USD/JPY fell back towards 101.5 after failing to breach 102.0 following 3 attempts to do so yesterday. The decline during Today’s Asian session appears to coincide with the release of Japanese Domestic Corporate Goods Price Index, which came in better than expected in both the M/M and Y/Y numbers – 0.3% vs 0.1% expected and 0.0% vs -0.2% expected respectively. However, it is highly unlikely that JPY strengthened on such news, as this is generally not regarded as an important news event. Furthermore, it has been well documented that JPY tended not to react significantly to any Japanese domestic data, but rather move more on Central Bank BOJ speculative actions, thus decreasing the likelihood even more.

Looking at EUR/USD and AUD/USD, it seems that the dip in USD/JPY is USD strength related. However, looking at S&P 500 and Dow Industrial Futures, prices aren’t really looking lower. Across Asia, Hang Seng Index and ASX are still holding onto their early morning gains, while Nikkei 225 did see a dip, which is likely a result of strengthening Yen rather than an indication of risk off appetite. This lead us to the unlikely suspect, but currently top of the list by process of elimination – Gold Rally/Recovery, driving USD lower during Asian trade.

As we are running rather light from our economic news docket, the question we need to ask ourselves is that whether current Gold prices will be able to continue influence USD on a longer term basis. Also, even if Gold influence on USD and subsequently the rest of the market is still in play, will the recovery in Gold continue, driving USD lower for the rest of the day? These are good questions that should be answered to give us a broader view of the market today.

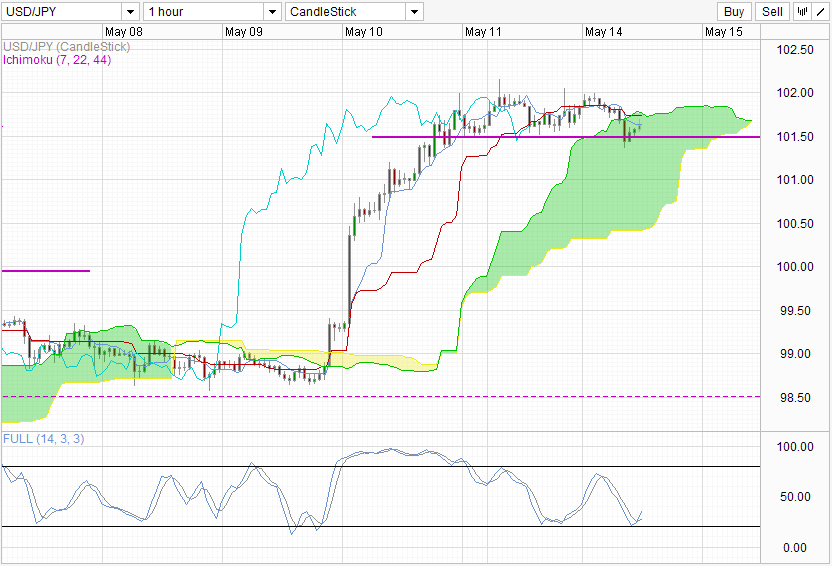

Hourly Chart

From USD/JPY own technicals, the dip caused by Gold pushed price into the Kumo rather than allowing the Senkou Span A to keep price afloat and closer to 102.0. Bulls will be glad that 101.5 support continues to hold, which is understandable considering that price will experience buoyancy while trading within Kumo. Stochastic indicator suggest that this dip may be short, with readings pushing higher and a stoch/signal cross already underway. All these open up the likelihood of price retesting 102.0 once more, but should price maintain within the current 50 pip range, there remains a likelihood where a retest of 101.50 tomorrow may result in price breaking below Kumo in conjunction with a bearish Kumo twist. Both bearish signals will add pressure on the support which may increase the likelihood of price breaking towards 100.5 and perhaps even 99.0.

Daily Chart

The above scenario is not obvious via the Daily Chart though, as current price is still higher than Friday’s closing levels. However, there is a sense of slowing bullish momentum and should momentum reverse, the significant support level would be 96.8, the previous consolidation ceiling. Stochastic readings are looking likely to peak now with Stoch/Signal line which suggest that a bear corrective cycle may be happening soon, but we’ll certainly require strongly reversal signal and confirmation to be established.

Fundamentally, traders should continue to watch out for USD related news moving forward as BOJ is expected to remain silent for a considerable amount of time now. A loss of risk appetite scenario which has historically bring Yen stronger is unlikely right now with stock prices trading higher consistently. Nonetheless, traders should still be ready if any strong swing in sentiment may transform small bearish corrective pullbacks into full fledged bearish reversals.

More Links:

GBP/USD – Claws Back Some Ground to Above 1.53

AUD/USD – Continues to Drift Lower to 0.9940

EUR/USD – Consolidates Just Below 1.30

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

centers on forex and macro-economic trends impacting the Asia Pacific region.

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014