Wednesday August 8: Five things the markets are talking about

Trade concerns continue to hover over capital markets. Yesterday, the U.S indicated that it will begin imposing another +25% duties on an additional +$16B in Chinese imports beginning in a fortnight. On the first go around, China swore to retaliate, they have yet to give specifics, but at the very least, it will be an in-kind retaliation.

Data overnight showed that China’s exports grew faster than expected last month and imports surged, which suggest that the “ongoing” trade war has yet to have a material impact on the worlds second largest economy’s bottom line.

Nevertheless, the prospects for a full blown trade war has the U.S dollar remaining better bid on pullbacks in a relative tight summer range.

Sovereign yields, further out the curve, trade a tad higher as dealers make room to take down today’s record amount of 10-year Treasury debt worth +$26B, and an all-time high of +$18B in 30-year bonds tomorrow.

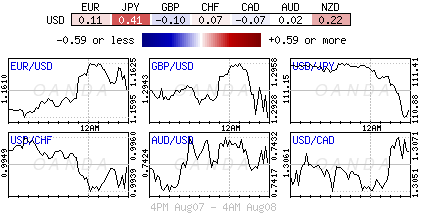

In currencies, the market is focused on sterling (£1.2904) as it encroaches on its 11-month low as politics continues to provide the overriding direction for the currency. And then there is the Turkish lira ($5.2923) as it makes it way towards record lows on market worries about President Erodgan’s grip on monetary policy.

On tap: The Reserve Bank of New Zealand’s (RBNZ) official cash rate decision and monetary policy statement is due this afternoon (05:00 pm EDT). No change in rates or accompanying statement is expected.

1. Stocks mixed overnight session

In Japan, the Nikkei edged lower overnight as the market waits for the start of U.S-Japan trade talks. Will the U.S be taking a hard stance, similar to that of China and Europe? Both the Nikkei and broader Topix ended -0.1% lower.

Down-under, Aussie shares rallied overnight, with financials higher after reporting a smaller fall in profit than expected, and while miners gained on strong import data from China. The benchmark S&P/ASX 200 index rose +0.2%, erasing most of Tuesday’s losses. In S. Korea, the Kospi index rose modestly, closing out 0.06% higher.

In Hong Kong, shares rise on tech and energy boost, but fears of a deeper trade war is capping gains. At close of trade, the Hang Seng index was up + 0.39%, while the Hang Seng China Enterprises index rose +0.32%. In China, the Shanghai Composite index closed down -1.23% while its blue-chip CSI300 index ended down -1.59% mostly on profit taking after Tuesday stellar session.

In Europe, regional bourses trade mostly lower, pressured generally by weaker earnings out of Europe.

U.S stocks are set to open little changed (+0.0%).

Indices: Stoxx600 -0.2% at 389.8, FTSE +0.3% at 7742, DAX -0.2% at 12627, CAC-40 -0.1% at 5517, IBEX-35 -0.10% at 9762, FTSE MIB +0.0% at 21863, SMI -0.4% at 9167 S&P 500 Futures 0.0%

2. Oil dips on weak China imports, but sanctions and weak U.S stocks support

Oil prices have dipped a tad overnight, pressured by Chinese weaker import data, although the market remains well supported on pull backs by falling U.S crude inventories and the introduction of sanctions against Iran.

Brent crude oil futures are at +$74.50 per barrel, down -15c, or -0.2% from Tuesday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$69.15 per barrel, down -2c.

Data shows that China’s July crude oil imports recovered slightly last month after falling for the previous two-months, but are still amongst the lowest due to a drop-off in demand from the independent Chinese refineries.

With U.S sanctions against Iran, which shipped out +3M bpd of crude in July, officially came into effect yesterday midnight and the market is anticipating that supply losses could range from +600K to +1.5M bpd.

Dealers are also focusing on the U.S market, where yesterday’s API data showed that crude inventories fell by -6M barrels in the week to Aug. 3 to +407.2M.

The market will take its cues from today’s EIA inventory report (10:30 am EDT).

Ahead of the U.S open, gold prices are better bid, supported by a mixed U.S dollar. Spot gold is up +0.2% to +$1,213.02 an ounce, after rising +0.4% in Tuesday’s session.

3. Sovereign yields could back up further

Yesterday, the U.S Treasury Department sold +$34B three-year notes and it was the largest three-year auction in eight-years. Later today, the Treasury will sell a record amount of 10-year debt worth +$26B (1:01 pm EDT) and tomorrow an all-time high of +$18B in 30-year bonds. With so many products on offer, dealers are expected to again cheapen up the curve to make room ahead of the deadline.

The yield on 10-year Treasuries has rallied +1 bps to +2.97%, while Germany’s 10-year bund yield is holding steady at +0.403%. In the U.K, the 10-year Gilt yield has rallied +1 bps to +1.314%.

4. Sterling’s Wild West

Trading GBP/USD (£1.2903) is proving to be a bit like the Wild West – unpredictable – the pound is again threatening to penetrate yesterday’s record 12-month low now that its failed to benefit from last week’s Bank of England rate rise. Markets are now turning their attention to the Brexit process, which will likely dominate trends in GBP for the remainder of this year.

The Turkish lira ($5.2920) has recovered some lost ground after plummeting to new record lows Monday ($5.42), helped by the Central Bank of the Republic of Turkey (CBRT) announcing a cut in the foreign exchange reserve requirement ratio (RRR) for commercial banks, a measure which should boost dollar liquidity. However, this week’s necessary course of action reaffirms the central banks reluctance to hike rates. Nevertheless, the plunge in the currency over the past few weeks is now on a scale, which has, in the past, prompted the CBRT to hike interest rates aggressively.

Will the CBRT hike the repo rate this week? They need to, but will they dare defy President Recep Tayyip Erdogan?

Note: A Turkish delegation is visiting Washington this week to discuss the friction between both countries. But the U.S has stated that they remain at odds on its core demand that Turkey free American an evangelical pastor.

5. China’s trade balance tightens

Data overnight showed that China’s trade surplus narrowed sharply in July, with imports surging as trade tensions with the U.S escalated.

China reported a trade surplus of +$28.05B in July, compared with a surplus of +$41.61B in June. The market was expecting a surplus of +$39.10B.

Digging deeper, exports rose +12.2% y/y, following June’s +11.3% increase. The market was looking for a +10% growth number.

Imports were up +27.3% in July y/y, accelerating from a +14.1% increase the previous month.

China’s trade surplus with the U.S. narrowed to +$28.09B in July from a record monthly high of +$28.90B in June.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019