Tuesday October 29: Five things the markets are talking about

Euro equities are rallying for a second consecutive session, along with U.S futures as Asian indexes rebounded as the market turned its attention again to a number of corporate earnings and the prospects for a Sino-U.S trade deal.

President Trump, on Fox news last night was predicting a “great deal” with China, despite his administration preparing to announce by early December tariffs on all remaining Chinese imports if talks next-month fail to ease the trade war.

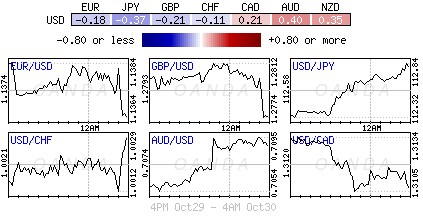

In currencies, the safe-haven yen eased and the Aussie dollar found support, with both moves aiding their domestic equity indexes.

In China, authorities guided the yuan to a decade low outright, a move that could fuel expectations of a further, self-reinforcing slide.

While the EUR remains under pressure on yesterday’s news that Germany’s Chancellor Merkel has planned her exit after Sunday’s disappointing state elections, and sterling has fallen to a 10-week low as markets react hesitantly to yesterday’s fiscal giveaways in the U.K budget.

In bonds, the U.S ten-year note backed up past +3.11% as risk-on trading strengthened. Elsewhere, WTI oil has fallen to trade atop of +$67 a barrel.

On tap: There are a plethora of U.S companies expected to report earnings – Facebook and GE top many list.

1. Stocks in the black

In Japan, the Nikkei rallied overnight as investors bought beaten-down cyclical stocks, softening fresh worries about US-China trade frictions. The Nikkei share average ended +1.5% higher, posting the biggest daily gain in two-months. The broader Topix rallied +1.4% in heavy volume.

Down-under, Aussie shares reversed earlier losses to end higher overnight on news that Beijing wishes to stabilize its markets, though underlying sentiment remains delicate. Broad-based gains pushed the S&P/ASX 200 index up +1.3%. In S. Korea, the Kospi stock index rose this morning, snapping a five-session losing streak. The index closed +0.93% higher.

Note: The Kospi is down around -19.1% so far this year, and down by -12.79% in the past month.

In China, the benchmark Shanghai Composite and the blue-chip CSI 300 gained +1.0% and +1.1%, respectively, reversing earlier losses in a volatile session. Indexes found support after China’s securities regulator said it would “encourage share buybacks and mergers and acquisitions by listed firms, and would enhance market liquidity,” in the latest attempt to put a floor under the country’s weak equity markets.

In Hong Kong, the Hang Seng index closed at its lowest in nearly 18-months, as tepid investor sentiment outweighed promises of support for mainland markets. At the close, the Hang Seng index was down -0.9%, while the China Enterprises Index lost -0.1%.

In Europe, regional indices trade mixed this morning following a positive session in Asia and mixed U.S futures following weakness yesterday. Italy’s FTSE MIB underperforms after GDP came in below exceptions (Q3 GDP +0% vs. +0.2%).

U.S stocks are set to open in the ‘black’ (+0.3%).

Indices: Stoxx50 -0.2% at 3,150, FTSE +0.2% at 7,037, DAX -0.3% at 11,299, CAC-40 -0.3% at 4,976, IBEX-35 -0.1% at 8,815, FTSE MIB -0.5% at 18,943, SMI +0.3% at 8,776, S&P 500 Futures +0.3%

2. Oil prices slip on rising supply, trade tensions, gold lower

Oil prices start the day on the back foot, weaker on concerns that the Sino-U.S trade dispute will dent economic growth and by signs of rising global supply despite upcoming sanctions against Iran kicking in on Nov 4.

Brent crude oil is down -15c a barrel at +$77.19, while U.S light crude (WTI) is unchanged at +$67.04.

Note: Both contracts have recovered ground over the past week, but are around -$10 a barrel below their four-year high print in early October.

CFTC data last Friday showed hedge funds slashed their “bullish” bets on U.S crude to the lowest level in more than a year – they cut their combined futures and options position in New York and London by -42,644 contracts to +216,733 in the week to Oct. 23.

The IEA said earlier today that high oil prices were hurting consumers and could dent fuel demand at a time of slowing global economic activity.

On the supply side, oil markets remain tense ahead of forthcoming U.S sanctions against Iran’s crude exports, which are set to start on Nov. 4 and are expected to tighten supply, especially to Asia, which takes most of Iran’s shipments.

According to Baker Hughes data last Friday, in North America there is no oil shortage. Production is set to rise further as U.S drillers added two oil rigs in the week to Oct. 26, bringing the total count to +875, the highest level since March 2015.

Ahead of the U.S open, gold prices have eased a tad as the ‘big’ dollar finds support on worries over slowing economic growth and fears the Sino-U.S trade war could intensify again. Spot gold is down -0.2% at +$1,227.41 an ounce, after falling -0.3% yesterday. U.S gold futures are up +0.2% at +$1,229.30 an ounce.

3. BTP yields off lows as Italian economy flat-lines

Italian BTP yields have backed upped this morning, reversing an earlier fall, after GDP data showed that the country’s economy ground to a halt in Q3 (+0% vs. +0.2%e).

Italy’s 10-year BTP yield was up +5 bps at +3.385%, after having been as low as +3.32% at the start of the Euro session. The BTP/Bund spread tightened -6 bps to +293 bps – the tightest spread in three-weeks.

Elsewhere, the yield on U.S 10-year notes gained + 2 bps to +3.11%, the largest rise in almost two-weeks. In Germany, the 10-year yield climbed +1 bps to +0.39%, while in the U.K, the 10-year Gilt yield rallied less than +1 bps to +1.402%.

4. U.S dollar has earned its stripes

The pound has fallen -0.33% to its lowest level in 10-weeks outright at £1.2756 as investors react suspiciously to fiscal giveaways in the U.K budget yesterday, which was conditional on a favourable Brexit deal being reached. With no Brexit deal done, and talks in deadlock, doubts exist as to whether the largest giveaway in eight-years will ever happen.

EUR/USD is steady at €1.1367 area but continues to see soft regional data, as both France and Italy Q3 GDP data came in below expectations. ECB noted last week that recent incoming economic data had been weaker than expected, but reiterated “risks to economic growth were still broadly balanced.” With Germany’s Merkel poor showing in state elections, dealers note that there is still the possibility of early election for Germany at some point.

China fixed the yuan at a ten-year low against the U.S dollar overnight. The PBoC fixed the midpoint of the dollar’s trading range at ¥6.9574 compared with ¥6.9377 on Monday. The Yuan’s value in the fix was near where it ended in daily trading on Monday.

5. Euro preliminary flash Q3 GDP

The euro-zone had its weakest quarter since it returned to growth five years ago in Q3, held back by a decline in auto production that was likely temporary, and slowing demand for exports that was likely not.

Note: The eurozone economy kept pace with that of the U.S in 2016 and 2017, but has fallen behind it this year.

Data this morning published by Eurostat showed the seasonally adjusted GDP for Q3 rose by +0.2% in the euro-area (EA19) and by +0.3% in the EU28 compared with the previous quarter.

In Q2, GDP had grown by +0.4% in the euro-area and by +0.5% the EU28.

Compared with the same quarter of the previous year, seasonally adjusted GDP rose by +1.7% in the euro-area and by +1.9% in the EU28 in Q3 of 2018, after +2.2% and +2.1% respectively in the previous quarter.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019