All eyes are on Cyprus again today as local banks are due to reopen after the government announced capital control measures to prevent a flight of deposits. The ordinary investor remains cautious, with current sentiment further undermined by the Italians failure so far to form a government and China’s tightening of its oversight over the country’s rural banks. Throw month-end, quarter-end and Japanese year-end into the mix and a few fireworks are possible. With the Easter long week-end upon us most investors will want to play it safe as liquidity becomes more of an issue across the asset classes in the next 24-hours.

Chinese authorities have been able to rattle a few investors overnight, especially during the Asian session, after banks were ordered to tighten controls over wealth management products, a popular but “opaque element in the country’s shadow banking system.” China’s Banking Regulatory is hoping to increase transparency and reduce risk. As with many new financial Chinese rules, corporations spend much time finding ways to circumvent them resulting with the new rules ending up lacking bite.

The 17- member single currency ‘bear’ is beginning to ground the scene, focusing again on elevating periphery yields. The euro bond market has received another jolt from an old foe, Italy and its never-ending political saga. The well-documented government gridlock weighed on the demand at the mid-week Italian bond auction. In doing so, has dragged higher other periphery yields while the euro classic safe haven bund rallied in price along with US treasuries and UK Gilts. Even the lure of higher Italian returns produced a feeble turn out at the sale of 5-year bonds mid-week.

Flight to safety sees the Yen holding demand into the Japanese financial year-end despite the new BoJ governor Kuroda disclosing his policy plans for government-bond purchases and other easing measures yesterday. A stronger bid for US Treasury’s, causing the tightening of the UST/JGB spread, is putting more pressure on USD/JPY. Mideast sellers continue to favor selling the dollar through 94.00 where Japanese bids are layered for the next 50-points ahead of the highly anticipated BoJ meeting next week. Since November investors have been positioning themselves for bold moves by the central bank under the influence of Abenomics. Next week we get to see if Japanese policy makers are again capable of disappointing current position holdings so soon.

With the Cypriot patchwork program in progress, the market has been able to focus its attention towards the weak Italian effort to form a new government after last month inconclusive elections. Political paralysis impedes the growth potential of any economy, making it near impossible for business to be completed.

The ECB’s pledge to do “what ever it takes within its mandate to preserve the EUR” has been the primary support for Italian and Spanish bonds to date – the market has been wary of aggressively selling any product in the presence of such an insurance policy. However, ongoing worries about Spanish banks after the Cyprus “bail-in,” the outlook for their economy getting weaker and potential social unrest due to high youth unemployment has many investors initiating new risk aversion trading strategies.

What’s in vogue – a bailout or a bail-in? The Eurozone policy makers attempt to limit the fallout of the Cyprus template comments looks to be falling on deaf ears. The Cypriot “bail-in” fallout is effectively telling uninsured Eurozone depositors to change their “savings” habits. Where are they to hide? What is considered safe? For now, the historical euro risk adverse sanctuary remains at the very short-end of the German yield curve. Nervous investors have also been gravitating towards the traditional safer currencies like GBP and CHF. While at it, you might as well throw a couple of Scandies into the mix.

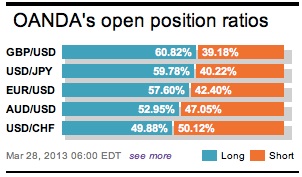

There is no fresh downside momentum in EUR/USD, but little bounce either. The trend of ratcheting through option barriers and corporate bids looks set to continue. The EUR/USD players are short euros and are certainly shorter than the last CFTC report on March 15th (-EUR7.25b). Throughout the Cyprus bailout crisis this market has feared a squeeze – one that has not truly materialized – why not? Is this market really not short enough? Apparently speculators were twice as short during the last two periods of a similar bearish trend at these levels. Previous reports indicate that the EUR bear was twice as short last November and a record –EUR31b short 10-months ago. The spec shorts may be undersold and if so, they have little to fear. Short-term movement continues to be dominated by the crosses, especially EUR/GBP and EUR/JPY selling. Outright, the important short-term target for the techies is 1.2680.

Other Links:

EURO Strangled By Options, Cyprus And Holiday’s

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019