With only 47 more companies yet to release Q1 earnings within the S&P 500 index (which makes that less than 1/10), we have a good idea of how S&P 500 as a collective bloc has been doing. Total earnings from the companies that have reported their results are up 3.3% with 65.3% of companies beating analysts estimates. However, revenues are lower, with less than half of the companies beating the headline estimate.

From a share valuation perspective, higher earnings is more important than higher revenue. But from an economy evaluation perspective, lower revenues can be an indication that the economy is actually shrinking, and a precursor to wider deflation risk. What it means is this – do not simply assume that the economy is doing better because share prices are higher. In fact, the falling revenue is in line with falling global consumption and also agrees with the observation of falling exports across the globe (bar China, whose numbers are highly dubious).

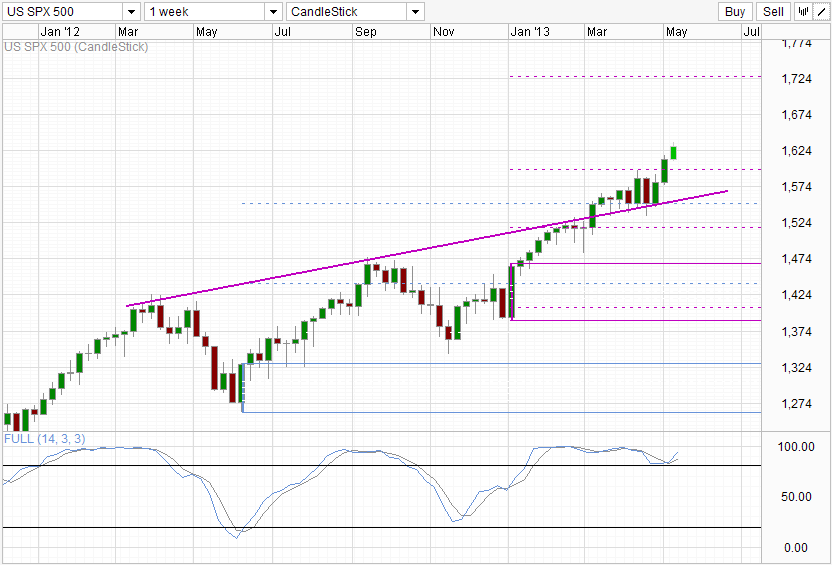

However, this doesn’t mean that price will move down from here immediately. Quite the opposite. Price is currently in a strong uptrend that is fueled by strong optimism and also incoming foreign funds as investors escape Europe and seek higher returns. Australia and Emerging Markets were the prime choice a few years ago, but with S&P 500 in such bullish mood, US stocks are attracting many foreign suitors right now.

From a technical perspective, current bull trend does feel a little extended even though we’ve just cleared the 261.8% Fib extension (of the initial push) and bounce off the rising trendline which was acting as a ceiling before Mar. The last bull cycle that started in Jun 2012 saw price similarly punch above 261.8% extension only to fall back shortly after. Looking back even further, the bull cycle that started in Dec 2012 also had the peak just around the 261.8% extension. If history provides any reference, a break of 261.8% does not lead us to 423.6% directly. However, do remember that past trends may not necessary represent future occurrence, hence traders should always look out for confirmation for bearish pullbacks rather than selling now and hope for that the pullback will happen.

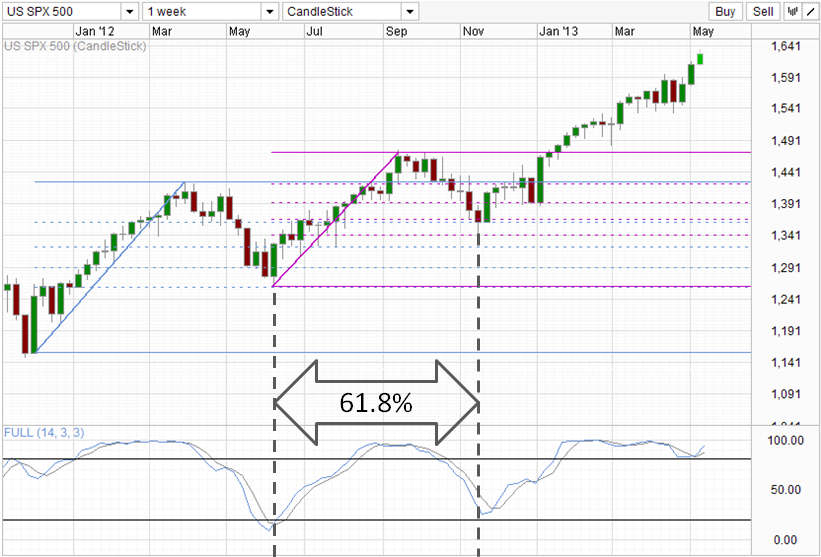

How much will the pullback be then? Using historical Fib retracement of the full bull cycles, the magic number appears to be 61.8%. If price does pullback below the 261.8% Fib discussed above, traders may wish to take note of the 61.8% Fib which may be around 1,450 – 1,470 (depending on where you consider as current uptrend starting point – either Jan’s low or Nov 12 low). The same precaution applies though. Traders should look out for evidence of rebound and not simply bet your farm on a rebound scenario.

Fundamentally, a pullback is also possible if current optimism evaporate. ECB has just revised its 2013 GDP forecast lower, while RBA is also cut its inflation forecast, while China has also stated growth will be lower. Amidst such pessimism, it is hard to imagine price being able to climb much higher towards the 423.6% extension. If price is unable to climb higher, expect traders to lose their optimism and start to look close at the underlying fundamentals, making a case for pullback in the future. When? No one can tell, but if Fib 261.8% is of any relevance this cycle, then we could see a retracement soon. Perhaps Sell in May and Go Away may still apply after all.

More Links:

NZD/USD Technicals – Kumo Breakout Confirmed

USD/SGD Technicals – Pushing Towards Channel Top

AUD/USD – Holding Declines after RBA Cuts Inflation Forecast

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

centers on forex and macro-economic trends impacting the Asia Pacific region.

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014