European equity markets are expected to open a little higher on Thursday, continuing the trend over night that saw most Asian markets in the green and US indices smash their way to new all-time highs.

Just as it seemed that investors were starting to suffer a little bit of Trump fatigue, Wednesday produced the biggest daily gains we’ve seen this year in the US. It would appear that not only are investors not yet losing patience with Trump’s vague rhetoric, they’re also buying into the Fed’s view that more rate hikes are needed to prevent the economy running too hot.

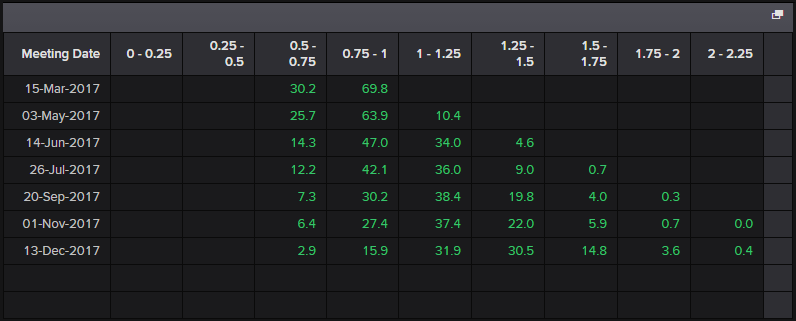

Not all investors will agree with this belief of course but the very fact that March has gone from being almost fully priced out to almost 70% priced in and the probability of three rate hikes this year is almost 50%, and yet equity markets are rallying, is a good sign. It’s not too long ago that investors would have freaked at the prospect of one rate hike, let alone three in one year.

Source – Reuters Eikon Terminal

Source – Reuters Eikon Terminal

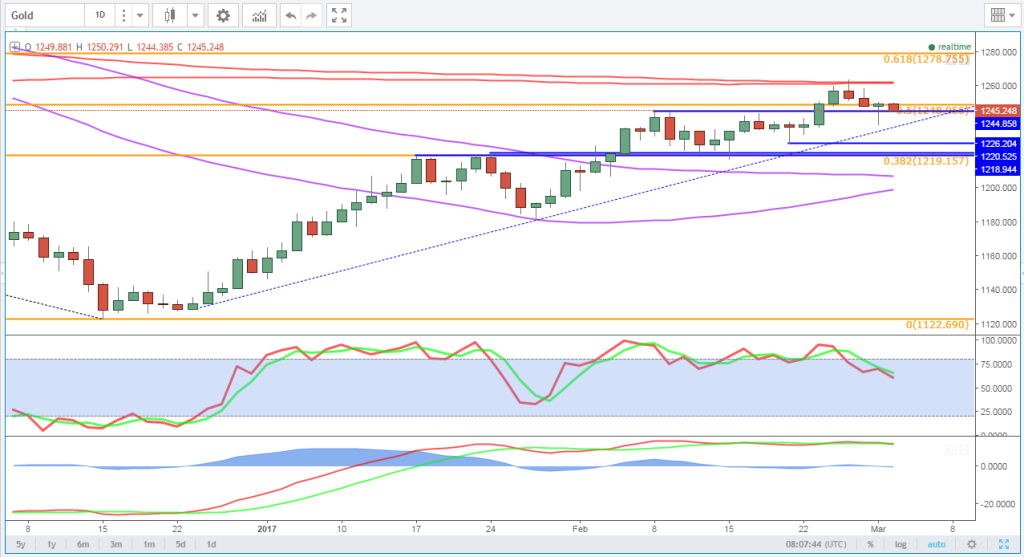

Of course, this may only be the case as long as investors continue to buy what President Trump has to sell and there is still a significant amount of underlying risk in the markets right now – largely political – which may explain why Gold – a traditional safe haven asset – is only trading 1.5% below its near-four month high. The yen, another safe haven play, has also continued to perform quite well throughout all of this, another sign that all is not as rosy as they may seem.

OANDA fxTrade Advanced Charting Platform

OANDA fxTrade Advanced Charting Platform

Still, the dollar hit its highest level since early January on Wednesday, busting through what had been a stubborn resistance along the way, and with interest rate expectations rising ahead of the Fed meeting in two weeks, further upside may be on the horizon which could further pressure Gold. Should the polls for the second round of voting in France continue to show a widening gap between Emmanuel Macron and Marine Le Pen – the likely two candidates to make it through the first – in favour of the former, then this may aid Gold’s move lower with the latter seen as being potentially disastrous for the euro area.

Gold Unchanged as Trump Speech Underwhelms Markets

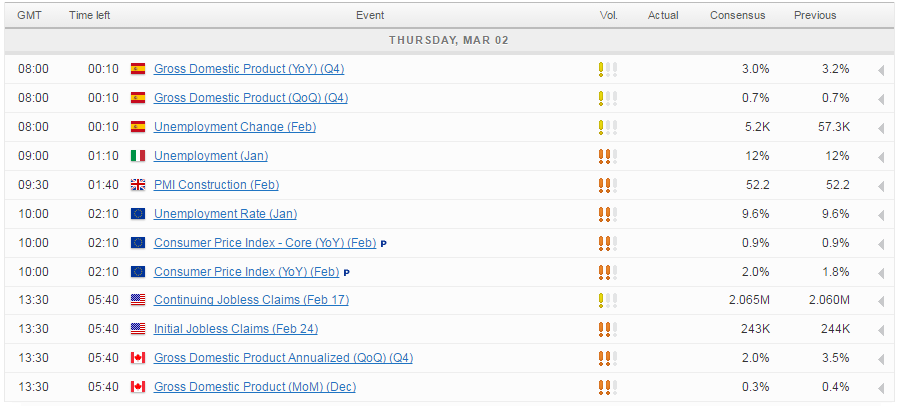

The focus this morning will be on the flash CPI number from the eurozone, where inflationary pressures have been building – albeit largely driven by commodity prices and the weaker euro – fuelling the discussion on whether a further reduction in asset purchases from the central bank is warranted. We’ll also get the latest construction PMI from the UK, and unemployment data from Spain and Italy. This afternoon we’ll get jobless claims data from the US followed later on in the evening by a speech from the Fed’s Loretta Mester who, given her very hawkish stance, will likely add her voice to those pushing a hike in March.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Craig Erlam

His views have been published in the Financial Times, Reuters, The Telegraph and the International Business Times, and he also appears as a regular guest commentator on the BBC, Bloomberg TV, FOX Business and SKY News.

Craig holds a full membership to the Society of Technical Analysts and is recognised as a Certified Financial Technician by the International Federation of Technical Analysts.

Latest posts by Craig Erlam (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024