Election gains wiped out

The pound came under renewed pressure in Asia this morning with GBP/USD falling 0.36% to 1.3072, the lowest level since December 12 and meaning that all the election gains have been given back. The jitters have arisen since Boris Johnson proposed to put into law a prohibition to any extension to the Brexit transition period beyond the end of December 2020. It’s possible a vote on the bill may be as early as Friday. Doubts have been raised whether all the agreements can be negotiated and put in place by that deadline.

GBP/USD Daily Chart

Source: OANDA fxTrade

Fitch affirms UK’s rating

Fitch Ratings yesterday affirmed the UK’s AA and advised that it had been taken off rating watch negative though the outlook remains negative. The agency said the outcome of the UK election had removed the short-term risk of a disruptive no-deal Brexit. The negative outlook is attributed to concerns about the uncertain future of UK-EU relations.

Japan posts a smaller-than expected trade deficit

Japan’s trade balance improved dramatically in November with the deficit narrowing to ¥82.1 billion, well below the ¥369.0 billion economists had expected. The wide miss came from a hefty slump in imports of 15.7% from a year earlier, while exports fell a less-than-expected 7.9% y/y. The Bank of Japan’s rate meeting is not expected to result in any changes to either rates or the bond-buying programme but, as many board members have constantly repeated, an accommodative policy is still needed.

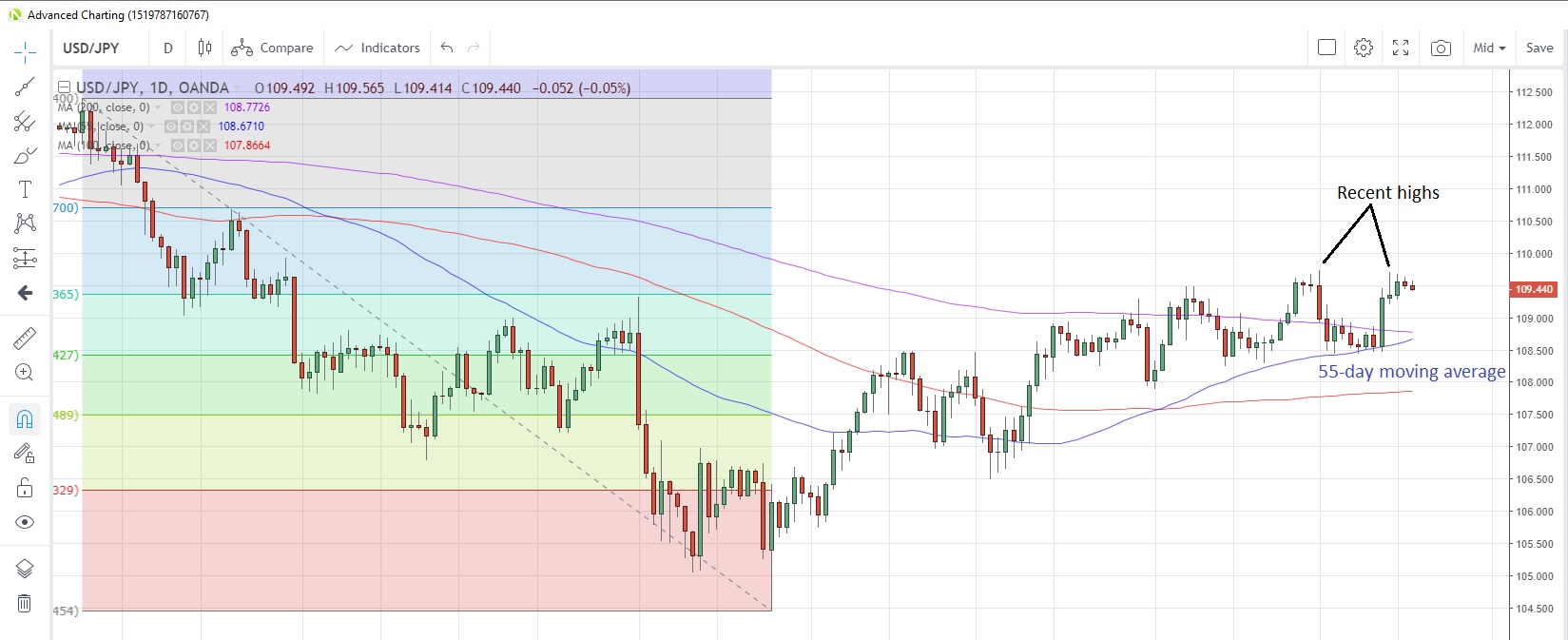

There was little reaction in USD/JPY after the data, with the pair confined to a tight range for most of the session. Two recent highs around the 109.70-73 area may provide immediate resistance while the 55-day moving average at 108.67 and the 200-day moving average at 108.77 will likely lend support.

USD/JPY Daily Chart

Source: OANDA fxTrade

German IFO surveys on tap

The December IFO surveys for Germany are due today, with forecasts that the expectations index will improve to 93.0 from 92.1 in November. That would be the third monthly improvement in a row as the index rebounds from the September low.

The UK’s PPI, RPI and CPI numbers for November are also scheduled, with CPI seen rising 0.2% m/m following a 0.2% decline in the previous month. The Euro-zone’s consumer prices are expected to drop 0.3% from a month earlier. Canada’s inflation data are also due, with CPI probably falling 0.1% month-on-month but rising 2.2% year-on-year.

There are no major US data releases scheduled for today, but speeches from the Fed’s Brainard and Evans complete the calendar.

The full MarketPulse data calendar can be viewed at https://www.marketpulse.com/economic-events/

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Andrew Robinson

Latest posts by Andrew Robinson (see all)

- RBA cuts rates on virus impact - 2 March 2020

- Commodities Weekly: Oil rises first time in eight days - 2 March 2020

- Daily Markets Broadcast 2020-03-03 - 2 March 2020