda and BoJ must remain vigilant and proactive. The yen however has failed to maintain its downward trajectory against G10 currencies. Market uncertainty and risk aversion is providing medium term support for the historical reserve currency.

Euro data released this morning revealed that growth in the Euro-zones manufacturing sector faded last month as factory recovery stalled in some of the regions biggest and most vulnerable economies (PMI for manufacturing – 51.1 versus 51.4). If confirmed by official figures, this would be a blow to Europe, especially since their economy staged a “muted recovery” in Q2 after 18-consecutive months of contraction. Growth in the region seems precarious at best, even Europe’s backbone and largest economy – Germany- is having employment concerns. The number of registered jobless, in seasonally adjusted terms, increased last month (+25k after a revision increase of +9k the previous month), pushing the unemployment rate higher to +6.9%. The adjusted rise is being linked to a decline in the number of people taking part in training programs, which is down by -12% on the year.

Obviously markets Stateside will be bombarded with the second-by-second progress report on Washington politics, its focus on the continuing resolution and on the debt ceiling later in the month. Fixed income dealers are expecting the short-end markets and securities with payments around mid-to late-October most likely to “show signs of stress.” For the rest of us, the debt ceiling question should not be a primary issue until closer to the expected October 24th deadline. Will market uncertainty provide support for the dollar? Will investors gravitate towards the USD as a safe haven asset? If so, then timing is most important.

At best, market reaction will be contained to a tight range against G10 currencies for immediate future. For now, the US government shutdown is being viewed by many as being EUR supportive as it makes its less likely that the Fed will be considering any tapering by year-end. The threat of the US debt ceiling not being raised by months end will be the trigger for investors to want to own some of those mighty safe haven dollars.

Other Links:

Ten Factors Affecting FX, Bonds and Equities

Dean Popplewell, Director of Currency Analysis and Research @ OANDA MarketPulseFX

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019