Investing is greatly influenced by emotion and perception. The market view has current sentiment ever rising, as the mood ahead of this morning’s non-farm payroll remains relatively upbeat after US data this week showed private sector job growth for February with an increase of +198k, higher than January and above expectations.

NFP is the granddaddy for all economic indicators. So far, Thursday’s better than expected US weekly initial claims benefits has not dramatically changed many individual’s outlook for this morning’s release. Consensus is looking for a +160k print confined within the +145k to +225k range forecasted. The unemployment rate is expected to ease a tad to +7.8% from +7.9%, with average hourly wages standing pat at +0.2% as most labor market indicators – jobless claims, ISM employment gauges, ADP –point to continued solid job gains.

How will the market interpret the data? From a yield perspective, an NFP headline print close to consensus would likely be supportive of US Treasuries holding their recent price move lower, and would be consistent with the generally positive US data this week. A particularly strong print should be capable of pushing US yields a good deal higher, especially 10-years – trading back through +2% again.

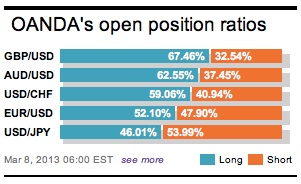

An above-consensus reading would be ‘big’ dollar supportive against low yielding currencies like the EUR and JPY and risk-on price action in currencies geared to growth in the US. The US’s closest neighbors, Canada and Mexico are capable of underperforming in this scenario. The two main FX trends are clear; a weaker yen and a stronger USD. This has made owning USD/JPY a market obvious call of late. With JPY being the currency most risk sensitive to data, it should lead on payrolls. Strong data will see USD longs squeezed again, and for neutral positioned traders, owning USD dips will look very appealing.

Also an aid in underpinning market sentiment was the release of some stellar overnight numbers from China. The world’s second largest economy posted a surprise trade surplus last month. This was achieved on the back of a stronger than expected export print. China’s trade recorded a strong surplus of +$15.2b, much stronger than consensus for a -$6.9b deficit. Analysts note that taking the first two months together; trade surplus totaled +$44b, a substantial increase compared to the -$4.9b deficit in the first two-months of last year. Exports surged, rising +21.8%, y/y, in February. This takes the growth rate in the first two months of the year to a non-shabby +23.6%!

This has been a tough week in assimilating data, dominated by a plethora of Central Bank rate announcements. Policy makers are about to enter the weekend very much unscathed after sticking to a tight script and not wanting to dent investor confidence any more. In Europe there does not seem to be any urgency from Draghi to cut rates. The lowering of growth forecasts by ECB will only increase market expectation for a rate cut later this year. GDP for 2013 is now seen at -0.9% to -0.1% versus -0.9% to +0.3%. The mid-point for inflation for this year has been left unchanged at +1.6% while next year has been lowered slightly to +1.3% from +1.4%.

Draghi is doing what all-good traders and analysts should be doing and that is making the markets understand that he and his cohorts will remain accommodating. By day’s end this process will fine-tune all necessary money markets adjustments.

The EUR has bounced nicely from yesterday’s intra-day lows mostly on the back of investor’s prior positions. A higher percentage of individuals were expecting for, at the “very least,” more dovish words from Draghi. Squeezing the weaker EUR shorts perhaps even further was the “no mention” of the single units value. The market caught a bid on the back of the ECB possibly feeling a bit more comfortable with the exchange rate.

Many were hoping that the BoE would initiate further monetary stimulus in light of recent downbeat macroeconomics data, and even more so after the Moody’s rating agency stripped the UK of its triple-A status. In truth, unless UK data continues to show further deterioration only then will the ‘pound’ maintain a negative trajectory amongst the major pairings. If UK headlines continue to miss the high notes there will be pressure on the BoE to ease further. It’s looking more likely that these tough decisions will be left up to the new Governor when he arrives.

The 17-member single currency has mostly stood pat in the overnight session, at least until the arrival of some “early-birds” from North America, who seemed to have managed to buy EUR/JPY, triggering some stops and dragging the EUR above yesterday’s highs ahead of NFP. The technical traders continue to want to fade the 100-DMA (1.3127-30) along with other speculative and prop trading positions that seem to be layered all the way up to the prominent resistance level of 1.3160-70. Do not expect many brave souls to deviate from their game plan ahead of NFP where many will be expecting Yen to take the lead.

Other Links:

What Can We Expect From The ECB’s Euro?

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

He has a deep understanding of market fundamentals and the impact of global events on capital markets.

He is respected among professional traders for his skilled analysis and career history as global head

of trading for firms such as Scotia Capital and BMO Nesbitt Burns. Since joining OANDA in 2006, Dean

has played an instrumental role in driving awareness of the forex market as an emerging asset class

for retail investors, as well as providing expert counsel to a number of internal teams on how to best

serve clients and industry stakeholders.

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019